Ardmore Shipping Looks Like a Buy Ahead of Earnings

This dividend-paying small-cap could be offering a terrific discount.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Yes, I know, my (our?) favorite former "Stocks Under $10" portfolio holding, which is Palantir Technologies PLTR, will report this evening. On that note, while Palantir was one of that portfolio's greatest successes, the stock is now a member of the S&P 500, a long way from trading under $10 and a long way from being a small- or even a mid-cap stock. Our other SU $10 faves, Rocket Lab USA RKLB will report next week, while SoFi Technologies SOFI has already stepped to the plate for this season.

One other name that, while not trading under $10, certainly does qualify as a small cap, comes to us by way of reader request. Ardmore Shipping Corporation ASC is an owner and operator of product and chemical maritime tankers globally. The firm, headquartered in Bermuda, operates through a single business segment, transporting refined petroleum products and chemicals to the oil majors, as well as to chemical companies and traders. The firm operates a fleet of mid-sized tanker ships providing services to its clientele such as voyage charters, time charters and commercial pools. The firm's fleet count is currently 25 vessels

Earnings Due

Ardmore Shipping will report its fiscal third quarter financial results ahead of the opening bell this Wednesday. Some of you may have been up all night watching election results at that time. Expectations are for a GAAP EPS of $0.72 adjusted down to $0.57. That compares to $1.47 adjusted down to $1.13 for the second quarter and to $0.49 for the year-ago period both on a reported and adjusted basis. Consensus is for quarterly revenue generation of $66.1 million, which would be down more than 20% year over year.

The Fundies

For the second quarter, Ardmore generated operating cash flow of $48.4 million, out of which came capex spending of $43.6 million, leaving free cash flow at $4.8 million. The firm did pay out $13.8 million in cash dividends to shareholders. That looks sloppy at first, but it really was making up several quarters of much more robust free cash flow on lower levels of capex spending to its investors.

As of the end of the June quarter, the firm had a cash position of $47.4 million and current assets of $142.4 million. Current liabilities ran at $40.7 million, which included no debt that would mature over the next 12 months. That puts the firm's current ratio at a quite healthy 3.50. Once accounting for inventories of $13.2 million at the time, the quick ratio remained a beefy 3.17.

Total assets amounted to $742 million, which is mostly property. Total liabilities less equity came to $87.3 million, which did include $44.2 million worth of long-term debt. Seems like a lot? Actually, it's something the firm could have paid off out of cash at the time if it had to.

Two Weeks Ago...

Stifel Nicolaus, five-star rated (by TipRanks), downgraded this stock from a "buy" rating to "hold" while taking his target price down to $17 from $24. While that's not ideal, Jonathan Chappell of Jefferies, also a five-star rated analyst, still has a "buy" rating on the stock with a $26 target price.

My Thoughts

Though a small cap, Ardmore is profitable, generates positive cash flows and has a strong balance sheet. The firm also pays shareholders $1.52 per year per share just to stick around. That's a dividend yield of a stunning 10.83% that is not only largely sustainable... the firm has increased the dividend each quarter this year.

While that might mean that a dividend payout yielding 10% probably is not a sure thing, a healthy dividend is. It also reflects the fact that management is self-aware and responsible when doling out only what they can.

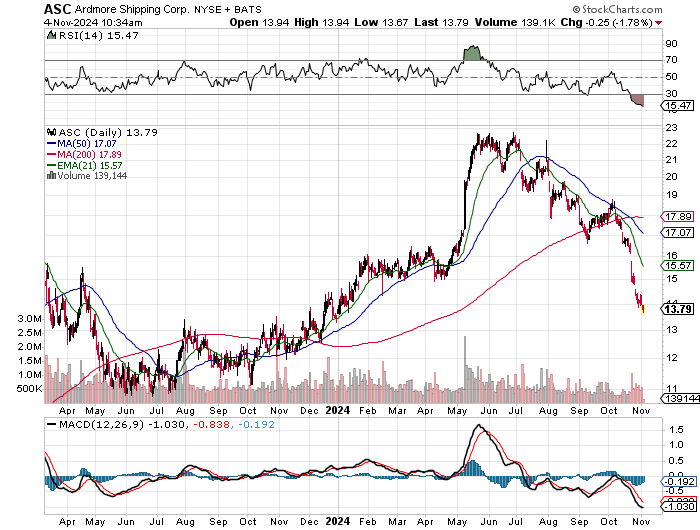

The stock is clearly in a state of free fall. It's kind of hard to write something logical based on what I see. The stock has retraced just about all of its 2024 gains and could have its sights set on its mid-2023 lows. The stock looks to have priced in some sort of cataclysmic event or something. Look at that RSI! Look at that daily MCD! Should Ardmore report something short of Armageddon this week, this may very well be a dividend stock that could have been had at a terrific discount. I think myself likely to pick some up ahead of Wednesday morning's release.

At the time of publication, Guilfoyle was long PLTR, RKLB and SOFI equity.