Against the Grain: This Is a Market Contrarian's Dream Setup

As the despair of the boom and bust commodity pattern is felt in growing regions, all the stars appear to be aligned for prices to firm up.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

So much for the commodity Supercycle.

A few years ago, grain markets such as corn, wheat, and soybeans were at, or near, all-time highs. Few fundamental analysts were willing to accept the prospects of high prices curing high prices; at the time, the world’s breadbasket, Ukraine, was under attack, and speculative money was flowing into the ag markets from investors desperate to hedge price inflation. A few years later, the despair of the boom and bust commodity pattern is being felt in growing regions.

The only good news is that low prices also cure low prices for producers, but the process takes much longer. Further, technology and scientific advances generally lead commodity prices to trade heavily more often than not. In other words, farmers are good at what they do and are only getting better. Nevertheless, we are approaching a scenario where all the bears have probably taken action. Simply put, the bearish news could be mostly priced in.

Corroborating our intuition to prepare for a trend reversal, market sentiment (particularly among producers) is gut-wrenchingly low, speculators are aggressively short, seasonality will soon turn bullish, the U.S. dollar has been plummeting, and we are nearing long-term chart support trendlines. This is a market contrarian’s dream setup. Obviously, there are no guarantees, but all the stars appear to align for prices to firm up.

Corn

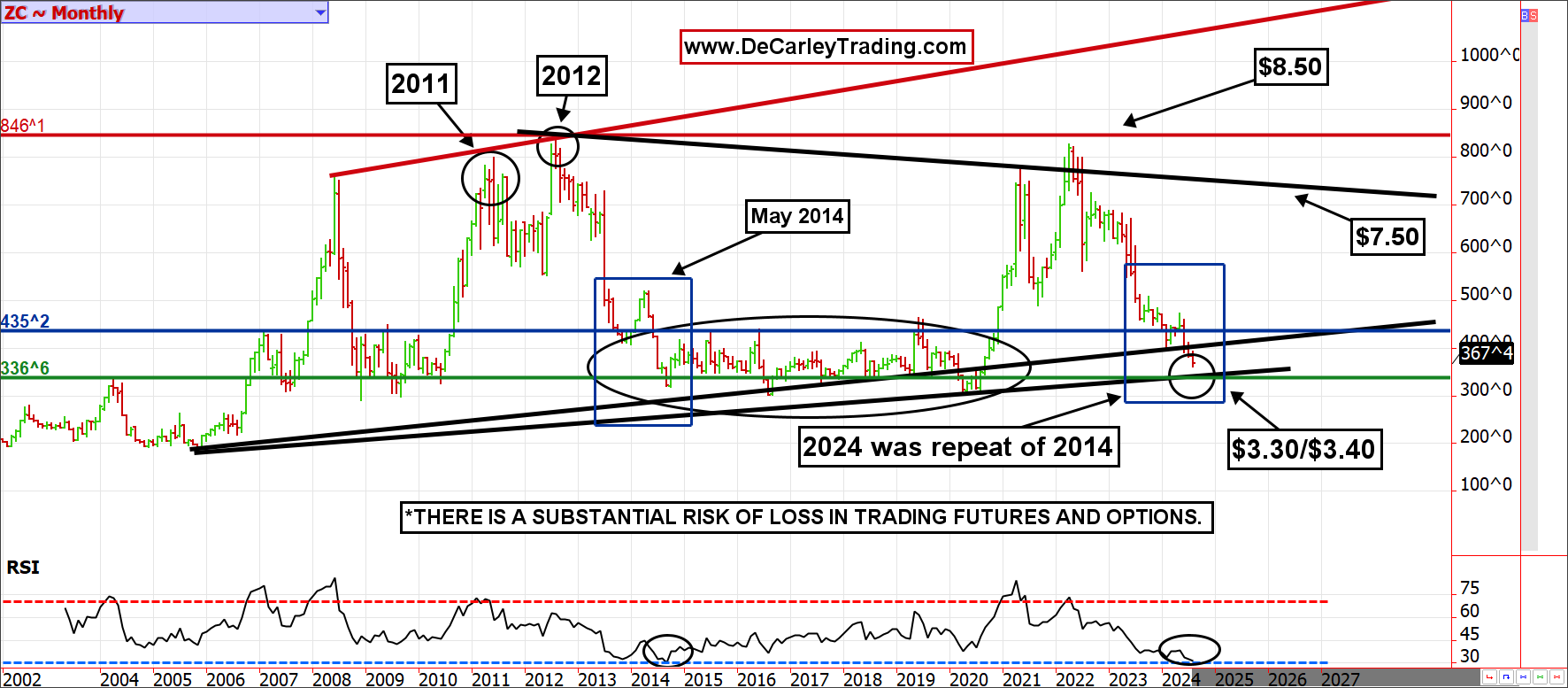

Let’s take a look at corn first. We have been unpopularly calling for $3.30 in corn. We believed the 2024 market would mimic the 2014 market, which is almost precisely what unfolded. In fact, the RSI (Relative Strength Index) is as oversold as it was in 2014.

Due to the time that has passed and the slow pace of the selloff, the trendline we have been watching is now closer to $3.40. Our analysis assumed this price would be seen on the old crop corn, not the new crop. We are obviously a little short of the trend line, but the cash market might make up for that after the First Notice Day of the futures contract.

Even so, we believe the vast majority of price weakness is behind us, and speculators should focus on looking for a reversal. Likewise, with ample time, producers can feel comfortable peeling off some of their hedges and/or re-owning via cheap call option purchases (March, May, or even July).

Soybean

Soybean futures, unlike corn, have successfully tagged their decade-long trendline on a monthly chart. While the jury is still out on whether or not support holds, we suspect it will. That does not mean we can’t see one more punch lower to retest lows or even overshoot lows by 30 to 40 cents to shake out weak longs, but the better trades are likely on the long side from here.

Wheat

Wheat has been the dog of the grain complex since topping out near $14.00 per bushel. While corn and soybean producers have been forced to endure one growing cycle of misery, wheat producers have felt the pain for two cycles.

There are several reasons for this, but sadly, the most plausible explanation is that the wheat ETF (Electronically Traded Fund) amassed unfathomable cash inflows when Russia invaded Ukraine. The unwinding of that position created a treacherous bear market, catching many traders off guard and leaving many farmers undersold. The underlying futures market simply couldn’t handle the newfound popularity of the ETF.

For those unfamiliar with them, commodity ETFs commonly pool investor money to buy futures contracts. The result of too many dollars chasing too few futures contracts (nobody wanted to take the other side of ETF buys) was a dysfunctional rally with several consecutive limit-up trading sessions (futures markets lock up when the daily maximum price move is achieved).

Bottom Line

The agriculture sector has suffered from intense selling pressure as the froth from two years of inflation spikes worked its way out of the system. Yet, in commodities, price trends are always temporary, and low prices, particularly with the perfect storm of bullish catalysts as described above, eventually lure buyers.

At the time of publication, Garner had no positions in any securities mentioned.