I Bought Pfizer After $1 Billion Move Points to Turnaround

A major investment in the pharmaceutical giant and a change in leadership suggest now could be the time to buy in.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

A ray of hope? Maybe.

Long-time readers know how I love to jump on the bandwagon when activist investors play the game that they play. Nelson Peltz of Trian Partners is one of my heroes. Do I know anything about his politics? No. Do I even know whether or not he's a good guy? No. What I do know is that, usually, when he shows up in a name I'm already in, I make money. Same goes for a number of higher-profile activist investors.

If I can't be in the stock ahead of any kind of announced investment, I try to jump in shortly thereafter if the stock has not moved much and looks to me to be undervalued. By that, I mean that the company behind the stock could possibly benefit from the input directed and pressure placed upon current management at said firm. Is anything a sure thing? In the real world, there is no such thing. That said, activist money can create for the smaller investor/trader an educated opinion and that's a whole lot better than pouring "alpha-bits" cereal into a bowl, looking for trade ideas.

New News

The news broke on Sunday night. A Wall Street Journal report hit the wire that activist investor Starboard Value had already taken a roughly $1 billion stake in pharmaceutical giant Pfizer PFE.

I know, Pfizer has a tough reputation with the anti-COVID vaccine crowd. I took the jab a few times myself in the hopes that it would cure me of my long COVID, which is a real thing, and though I was feeling somewhat better within eight months, and much, much better within two years, there are some symptoms (such as high blood pressure and lactose intolerance) that appeared with COVID and linger to this day. I haven't been jabbed since 2021 and I don't think too many other folks have, either.

Pfizer's sales and cash flow improved dramatically during the pandemic as the U.S. government rushed funding into finding a vaccine of vaccines and then continued to push the vaccines long after it was believed by most of the populace that it did not protect very well against transmitting infection and that what protection afforded by the shots was short-lived.

What we think we know is that Starboard is likely to seek a turnaround at Pfizer as the stock has struggled, especially since the COVID gravy train slowed down, but no specifics have been revealed. Additionally, under CEO Albert Bourla's leadership, the firm has relied upon expensive acquisitions in the attempt to buy growth that the firm was not producing organically.

Why an Activist Investor?

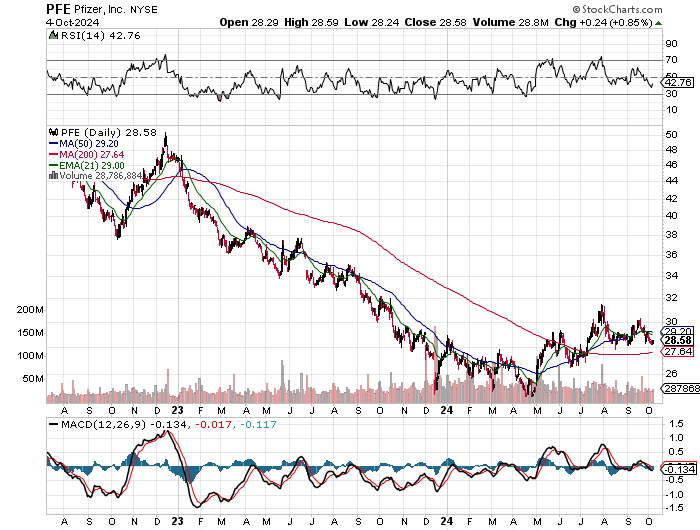

2023 was a fairly lousy year for Pfizer shareholders. The shares stabilized in 2024, but made very little progress in recovering.

What makes this push into Pfizer truly interesting, though, is that the activist investor has recruited two high-level and formerly successful Pfizer executives to support its turnaround cause.

Starboard has brought in former CEO Ian Read, who served in that role from 2010 to 2018. The shares doubled in value over that time frame. Along with Read came Frank D'Amelio, who served as Pfizer's CFO from 2007 to 2021. So, he and Reed are obviously comfortable with each other and could stand ready to lead, advise or, if need be, step in.

I bought an entry-level stake in PFE very early on Monday morning. I was piqued at seeing the initial story, but once I read that Ian Read was a player, so was I.

Earnings

Pfizer will report in about three weeks. Wall Street is looking for an adjusted EPS of $0.59 (or a GAAP EPS of $0.28) on revenue of $14.9 billion. Interestingly enough, results like this would be up from an adjusted EPS of $-0.17 a year ago, while reflecting 13% sales growth, so maybe Starboard is sniffing out a positive turning point for the business that has not yet been visible in the share price.

The stock trades at ten-times forward-looking earnings, so it is cheap enough. That said, though, operating and free cash flows had gone from positive to negative, and the balance sheet is pretty messy. Current liabilities outweigh current assets, while the debt-load simply dwarfs the firm's cash position. This is a trade, not an investment. Understand that. Despite a beefy dividend yield of 5.88%, there is a lot of work to be done to get this company back on sound fundamental footing. Do not become emotionally involved.

The Now

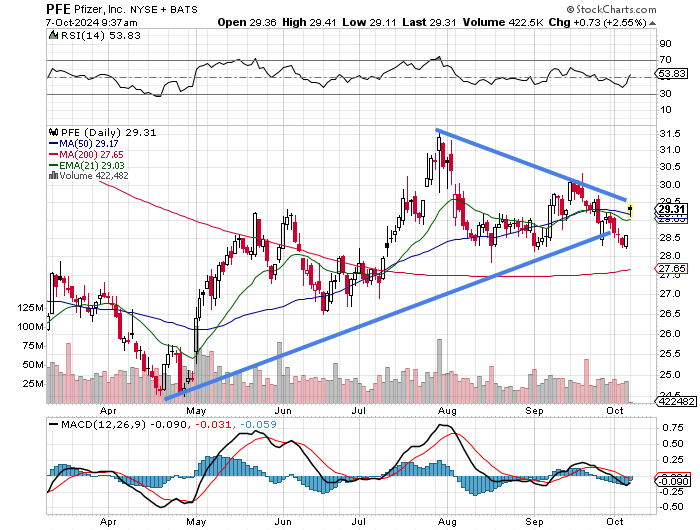

Readers will see that PFE has developed a pennant pattern that appears to be closing. The upper trendline only goes back to late July, but the lower trendline is about six months long.

What do we know about closing pennant patterns? They can often move violently in one direction or the other when they do close. Does the involvement of an activist investor and a former CEO who had a decent run increase the odds that the move will be higher? I am willing to bet a small amount on it. Perhaps more than a small amount if the shares stick around for a while.

At the time of publication, Guilfoyle was long PFE equity.