With $100 Billion Forecast, I'm Interested in Owning Oracle

The technology provider has popped and some intriguing comments by the founder has us looking for an opportunity to buy in.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Software and cloud technology provider Oracle ORCL popped overnight after the firm increased its guidance for revenue generation at its meeting for financial analysts.

At the meeting, Oracle lifted the firm's outlook for fiscal 2026 to $66 billion, which is above the $64.7 billion or so that Wall Street had penciled in. We are currently in what is, for Oracle, the second quarter of fiscal 2025. The firm also forecast that annual revenue generation could top $100 billion by 2029 or the end of the decade. Very confidently, CEO Safra Catz stated "Those numbers should not be a problem," to his audience.

Earlier This Week

Oracle reported the firm's fiscal first quarter results on Monday after the closing bell.

For the three-month period ended August 31, 2024, Oracle posted an adjusted EPS of $1.39 (GAAP EPS: $1.03) on revenue of $13.307 billion. The adjusted earnings print managed to beat Wall Street's expectations by about a nickel. That top-line number not only beat expectations but was also good for year-over-year growth of 6.8%. The adjustments made were made mostly for stock-based compensation expense and for the amortization of intangible assets.

The highlights of the release were growth in total remaining performance obligation of 53% to $99 billion, and Cloud Revenue (IaaS and SaaS) of $5.6 billion, which was up 21%. This included Cloud Infrastructure Revenue (IaaS) that increased 45% to $2.2 billion. On top of the earnings release, impactful deal news was announced that evening.

Oracle had signed a multi-cloud agreement with Amazon's AMZN AWS which would involve embedding Oracle's Exadata hardware and Version 23ai database software into Amazon's AWS cloud data centers.

The agreement will enable enterprise customers to connect data in their Oracle database to applications running on Amazon's cloud service. In return, AWS customers will get access to Oracle's database as soon as this month. A somewhat similar deal had already been struck with Alphabet's Google Cloud. The cooperation of two out of three of the nation's largest cloud services providers on top of already solid earnings and solid growth where it counts was exactly what the doctor ordered. ORCL took off on Tuesday morning and hasn't let up.

Anyone Else Catch This?

After CEO Safra Catz spoke during the call on Monday night, founder, chairman and CTO Larry Ellison spoke. The quotes of his are not all in line together, so listeners or readers had to piece the comments together to understand how aggressive the firm's leadership expects to be. Check these out:

From 162 data centers to 1,000 or 2,000 or more? That's the kind of stuff that the word "wow" was created for.

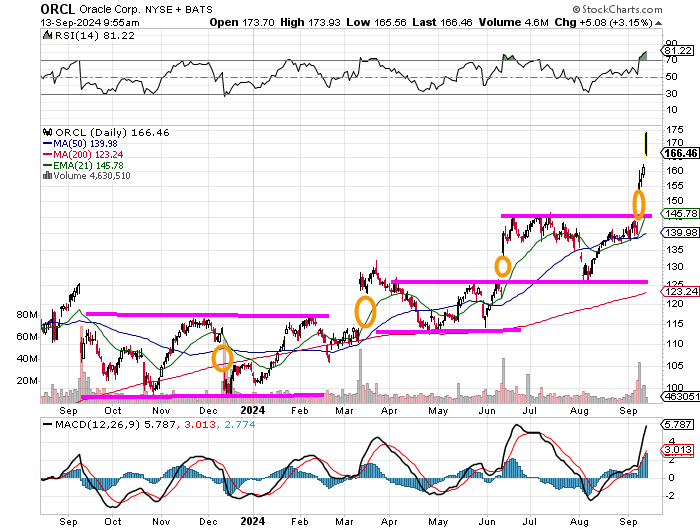

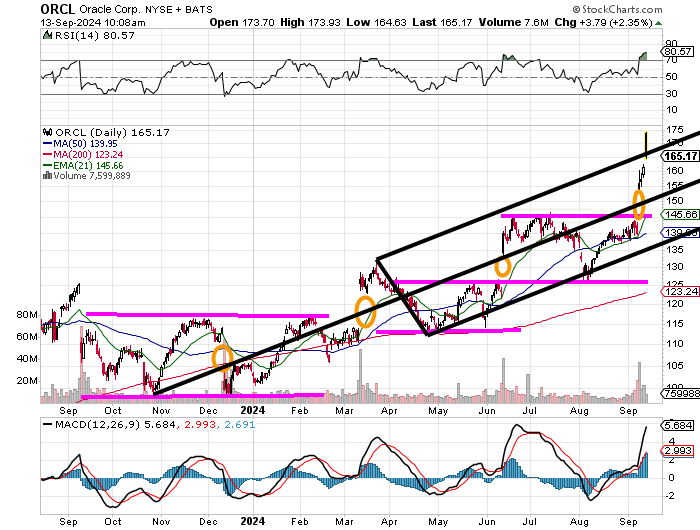

The Charts

Readers will see a repetitive pattern that has now been created for four consecutive reporting periods. Oracle has reported earnings that have created a "gap up or down" opening the next morning. The last three of these gaps have helped move the stock out of periods of what I see as basing consolidation (December was a gap lower) in March, in June and again this week. It's almost like a staircase. Can it hold this gap, which is kind of a double gap? In both prior cases, the gap had been filled ahead of the next reporting date.

Does that give pause to the idea of chasing this gap? I never like to chase anything, so yes. Is it smart to use history as a guide and wait for the stock to come in. I like to think that way, but over these past nine months, ORCL has never broken through established support.

The reading for relative strength looks to be technically overbought as well. Overbought readings in this stock's RSI have historically been temporary sell signals. That said, the daily MACD below the chart, is not overtly bullish. The 12-day EMA is now well above the 26-day EMA and the histogram for the nine-day EMA is now decisively above zero.

Now, I overlay an Andrews' pitchfork model over the entire rally going back to late October 2023. We see that almost everything in between that date and the present had been part of the existing trend. This morning, ORCL has broken through the upper trend line of the pitchfork. Should that line hold, ORCL could be off to the races. That said, a move back towards the central trend line would not completely surprise.

If I were interested in owning ORCL, and I think I am after Ellison's comments, I would rather get paid to wait than to pay $165-plus on Friday morning for an equity stake. Maybe this gets done by selling (writing) October 24, 2024, $155 puts for about $1.60 or selling (writing October 24, 2024, $150 puts for a rough $0.75 or some combination of both.

This way, if the stock comes in, I end up long at a discount that is further discounted by the aggregate premiums taken in, or if the stock never comes in, at least I got paid the premiums for my effort.

At the time of publication, Guilfoyle was long NVDA equity.