Weakening Economic Data Has Stoked Investor Fear: Here’s Our Plan

July jobs and Service PMI numbers could further amp-up rate-cut expectations. This is what we'll be watching.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

* Weaker-than-expected July Manufacturing PMI data re-ignited investor fears over the speed of the economy.

* If Friday’s July Employment Report adds to that growing concern, the next crucial data point will be Monday’s July Service PMI reports.

* Should those reports echo the July Manufacturing PMI slowdown, odds of a Fed rate cut in September will move even higher.

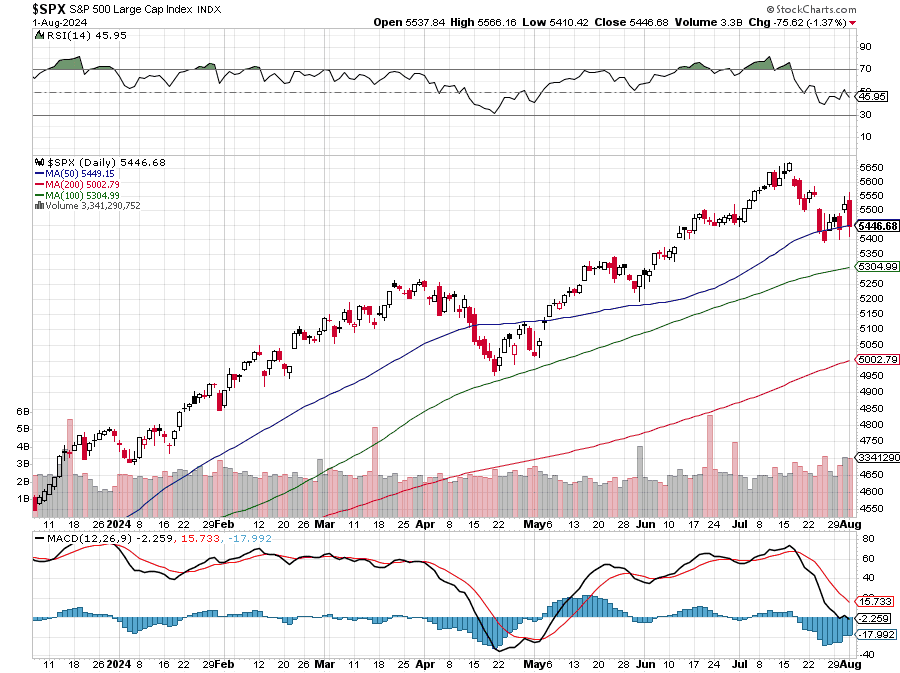

* Friday we will be watching the market’s technical support levels, and here’s where it could make sense for us to get off the sidelines.

Investor fear is once again running the market, which helps explain Thursday’s move in the market following the July Manufacturing PMI from ISM. The headline figure did miss expectations, as did new orders, but it was the plummet in ISM’s manufacturing employment to 43.4 from June’s 49.3 that raised eyebrows because it was the weakest figure since June 2020, back in the somewhat early days of the global pandemic. Also drawing attention was the uptick in the Prices sub-index to 52.9 from June’s 52.1.

Shoot first, ask questions later took over, but our job is to remain level-headed. So, while the manufacturing economy fell more than expected, indicating an accelerating slowdown in that part of the economy, we have to remember the Services sector has been carrying the overall economy. What was more concerning to us was the manufacturing contraction found in the final July PMI report from S&P Global.

We say that recognizing the two manufacturing PMI reports have painted a different picture of the manufacturing landscape in recent months. Similar to ISM’s findings, the July picture painted by those from S&P Global showed a reversal for the recent manufacturing recovery. Central to that reversal was the steepest decline in new order activity so far this year. Many respondents shared the view this decline was temporary and “linked to paused spending and investment ahead of the Presidential Election.”

While this could be true for mid-to-large capital spending items, S&P’s survey also showed “producers of consumer goods also reported a modest fall in demand.” We’ve recognized the consumer has been selective, but when the CEO of Hershey HSY comes out and says consumers are “pulling back on discretionary spending” it means either they are tightening their belts even more or pushing back on paying up after multiple rounds of price increases. Odds are it’s a combination of the two, and for that reason, we’ll continue to favor Costco COST over other consumer-facing companies. We will see how PepsiCo’s PEP efforts to reposition its products to more price-sensitive customers pays off, but if there are signs that it’s not or if consumer spending develops the way ISM’s July Manufacturing employment data did, it would be a reason to revisit owning PEP and potentially Mastercard MA in the portfolio.

That brings us back to the July Services PMI reports from ISM and S&P Global that will be published Monday morning. For June, ISM’s Service PMI showed that part of the economy contracting, and if next week’s report confirms that it will add to renewed concerns about the economy. Getting ready for that data means paying close attention to what is revealed in Friday’s July Employment Report, which the market expects to show more jobs being added compared to June. ADP’s July Employment Change Report disappointed, with 122,000 jobs added during the month compared to 155,000 in June and the market forecast for 150,000. A miss like that in the July Employment Report and sizable negative revisions for May and June will add to concerns about the speed of the economy and the consumer.

As we sift through these reports — so too is the Fed. Fed Chair Powell’s recent comments revealed the central bank is walking a line now between further progress on inflation and the economy, including the jobs market. During his prepared remarks this week, Powell said “If the labor market were to weaken unexpectedly or inflation were to fall more quickly than anticipated, we are prepared to respond.”

The potential for the Fed to wait too long to start cutting rates has been a growing concern, and if Friday’s jobs data and Monday’s July Service sector data confirm the economy has hit something larger than a speed bump, expectations for a September rate cut will move higher than they already are. As we said in recent weeks, bad economic news is back to being good news for rate cuts.

Despite the recent pain in the market, including the near 4% fall in the S&P 500 since its July 16 peak, that market barometer has continued to hug its 50-day moving average. If Friday’s jobs numbers and the fallout from earnings last night, including the disaster that was Intel INTC, push the S&P 500 past its 50-day moving average, the next level of support is ~2.6% lower at its 100-day moving average near 5305. While not yet oversold with its RSI level near 46 as of last night, the S&P 500 is far from oversold at current levels.

If we see the market become oversold in the next few days, that would be a potential signal for us to get off the sidelines with some of our holdings that have been hit the worst by investor fears.

Part of that will be seeing what today’s July Employment Report brings for not only job creation during the month but revisions for the last few as well.

More Pro Portfolio:

- We're Adding to Two of Our Tech Positions

- Monthly Roundup: Can the Market Meet the Challenge?

- What McD's $5 Meal, an L.A. Court Hack and Demand for Perfume Tell Us

At the time of publictaion, TheStreet Pro Portfolio was long COST and PEP.