Can Nvidia Live Up to the Lofty Expectations of an AI-Obssessed Market?

Here's what to expect leading up to the print, my thoughts on inflation, and how I'm playing China and muni closed-end funds.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The market survived last week’s PPI and CPI reports. They came in relatively hot, but markets were able to look deeper at the data and came away nonplussed:

- On PPI in particular, there were downward revisions to prior months.

- Some components, most noticeably housing, have a built-in lag effect, which should ease pressure going forward.

- Many of the “problematic” areas of inflation, were viewed as relatively “one-off” type of things, like auto insurance.

As a whole, I agree that inflation has been coming down, which helped explain why I’ve been bullish on bonds.

On the other hand, I’m seeing some potential sources of inflation, especially as commodity prices seem to be on the rise. While China seems to get a lot of attention there, I think India might be a bigger contributor to commodity demand, one that could continue and push commodities much higher in the coming years.

But enough on inflation. And enough on the Fed — where the reality is the bond market is only moving Fed expectations just a little on every piece of data and Fedspeak (Chair Powell was incredibly dovish, again, last week). I think too much attention is being paid to where inflation has been and to the Fed.

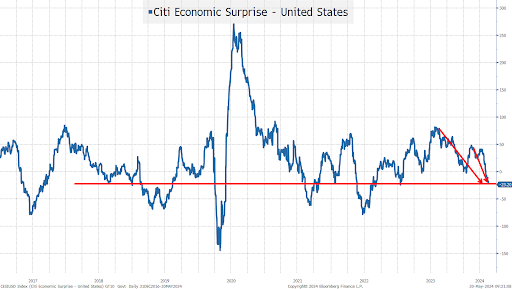

Let’s go back to the Citi economic surprise index, which continues to decline. Economic data are missing expectations, which has been helping bonds, which in turn seems to be helping stocks, but I’m not sure how long that can continue.

All that we can do is add to that argument today.

We have earnings from Nvidia NVDA out on Wednesday night. We all know, at this stage, that AI is all the rage. That every company is trying to incorporate AI into their process — or calling anything from machine learning, advanced regression, to simple calculations AI, to hop on that bandwagon.

We know that companies are paying up for chips that are in short supply relative to their demand. There seems to be almost no doubt that Nvidia's report (and outlook, which they have been providing recently in more detail than they once did), will be good. But good enough to support the current market cap?

I expect some weakness into earnings as bulls get nervous.

China

I continue to like Chinese stocks. iShares China Large-Cap ETF FXI and KraneShares CSI China Internet ETF KWEB both outperformed U.S. equities by an incredibly wide margin last week — up over 5% and 7%, respectively, on the week.

As China tries to build their brands and sees their economy stabilize, we could see more of a run. I’ve trimmed my position a bit (and so far regret it), and will probably add on any pullback.

Muni Closed-End Funds

I have been re-allocating my portfolio of late. Trimming a tiny bit of risk.

In general I’ve been selling some funds where the discount to NAV has shrunk — even some BlackRock ones, where they are facing outside pressure from the likes of Saba. (For full disclosure, I have been a closed-end fund board nominee on behalf of Saba in years past, prior to joining Academy Securities.)

I’ve been adding Blackrock funds where the discount to NAV is still in the “normal” range, as I think they too could benefit from the discount to NAV shrinking as BlackRock navigates the current environment of shareholder actions.

At the time of publication, Tchir was long FXI, KWEB and muni closed-end funds.