As This Stock Gets 'Thrown Out,' Is It Worth a Dumpster Dive?

Anywhere Real Estate being cast out of the S&P 600 'cool kids' club has me doing some thinking.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Investors may have read the "good" news on Friday night. Maybe, if they were in hibernation all weekend, they found out Monday morning. The announcements were made last Friday for changes to be made this Friday.

CrowdStrike CRWD, KKR KKR and GoDaddy GDDY were all elevated to the S&P 500. Sorry, Palantir PLTR fans, believe me, I do think that your day is coming. The firm, honestly, is not ready yet. Pass them over next year and I think we'll have some legitimate beef.

Moving out of the S&P 500 will be Robert Half RHI, Comerica CMA and Illumina ILMN. Illumina will be demoted to the S&P MidCap 400, while Robert half and Comerica will be relegated all the way to the S&P Smallcap 600.

Coming out of the S&P 600 will be Anywhere Real Estate HOUS and Adtran ADTN, which are both apparently being cast completely out of the "cool kids" club. Right now, I'm doing some thinking and I'm thinking about Anywhere Real Estate.

Let us begin.

Who Are These Guys?

Anywhere Real Estate is a New Jersey-based integrated residential real estate services provider. The firm operates its businesses through three operating segments.

-- The Anywhere Brands segment franchises a portfolio of brokerage brands including Better Homes and Gardens Real Estate, Century 21, Coldwell Banker, Coldwell Banker Commercial, Corcoran, ERA and Sotheby's International Realty. The segment provides for global relocation services and lead generation.

-- The Anywhere Advisors segment operates full-service real estate brokerage services in many U.S. metropolitan areas.

-- The Anywhere Integrated Services segment provides title, escrow, and settlements services largely in support of residential real estate transactions.

It's Been Rough

On April 25, Anywhere Real Estate reported its first-quarter financial results. The firm posted a GAAP loss of $0.91 per share on revenue of $1.13B. Both of these numbers fell short of Wall Street's expectations, while sales growth was flat from the year ago period and free cash flow printed at -$145M. This was the second consecutive non-profitable quarter for Anywhere Real Estate, which is likely why they were shown the door at S&P indexes.

The thing is that the firm at that time, projected adjusted operating cash flow for 2024 to end up being moderately positive. Anywhere Real Estate also expects to realize more than $100M in cost savings this year but acknowledged an anticipation of more than $100M in one-time payments that will have to be made at some point this year related to a class action litigation settlement and a legacy California tax matter.

Still, It's Not All Bad

Anywhere Real Estate is expected to post its second-quarter results in late July. Wall Street expectations are for adjusted EPS of 0.40 or GAAP EPS of $0.36 on revenue of $1.68B, which would be good for year-over-year growth of 3.4%.

For the full year, the Street is looking for an adjusted loss per share of $0.15, but an improvement to EPS $0.58 for 2025. Consensus is for full-year revenue growth of just about 3% this year, but 8% next year. In short, the business is going through a difficult period that analysts do see improving.

More Stocks Under $10:

- I've Got My Eyes on an Apparel Group After Surprise Profit Report

- This Iconic Retail Chain Got Rocked, But Absurd Yield Is Still Possible

- Time to Get Fired Up About Rocket Lab

Fundamentals

Sure, we know free cash flow went to the dark side for the first quarter. That said, for the trailing 12 quarters at that time, HOUS generated operating cash flow of $178M and free cash flow of $106M. That's free cash flow of $0.96 per share. Not really too bad.

At quarter's end, the firm had $111M in cash on its balance sheet and current assets of $597M. This is where it gets dicey. Current liabilities added up to $1.475B, including $749M in short-term debt and longer-term debt due to mature in less than a year. This is problematic, leaving it with a current ratio of just 0.40 and in a sport where it will have to refinance a lot of debt at less than favorable terms.

Total assets amounted to $5.799B, which is mostly (70%) goodwill and other intangibles. Total assets less equity came to $4.219B, including $2.053B in long-term debt.

You get the picture. This balance sheet is pretty close to being a train-wreck.

My Thoughts

OK, the fundamentals are lousy. The stock trades at 15 times forward-looking earnings, but at less than 0.1 times sales and around 0.27 times book. There's a reason for that. That said, the firm can and should be GAAP profitable in 2025 if it can get that far.

About 12% of the float is held in short positions, so there could be some upward pop in this stock's future, if not as an investment, at least as a trade.

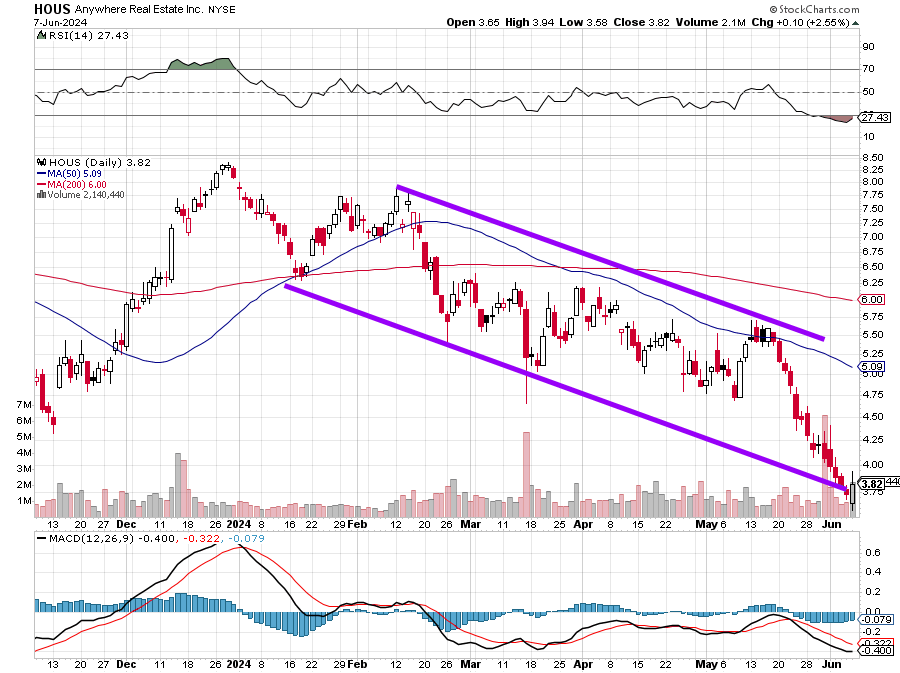

The stock is mired in a six-month long downward-sloping price channel. I am not thinking of buying any right now. Let it test and perhaps break that lower trendline as the S&P 600 gives this stock the boot.

In six weeks, when the company likely posts a positive quarter and gives some maybe not-so-awful guidance going into 2025, that's when the short interest may matter. What I am thinking of doing at these levels or lower (where the risk/reward proposition is not awful) is getting long a tranche ahead of those late July earnings for a trade as the shorts face a potential squeeze.

This is not a call for action. It's a heads up to put something that might be profitable in six weeks when it would not be on your radar, in the back of your head.

At the time of publication, Guilfoyle had no positions in any securities mentioned.