AT&T Shows Signs of Improvement, But the Problems Are Massive: Here's the Trade

The firm is still driving exceptional free cash flow, which is its saving grace.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Retail investor favorite AT&T T released the firm's fourth quarter results on Wednesday morning.

For the three month period ended December 31st, AT&T posted an adjusted EPS of $0.54 (GAAP EPS: $0.30) on revenue of $32.022B. The adjusted earnings print fell 11.5% from the year ago comparison while also falling two cents short of consensus view. The revenue number both beat Wall Street and was good enough for year over year growth of 2.2%. The adjustments made were primarily made for an actuarial remeasurement of pension plan assets and obligations as well as restructuring and impairment charges.

Wireless postpaid phone net additions for the fourth quarter printed at 526K, which was well above expectations for 490K. Churn held at 1.01%. Remarkably, fiber internet additions amounted to 273K, marking 16 consecutive quarters (4 years) with greater than 200K net adds.

Operations

As revenue was busy growing 2.2%, total operating expenses decreased by a whopping 49%, showing that AT&T management is serious about being disciplined, to $26.751B. The lion's share of the reduction came from a near 100% drop in impairment and restructuring costs. Operating income improved to $5.271B from the year ago comp of $-21.197B.

After accounting for taxes, interest, non-controlling interests, and dividends for preferred stock, net income attributable to common shareholders printed at $2.135B, up from $-23.571B. This took GAAP EPS to the above mentioned $0.30 from the year ago comp of $-3.20.

Segment Performance

Communications drove operating revenue of $30.797B (+1.4%), producing operating income of $6.608B (+0.5%).

- Mobility drove operating revenue of $22.393B (+4.1%), producing operating income of $6.608B (+6.2%).

Service drove operating revenue of $16.039B (+3.9%).

Equipment drove operating revenue of $6.354B (+4.7%).

Service & Equipment produced operating income of $6.214B (+6.2%).

Mobility operating margin came to 27.7%, up from 27.2%.

- Business Wireline drove operating revenue of $5.052B (-10.3%), producing operating income of $165M (-69.4%).

Service drove operating revenue of $4.873B (-11.0%).

Equipment drove operating revenue of $179M (+10.5%).

Service & Equipment produced operating income of $165M (-69.5%).

Business Wireline operating margin came to 3.3%, down from 9.6%.

- Consumer Wireline drove operating revenue of $3.352B (+3.8%), producing operating income of $229M (+21.8%).

Broadband drove operating revenue of $2.7B (+8.3%).

Legacy Services drove operating revenue of $361M (-12.8%).

Other drove operating revenue of $291M (-9.9%).

Broadband, Legacy & Other produced operating income of $229M (+21.8%).

Consumer Wireline operating margin came to 6.8%, up from 5.8%.

Latin America drove operating revenue of $1.09B (+26.6%), producing operating income/loss of $-43M (up from $-79M).

- Wireless Service drove operating revenue of $671M (+15.9%)

- Wireless Equipment drove operating revenue of $419M (+48.6%).

Latin American operating margin came to -3.9%, up from -9.2%.

Guidance

For the coming full year, AT&T expects to see revenue grow close to 3%, while broadband revenue grows 7% or more. Adjusted EBITDA is seen growing about 3%. Capital investment should be in the $21B to $22B range, leaving free cash flow of $17B to $18B.

Adjusted EPS for the full year is expected to print in between $2.15 and $2.25. This projection takes into account a $0.17 per share depreciation expense from the open radio access network transformation as well as another $0.15 per share in aggregate related to amortization, pension and DIRECTV expenses. In 2025, a year from now, AT&T projects adjusted earnings growth.

Fundamentals

For the full year, AT&T generated operating cash flow of $38.314B (+7%). Free cash flow printed at $16.8B after a fourth quarter contribution of $6.4B. This 2023 total exceeded 2022 FCF by $2.6B. For the full year, the firm paid cash dividends of $8.136B to shareholders and paid down more than $12B worth of long-term debt. That's a positive, but the firm is a long way from being out of the financial woods.

Glancing over at the balance sheet, AT&T ended the quarter and year with a cash position of $6.722B and inventories of $2.177B. That left current assets of $36.548B. Current liabilities add up to $51.127B including $9.477B in debt maturing in under a year. That leaves the firm with a current ratio of 0.71 and a quick ratio of 0.67. It does not take a genius to see that these ratios remain unacceptably weak. The firm also does not have enough cash on hand to take care of its short-term debt and will likely have to roll over a portion of that debt at higher interest rates. Cutting the dividend again would be the only way around that.

Total assets amount to $407.06B including $73.137B in goodwill and other intangibles. At 18% of total assets, that would not be so bad if the rest of the balance sheet was in good shape, which is not the case. Total liabilities less equity comes to $287.645B including $127.854B in long-term debt, which is just daunting.

My Thoughts

AT&T is certainly showing signs of significant improvement. That said, the problems were so massive that they still exist and they're still massive. The firm is still driving exceptional free cash flow, which is its saving grace. I know it does not want to as it would drive many shareholders away, but it would help correct the horrendous balance sheet more quickly if the firm could "just" return less cash to shareholders and try to pay down large chunks of debt on the regular.

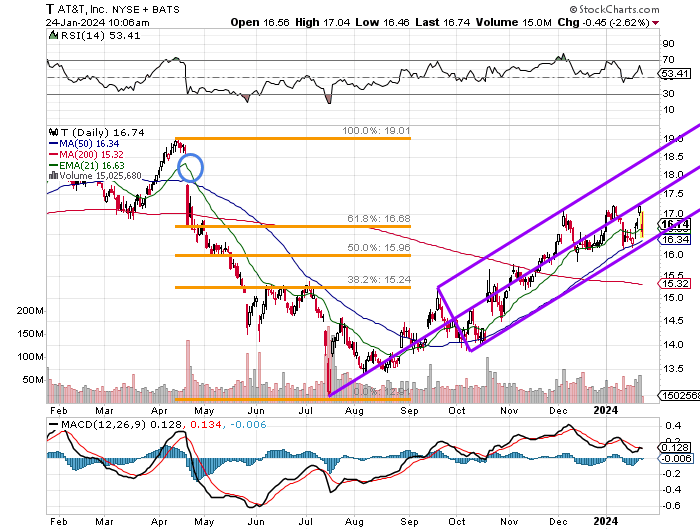

I understand being long AT&T for the dividend yield. I can not see being long this name for fundamental reasons. Technically, there is some hope.

Readers will see that AT&T suffered a steep drop this past April and in doing so left a large unfilled gap that would require $19.61 to fill. The stock's rebound that began in mid-July hit some turbulence at a rough 61.8% Fibonacci retracement of the April into June selloff.

In doing so, the stock fits neatly into an Andrews Pitchfork model covering the period. The stock is now testing the lower trendline of that model after being rejected at the central trendline just a few days ago.

Now, I know some of you are going to hang on no matter what for the almost 6.5% yield. That said, should the stock not make a run at that unfilled gap, and break through the bottom of this model, the 20 day SMA (simple moving average) will come into play. The last time AT&T lost its 200 day SMA, the stock dropped 27%.

Keep that in mind, and if you do get that gap fill up in the $19's, take something off of the table.

At the time of publication, Stephen Guilfoyle had no position in the securities mentioned.