Weekly Roundup: Prepare to Be Selective

With some quiet weeks ahead, we'll make sure our portfolio is well positioned for the second half of the year.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

While all four major stock market indices moved higher this week, we saw a bit of a change with the Dow leading the pack, followed by the S&P 500, then the Russell 2000, with the Nasdaq Composite bringing up the rear. Some of that could be driven by profit-taking given the quarter-to-date and year-to-date moves in some of the meatier weightings found in the Nasdaq, such as Nvidia NVDA, Qualcomm QCOM and Apple AAPL that were still up more than 40%, 25% and 22% quarter to date, respectively. Those moves and others have had a wonderful impact on the portfolio’s performance.

We expected a relatively quiet week because of the midweek Juneteenth holiday, and average daily volumes suggested that was the case. Helping spur the market along was the week-over-week decline in the 10-year treasury yield that bottomed out near 4.22% before climbing back to finish the week near 4.26% following Friday’s Flash June PMI report from S&P Global.

That report followed the May reports for retail sales, industrial production and housing starts and showed a pickup in both the manufacturing and services economies compared to May. S&P’s findings also pointed to inflation pressures continuing to soften in June, a welcomed development. Continued job growth and real wage growth suggest we could see a rebound in consumer spending compared to the year-over-year gain of 2.0% for retail-only sales in May. With that in mind and because of our position in Mastercard MA, we’ll be focused on the May personal income and spending report out next Friday.

Because there are only a few second-tier economic data points ahead of that report and only a few earnings reports of consequence, we could see the market melt-up further to close out the final month of the current quarter. That same look at the calendar also tells us companies are entering their respective quiet periods as they begin to close their books for Q2 2024. While some companies may be holding investor events next week, the recent wave of investor conferences is over.

Next week, and the following one that includes the July 4 holiday, may be quiet ones for the market, but we’ll continue to focus on making sure the portfolio is well positioned as we move into 2H 2024 and beyond.

Catching Up on the Portfolio This Week

Because of the midweek holiday and the expected impact on trading volumes, we made no moves with the portfolio this week. The weak headline May housing starts report weighed on our shares of Builders FirstSource BLDR and Vulcan Materials VMC even though the non-seasonally adjusted painted a much stronger picture for housing activity. Friday’s non-seasonally adjusted data for May existing home sales did the same. As the dust settles on those reports, we’ll look to pick up some additional BLDR shares in the coming days. Other shares on our shopping list include Waste Management WM, Trade Desk TTD and Labcorp LH.

While some were perturbed by the May retail sales report, what we saw supported our shares of Amazon AMZN, PepsiCo PEP and Costco COST. Non-store retail sales continued to outpace overall retail sales during the month, while consumer spending at food service and drinking places softened over the last three months compared to the December 2023 to February 2024 period. While it may be a bit rearview mirror, data like that reaffirms our decision to exit McDonald's MCD shares back in late April at $274.80. And comparing Costco’s adjusted comp sales of 5.7% for May against the 2.0% gain for retail-only sales in May tells us the warehouse company continues to rack up wallet share.

When it comes to the shares of Lockheed Martin LMT, which climbed well ahead of the market this week, one of our focal points is the company’s backlog. A rising backlog indicates extended visibility, and this week a $2.27 billion win from NASA was more than a nice addition. The program is for developing three spacecraft and four options for additional spacecraft with an expected duration of 15 years for each aircraft. Remember, the catalyst we and others are waiting for when it comes to LMT shares is the resumption of F-35 deliveries.

This week we also learned Axon AXON and drone manufacturer Skydio will launch an end-to-end offering for drones in public safety, including a scalable drone-as-a-first-responder solution. While we like the drone revenue sleeve, it is the pull-through to the company’s cloud and services business. Weighing on Axon shares this week was the sale of 1,434 shares by President Joshua Isner, but we’d note that the sale was part of a 10b5-1 trading plan put in place in September 2023.

With our cash levels now back below 10% and barring any register ringing that would bring some additional cash into the fold, we will have to be selective with any next moves. As we prepare for that, we’ll be revisiting EPS expectations for the coming quarters relative to the S&P 500, but also noting which companies in the portfolio are entering their seasonally stronger times of the year.

This Week's Portfolio Videos and Podcasts

We cover a lot of ground during the week in our Daily Rundowns and the Portfolio Podcast. If you happened to miss one or more of them, here are some helpful links:

- Monday, June 17: "Our Roadmap for This Funky Trading Week"

- Tuesday, June 18: "Our Preferred Strategy for Harvesting Gains in the Portfolio"

- Thursday, June 20: "Why We Like Companies With These Characteristics"

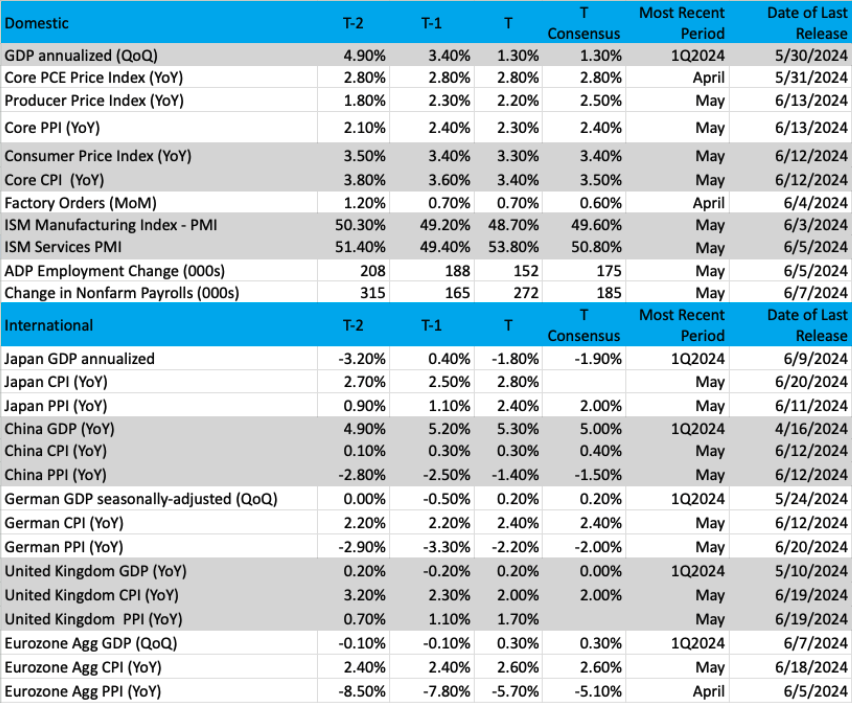

Key Global Economic Readings

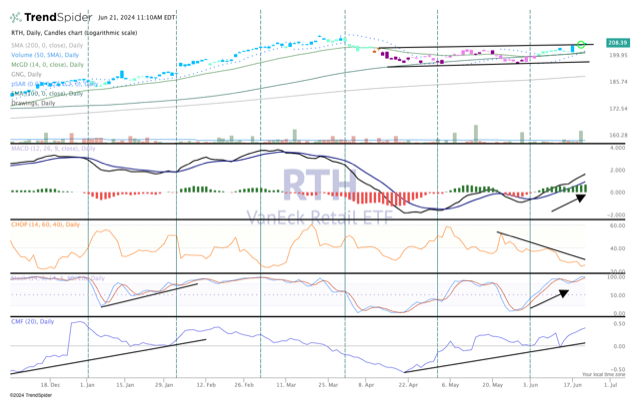

Chart of the Week: The VanEck Retail ETF (RTH)

As the consumer/spending are close to 70% of the economy, it stands to reason we have a close on retail companies/retail sales. On Tuesday, saw the release of May retail sales and they were rather disappointing even though there were some positives to be had for several of our holdings. The data seem to reflect the consumer is slowing down with their spending habits, perhaps the wish from the Fed of a slower economy to cut interest rates is starting to happen.

Some have written off the consumer, saying prices are too high and income too low. This happens frequently, but we have learned when you start doubting the consumer and spending habits it is often the wrong move. We watch the retail names closely, not just the big names like Costco, Walmart, Target and Home Depot. Collectively, the VanEck Retail ETF RTH really captures the entire retail complex, including Amazon as well (the biggest online retailer).

The chart is actually very strong here. The RTF shows a nice series of higher highs, higher lows and blue candles on the GoNoGo indicator (top pane). This tells us this ETF is in a strong bullish run. The RTH seems to be breaking out of the channel, which is also bullish (if confirmed next week). MACD (moving average convergence/divergence) is on a buy signal while the chop index is pointing down, which tells us a trend is now in place. We like the position on stochastics here, higher highs and higher lows (pane four) as this shows the RTH has momentum.

We hold some retail names in TheStreet Pro portfolio, like Costco and Amazon. There seems to be good upside to this ETF and perhaps a move to $220 is coming soon.

Other charts we shared with you this week were:

- Monday, June 17: S&P 500 – "The S&P 500 March Forward"

- Monday, June 17: SPDR Gold Trust – "Gold Is in a Consolidation Period"

- Tuesday, June 18: Qualcomm QCOM – "Qualcomm Continues Its Winning Ways"

- Thursday, June 20: Apple AAPL – "Apple’s Chart Is Simply Stunning"

The Coming Week

While the pace this week was slower than usual given the Juneteenth holiday, the combined impact of the retail sales, housing starts and industrial production reports led to only a modest downward revision to the Atlanta Fed’s GDPNow model. While down to 3.0% from 3.2% a week ago, the rolling forecast is still higher than the early June reading of 1.8%. If the Atlanta Fed factored S&P’s flash or final monthly PMI data into its rolling GDP forecast, odds are we wouldn’t have seen any modest revision this week.

Next week brings more housing data with the May new home sales report and the pending home sales report. We’ll also get the latest take on housing prices but comments this week from Lennar LEN and KB Home KBH tell us home builders are focusing on more affordable housing.

Because the market is still finely attuned to the potential for Fed rate cuts, next week’s May PCE price index is bound to be the economic data focal point next week. As expectations for the headline figure as well as the core one firm up ahead of next Friday’s print, we’ll share them with you. Alongside that data, we’ll also receive the May figures for personal income and spending. We should see real wage growth continue, a positive for overall spending, but digging into the May personal spending data will give us a clearer picture of where consumers have been spending quarter to date.

Here's a closer look at the economic data coming at us next week:

U.S.

Tuesday, June 25

- Chicago Fed National Activity Index – May (8:30 a.m. ET)

- FHFA Housing Price Index – April (9:00 a.m. ET

- S&P Case-Shiller Home Price Index – April (9:00 a.m. ET)

- Consumer Confidence – June (10:00 a.m. ET)

Wednesday, June 26

- MBA Mortgage Applications Index – Weekly (7:00 a.m. ET)

- New Home Sales – May (10:00 a.m. ET)

- EIA Crude Oil Inventories – Weekly (10:30 a.m. ET)

Thursday, June 27

- Jobless Claims – Weekly & Continuing (8:30 a.m. ET)

- Advance Retail & Wholesale Inventories – May (8:30 a.m. ET)

- Durable Orders – May (8:30 a.m. ET)

- GDP (Third Estimate (1Q 2024) - (8:30 a.m. ET)

- Pending Home Sales – May (10:00 a.m. ET)

Friday, June 28

- Personal Income & Spending, PCE Price Index – May (8:30 a.m. ET)

- The University of Michigan Consumer Sentiment Index (Final) - June (10:00 a.m. ET)

International

Thursday, June 27

- China: Industrial Profits – May

- Eurozone: Loans to Companies and Households – May

- Eurozone: Economic Sentiment, Consumer Confidence - June

While it’s true the sheer volume of earnings reports will slow to a mere trickle, because of our holdings in Bank of America BAC, Morgan Stanley MS, Nvidia NVDA, Apple AAPL, Qualcomm QCOM, Marvell MRVL, Universal Display OLED and PepsiCo PEP we will be parsing quarterly results and guidance from Jefferies JEF, Micron MU and General Mills GIS closely.

We’ll also be interested in comments from FedEx FDX and Nike NKE about what they see ahead for the global economy, consumer spending, the dollar, and China.

Here's a closer look at the earnings reports coming at us next week:

Tuesday, June 25

- Open: Jefferies

- Close: FedEx

Wednesday, June 26

- Open: General Mills

- Close: Micron

Thursday, June 27

- Open: Acuity Brands (AYI), McCormick & Co. MKC, Walgreens Boots Alliance WBA

- Close: Nike

Portfolio Investor Resource Guide

- Economic Data: "Here's a List of Links to the Key Economic Data We Closely Watch"

- Investing Terminology: "16 Key Terms Club Members Should Know"

- 10-Ks: "Want to Know About a Stock? Read the Company's Reports"

- 10-Qs: "Unlock the Numbers and Key Information Behind Your Stock With the 10-Q"

- Income Statement: "Our Cheat Sheet to Understanding This Financial Document"

- Balance sheet, Cash Flow Statements, and Dividends: "How to Know If a Company Is Off-Kilter? Read Its Balance Sheet"

- Valuation Metrics: "Everyone Wants a Value. Here's How Investors Can Find"

The Portfolio Ratings System

- Buy Now (BN): Stocks that look compelling to buy right now.

- Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

- Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

- Sell (S): Positions we intend to exit.