Dramatic Improvement for This Small-Cap Stock With Potential Ahead

After a hard sell off, this stock has reacted favorably to increased liquidity and the market's rotation.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I received a request from a reader to update B&G Foods BGS, which we last focused on here back on May 15, 2024, a week after the somewhat troubled, but high-dividend paying small-cap stock that trades for under $10 per share had released its first quarter financial results.

Readers may recall that those results did not impress. For that period, the firm posted an adjusted EPS of $0.18 (GAAP EPS: $-0.51) on revenue of $475.22 million. That sales print reflected a year-over-year contraction of 7.1%. The firm had made adjustments for a goodwill impairment of $70.58 million and $14.389 million for the tax impact of that adjustment. What it all meant was that a GAAP net income/loss of $-40.2 million was adjusted to $14.4 million. Adjusted EBITDA for that period was reported at $75 million, which was down 8.9% from the year ago comp.

Coming Earnings

Back in May, B&G Foods cut full year guidance across several metrics. Net sales expectations were taken down to $1.955 billion to $1.985 billion from $1.975 billion to $2.02 billion. Adjusted EBITDA was also revised down to $300 million to $320 million from $305 million to $325 million, while adjusted EPS also took a haircut. What was $0.80 to $1.00 had become $0.75 to $0.95.

B&G will release the firm's second quarter numbers on or around August 6, 2024. Wall Street is looking for GAAP profitability this quarter that with adjustments rises to $0.10 on revenue of about $438 million. That would be down from the year ago comps of $0.15 on $465.64 million.

One Thing We Do Know

We do know that in June 2024, B&G Foods priced an offering of $250 million aggregate principal amount of 8% senior secured notes due 2028. The new notes were issued at a price of 100.5% plus accrued and unpaid interest from March 15, 2024. The firm said at that time that it expected to reduce the size of its previously announced proposed amended tranche B term loans under its senior secured credit agreement from $600 million to $450 million aggregate principal amount.

Net proceeds from the offering were supposed to be a little better than $247 million. Those proceeds were intended to be used to repay a portion of B&G's revolving credit loans and tranche B term loans under the senior secured credit agreement.

Balance Sheet

I am interested in seeing how that offering and the business in general have impacted the balance sheet when reported in early August. Readers may recall that B&G Foods ended the first quarter with a cash position of just $42.46 million, but inventories of $560.589 million and current assets of $785.321 million. Current liabilities added up to $244.235 million, including $22 million in short-term debt. That left the firm at that time with a quite robust current ratio of 3.22 and a quick ratio of 0.92, which is not that bad at all given the nature of the business and the fact that the inventories have a shelf life.

Total assets amounted to $3.361 billion, including $2.171 billion in goodwill and other intangibles. That was almost 65% of total assets, which I did and do find this concerning. Total liabilities less equity came to $2.579 billion, including long-term debt of $2.014 billion, which will have grown some. This was obviously not a great balance sheet. Yes, the firm is profitable on an adjusted basis. The current situation is neat and tidy. The longer-term health of the balance sheet is obviously going to be in question going forward as the majority of the assets are intangible and debt outweighs cash quite dramatically.

My Thoughts

After selling off hard, the stock has reacted favorably to the increased liquidity mentioned above as well as the recent rotation out of mega-cap tech and into the unloved, which includes small caps. Readers may also remember from that note back in May that Stephen Sherrill, who is a director at the firm, had purchased a chunk of stock after those Q1 earnings had been released. We took that as a positive.

Last week, Michael Lavery of Piper Sandler, who is rated at four stars (of five) at TipRanks, reiterated his "hold" rating on BGS, but did take his target price down to $8 from $9. On the bright side, since those most recent earnings were released, four other highly-rated sell-side analysts have placed an average target price of $9.50 on the shares.

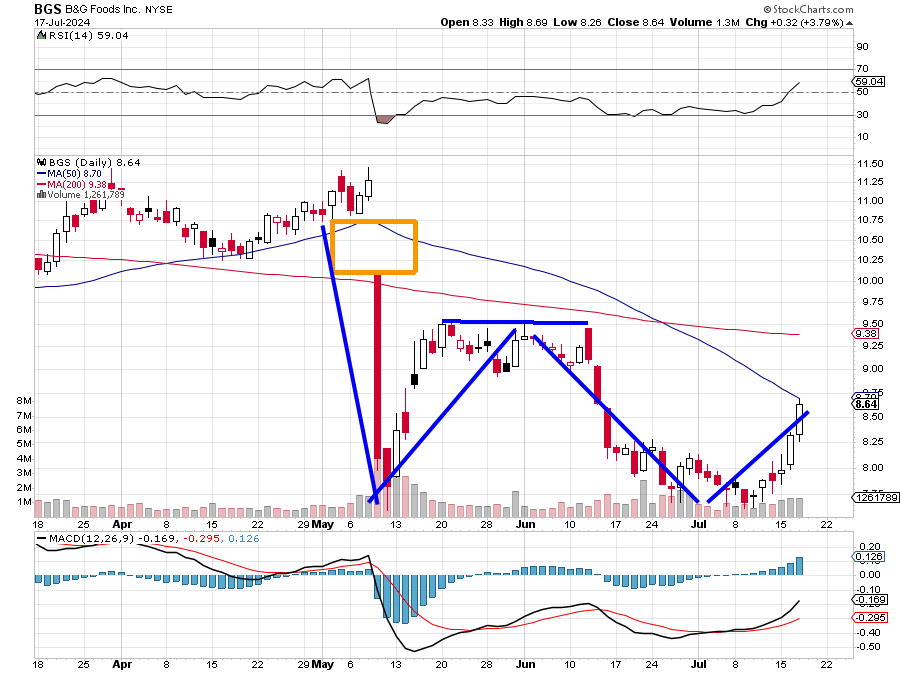

Readers will see that, after that last earnings release, the stock has developed a double bottom pattern with a $9.70 pivot. That promises nothing as the daily MACD is still postured bearishly, but relative strength has improved dramatically. If the stock can take and hold that pivot, a target price of $11.50 is not out of the question.

Oh, did I fail to mention that BGS $0.19 a quarter just to stick around? That's a dividend yield of 8.8%. Is the dividend safe? They last cut it in 2022. No, it's probably not safe, but for now, it's a reason to hang on to the shares, at least for a while.

At the time of publication, Guilfoyle had no positions in any securities mentioned.