As Campaign Season Heats Up, Thoughts on Corporate Tax Rumblings

There are many moving parts but higher tax rates in 2026 could trigger EPS re-thinking

You've reached your free article limit

You've read 0 of 1 free Pro articles.

As you have likely heard, the Democratic National Convention is being held this week, and on Thursday night Vice President Kamala Harris is expected to accept the party’s nomination. Leading up to that Harris is discussing her economic plans and related matters, she recently commented that if elected she would propose raising the corporate tax rate to 28% from 21%. The rate landed at 21% as part of the 2017 Trump tax cuts that reduced the rate from 35% and several of those provisions are set to expire at the end of 2025 barring any changes from Congress.

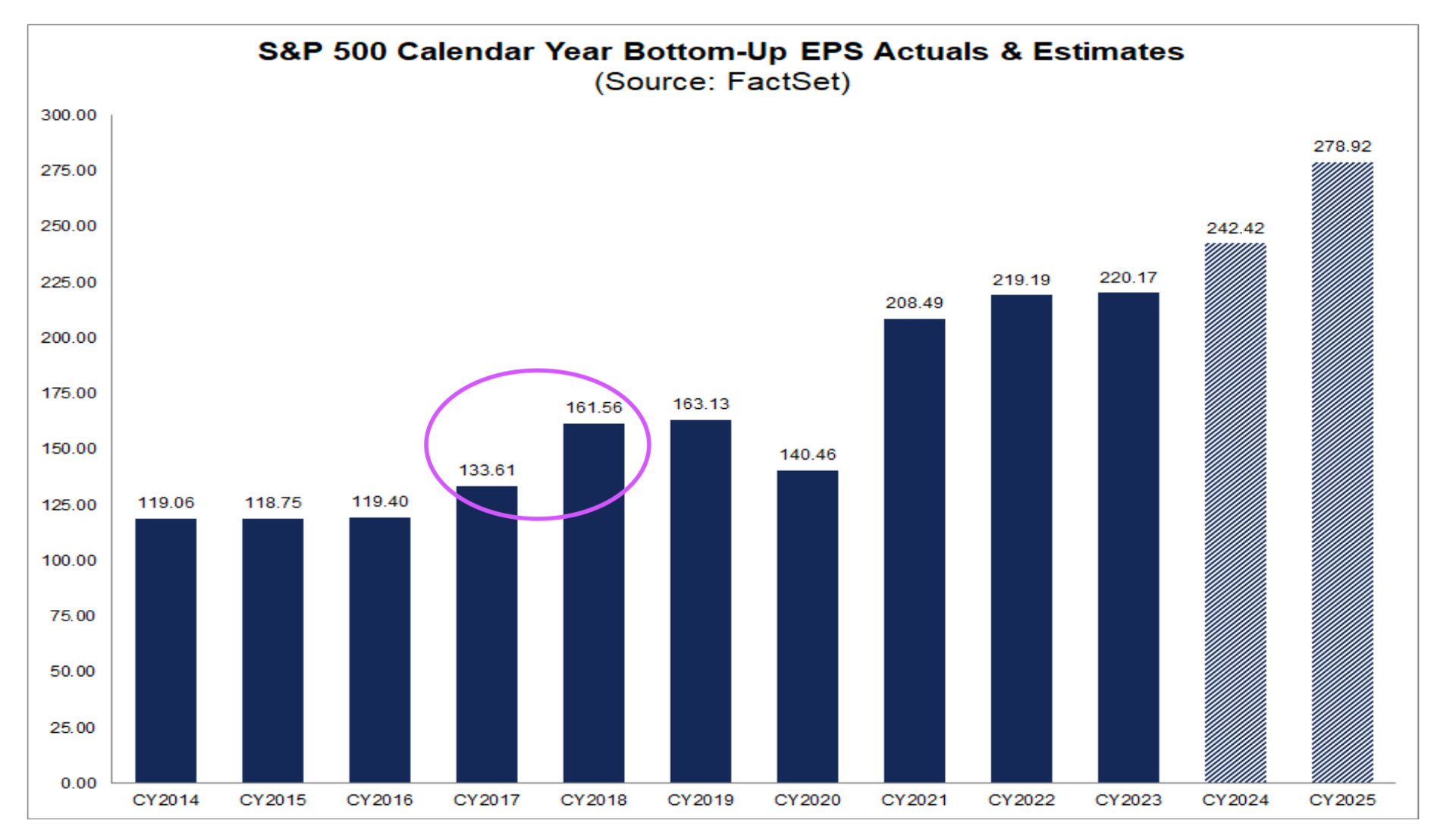

Depending on the presidential election and the landscape in Congress, it means in about a year we could be in for a different corporate tax rate, something that could have potential implications on corporate earnings in 2026 and beyond. When the Trump tax cuts went into effect in January 2018, as we can see it had a pronounced impact on 2018 EPS figures for the S&P 500. We also saw the market multiple for the S&P 500 expand considerably compared to pre-2018 levels.

Was all that 2018 EPS growth tied to the Trump tax cuts? With GDP for 2018 rising to 2.9% from 2.3% the year before, it’s likely a safe bet the answer is no, but there is little question the drop in the corporate tax helped grow EPS in 2028 compared to 2017.

Examining the consensus 2026 expectations across a swath of companies, we find that tax expense as a percentage of pre-tax income averages 23.8% and skews a bit lower for companies with greater international exposure. For 2027, the same findings were had.

While it may be a bit of way off, this suggests that higher tax rates will ding 2026 and most likely forward EPS expectations, resulting in what may appear to be slower growth rates. As of now, that hit doesn’t look to be tremendous and it doesn’t seem that a return to the pre-Trump tax cut level of 35% is in play.

To be fair, the majority of EPS expectations for 2026 and beyond are nowhere near fully baked and a lot can change subject to the outcome of the 2024 election cycle and the economy.

We’re not sharing this to alarm anyone. However, because we’re longer-term in our thinking and our position holding, we’ll continue to revisit this as new developments arise. The more near-term focus will be determining how realistic the expected 15% year-over-year 2025 EPS growth for the S&P 500 is.