After Very Bad Miss, I'm Torn on GameStop

The video game retailer fell more than $100 million short of Wall Street expectations, but this stock might not be a lost cause.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Tuesday evening, GameStop GME, the troubled purveyor of video games as well as related hardware and collectibles released the firm's second quarter financial results.

For the three-month period ended August 3, 2024, GameStop posted an adjusted EPS of $0.01 (GAAP EPS: $0.04) on revenue of $798.3 million. The adjusted EPS print beat Wall Street by roughly a dime. However, the top-line print missed very badly, falling more than $100 million short of expectations and reflecting year-over-year contraction of 31.9%.

As investors in this name likely already know, the firm does not host a conference call related to its earnings releases and therefore is not subject to questions posed by the community of sell-side analysts.

Hardware and accessories accounted for 56.5% of sales, up from 51.3%, as software sales dropped to 26% of sales from 34.1%. Collectibles improved from 14.6% of sales to 17.5%. I know that collectibles have been a focus for the firm, but so has software, so this is a mixed sales split.

Operations

As sales contracted 31.9% to $798.3 million, the cost of those sales dropped 36% to $549.5 million. This left a gross profit of $248.8 million (-18.7%) as gross margin improved from 26.3% to 31.2%.

Operating expenses decreased by 16% to $270.8 million. That left an operating income/loss of $-22 million, down from the year ago comparison of $-16.6 million. After accounting for interest, other income/losses and taxes, GAAP net income/loss hit the tape at $14.8 million, up from $-2.8 million a year ago. This works out to $0.04 per fully diluted share, up from the year ago comp of $-0.01.

Fundamentals

For the period reported, GameStop generated operating cash flow of $68.6 million (up from $-109.1 million a year ago). Out of that came capex spending of $3.1 million (down from $10.1 million), leaving free cash flow of $65.5 million (down from $-119.2 million). The firm is obviously in no position to return capital to shareholders.

Turning to the balance sheet, GameStop is not in the rough shape you might think it is if you only watch financial television. The firm ended the quarter with a cash position of $4.204.2 billion and inventories of $560 million. That makes for $4,883.9 billion in current assets. Current liabilities add up to $783.6 million, including just $11 million in short-term debt. That works out to a gargantuan current ratio of 6.23. Many corporations thought of, as much healthier than GameStop stand with current ratios nowhere near anything like that. Even if the inventories are of questionable value (I don't know), assuming they are worthless, the firm's quick ratio currently stands at a very muscular 5.52.

Total assets amount to $5,536.3 billion. The firm includes no goodwill and no intangibles of any kind in that number. We appreciate that. Total liabilities less equity comes to $1.152.9 billion. This includes almost no (just $12.4 million) long-term debt. Don't tell the naysayers, but GameStop has one of the strongest balance sheets I have analyzed this earnings season.

News

In an SEC filing, the firm disclosed that, as part of its attempt to achieve sustained profitability, there is an ongoing effort to evaluate its assets and operations to determine which assets underperform and where there are redundancies. The firm continues to try to identify stores that might be candidates for closure and the firm continues to contract its footprint. A firm number for expected closures going forward has not yet been determined.

My Thoughts

I'm so torn. Not because this is a good business. It is not. Unless the firm can find out what works next, it faces what are likely insurmountable odds in turning the company around, given that it is still somewhat reliant on an industry that has evolved past the era of physical retail. That said, the firm is undeniably well managed. Cash flows are positive, and the balance sheet is top notch. I like to reward such an effort, but there has to be a business not just fighting a losing battle, but with a chance to grow.

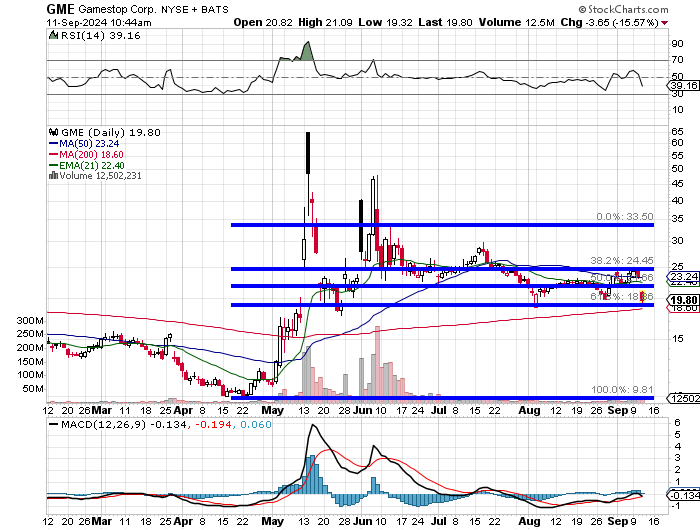

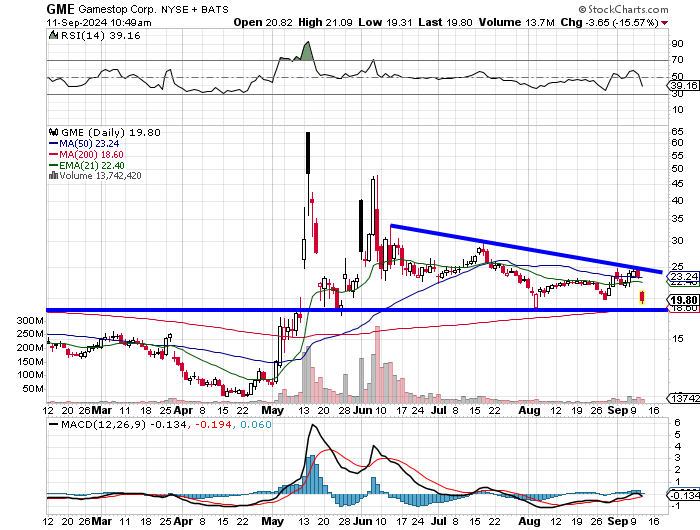

The Charts

If investors can omit the "Roaring Kitty" nonsense and not see the spikes of this past May and June, they will see that a high that may not have been skewed by the Kitty occurred on June 12, 2024. A Fibonacci model laid over the actions of this stock recognizing that high as "the high" of the cycle, shows that support has been found upon multiple occasions at a 61.8% retracement of that move. Let's look at this another way:

Readers will see that what has developed, is a descending triangle, which is considered to be a bearish pattern. The gap lower open this morning has placed the last sale below both the 50-day SMA and 21-day EMA. The shares seem likely to retest the above-mentioned Fibonacci level which is the support line for the triangle.

Both the reading for RSI and the daily MACD are weakening. What matters now is what happens at that support line, as it is running concurrently with the stock's 200-day SMA. A break of that line likely leads to sub $15 levels. At some point, a downsized business with a balance sheet like that and some level of positive cash flow will be investible. This stock is not a lost cause.

At the time of publication, Guilfoyle had no positions in any securities mentioned.