My New Price Target for Broadcom Following Stock Split Announcement

The semiconductor giant announced a 10-for-1 stock split and I'm offering new guidance after taking a closer look.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I had a darned feeling but also felt that I was exposed enough to the revolution in generative artificial intelligence when a little voice suggested that Broadcom AVGO might be a strong candidate for a stock split.

Well, there are no woulda, coulda, shouldas in baseball, nor in the racket we all chose to make our living. Oh well, c'est la vie, and we move on. Still, I think Broadcom deserves a "wow" at a minimum for that performance last night. Rock and roll.

For the firm's fiscal second quarter, Broadcom posted an adjusted EPS of $10.96 (GAAP EPS: $4.42) on revenue of $12.487 billion. The lion's share of the adjustments were made for the purposes of share-based compensation expense. These top- and bottom-line results both beat Wall Street's expectations, while that revenue print was good for year-over-year growth of 43.1%. This was a second consecutive quarter of 40%-plus annual growth.

Additionally, the firm announced a 10-for-1 stock split that will commence with the opening of business on July 15, 2024. This, along with the strong quarter reported and the strong guidance provided, has put the shares in overdrive since Wednesday evening.

Operations

Revenue grew 43.1% to $12.487 billion. Within that number, sales of products increased 6.7% to $7.192 billion, while sales of subscriptions and services increased a whopping 165.8% to $5.295 billion. Cost of revenue increased by 80% to $4.711 billion, leaving a GAAP gross profit of $7.776 billion (+27.2%) on a GAAP gross margin of 62.3%. On an adjusted basis, gross margin printed at $9.518 billion (+44.1%) on a gross margin of 76.2%.

Operating expenses grew 128.3% to $4.811 billion, leaving a GAAP operating income of $2.965B (-26%) on a GAAP operating margin of 23.7%. Once adjusted, operating income printed at $7.146 billion (+32%) on an operating margin of 57.2%. That's some sizable adjustment. Wow. After accounting for interest, taxes and other income/losses, GAAP net income hit the tape at $2.121 billion (-39%), which works out to an EPS of $4.42. Adjusted, net income printed at $5.394 billion (+20.2%), which works out to an EPS of $10.96.

Gee whiz. No wonder these guys adjust for stock-based compensation, which for a mature firm, should be recorded as an ordinary operating expense. It's the difference between non-GAAP net income growth of 20.2% versus GAAP net income growth of -39%. Yikes.

Segment Sales

- Semiconductor solutions experienced 6% sales growth to $7.202 billion, as its share of firm-wide revenue generation decreased from 78% a year ago to 58%. Networking was strong (+44% on AI-related sales, while wireless grew at a pedestrian pace. Server and storage, broadband and industrial all experienced contracting year-over-year sales.

- Infrastructure software experienced 175% sales growth to $5.285 billion, as its share of firm-wide revenue generation increased from 22% to 42%. This segment included a contribution of $2.7 billion from what used to be VMWare, up from $2.1 billion sequentially.

CEO Hock Tan on AI

CEO Hock Tan did comment on AI several times last night.

"Talking of AI accelerators, you may know our hyperscale customers are accelerating their investments to scale up the performance of these clusters," he said. "And to that end, we have just been awarded the next-generation custom AI accelerators for these hyperscale customers of ours."

"Networking these AI accelerators is very challenging, but the technology does exist today," Tan added. "In Broadcom, with the deepest and broadest understanding of what it takes for complex, large workloads to be scaled out in an AI fabric. Proof in point, seven of the largest eight AI clusters in deployment today use Broadcom Ethernet solutions."

On Competing with Nvidia (NVDA)

Vivek Arya (a five-star analyst at Bank of America) said: "Hock, I would appreciate your perspective on the emerging competition between Broadcom and NVIDIA across both accelerators and Ethernet switching."

Tan responded: "We don't even think about competing against them in that space, not in the least. That's where they're very good at and we know where we stand with respect to that. Now what we do for very selected or selective hyper-scalers is, if there's a scale and the skills to try to create silicon solutions, which are AI accelerators to do particular very complex AI workloads. We are happy to use our IP portfolio to create those custom ASIC AI accelerator(s)."

Guidance

For fiscal full year 2024, Broadcom increased its outlook for revenue generation from prior guidance of $50 billion to $51 billion. Full-year EBITDA is projected at 61% of revenue, up from prior guidance of 60%. These numbers include a full contribution from VMWare.

Fundamentals

For the quarter reported, Broadcom generated operating cash flow of $4.58 billion. Out of this number came capex spending of $132 million, leaving free cash flow of $4.48 billion. Out of that number, the firm paid shareholders cash dividends of $2.443 billion, and repurchased $1.548 billion worth of shares for tax withholding purposes related to share-based awards.

Glancing at the balance sheet, Broadcom ended the period with a cash position of $9.809 billion and inventories of $1.842 billion, putting current assets at $25.302 billion. Current liabilities add up to $20.171 billion including debt of $2.426 billion that will come due this year. That leaves the firm a current ratio of 1.25 and a quick ratio of 1.16. Solid. Not spectacular. Passes muster.

Total assets amount to $175.211 billion, including goodwill and other intangibles that add up to an incredible $143.28 billion. At 81.8% of total assets, this is almost absurdly high. I would definitely prefer to see a much larger portion of the firm's total assets be tangible in nature. Total liabilities less equity comes to $105.25 billion including another $71.59 billion in longer-term debt. I am sure that this longer-term debt came with lower interest rates than would be available now. That said, that much debt versus really so little cash and so few tangible assets is certainly cause for some concern. I don't know... maybe slow down the stock-based compensation and get to work on this balance sheet. Gee whiz. You would think that someone on Wall Street would mention this. It certainly detracts from what was a great quarter.

Wall Street

Since these earnings were reported last night, I have come across 18 highly-rated (four-plus stars at TipRanks) sell-side analysts that have opined on AVGO. Among these 18 analysts, there are 17 "buy" or buy-equivalent ratings and one "hold" rating. Two of our "buys" have not set target prices, leaving us with 16 of those to work with. The average target price across the remaining 16 analysts is $1,890.94 with a high of $2,050 (Blayne Curtis of Jefferies) and a low of $1,500 (Hans Mosesmann of Rosenblatt Securities). Once these two are omitted as potential outliers, the average target across the other 14 rises to $1,907.50.

My Thoughts

It's all kind of perplexing. A great quarter, strong guidance, a 10-for-1 stock split, part of the AI revolution.

In every way, Broadcom seems to be cooking with gas. Yet, the firm has this balance sheet, that to put it kindly, no one would brag about. It's correctable. The cash flows are there. The stock-based compensation is enormous. This could be done without reducing the $21 per year per share dividend. It's a shame, but I now complete writing this article a lot less impressed than I was at the start.

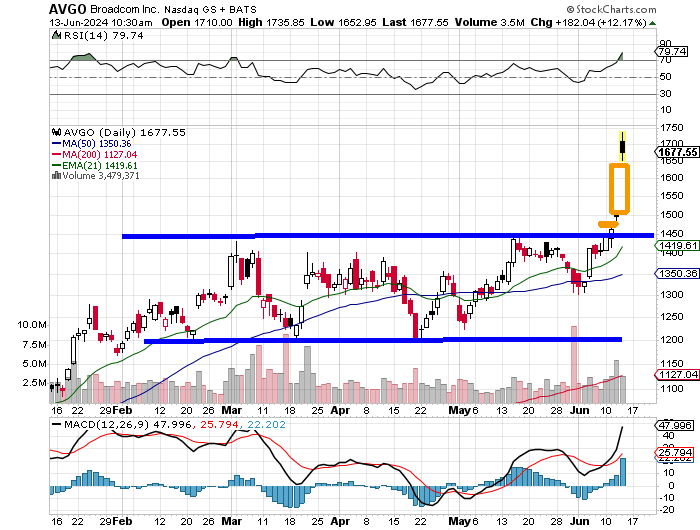

The stock has soared over the past two sessions, breaking out of a basing period of consolidation with a $1,445 pivot. In doing so, the stock has left two unfilled gaps in its wake that would need a trade as low as $1,465 to both fill. Relative strength has crossed over into overbought territory, as several components of the daily MACD appear to have gone parabolic.

Yes, I do think that AVGO will remain strong through the split. I think the growth in the AI and VMWare parts of the business are impressive. That said, I think for me, this would be a trade more than an investment at this time. My target price based on that pivot and this action would be $1,734.

At the time of publication, Guilfoyle was long NVDA equity.