Four Charts That Explain Why the Market Is Selling Off

Our call for a re-thinking of the Fed's rate-cut cadence is unfolding.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

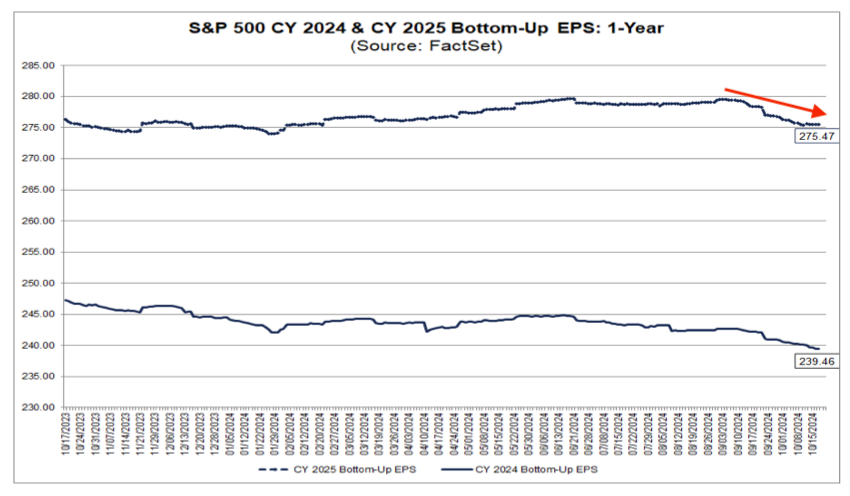

In Monday’s Daily Rundown video, we laid out our game plan for the week, discussing that 2024 EPS expectations were once again reset lower last week, continuing what we’ve seen over the past few months. We also said that the stronger-than-expected economy may mean those downward revisions were overdone, but that same strength in the economy may lead to a slower pace of Fed rate cuts.

While many are focused on how many rate cuts the Fed may deliver before year-end, a slightly longer view shows expectations for the Fed Funds rate to hit 350-375 basis points with the Fed’s June 2025 meeting. The Fed Funds rate currently sits between 475-500 basis points.

Based on comments from Fed officials and the move higher in the 10-year Treasury yield, it would seem our view that rate-cut expectations need to be revised to a somewhat slower pace based on data from the last several weeks is starting to take hold with more on Wall Street.

Weighing the probabilities and anticipating this likelihood, we’ve boosted our cash levels and recently added a small position in the ProShares Short S&P500 ETF SH. Our plan remains to let stock prices come to us, bringing with them opportunities to pick up stocks of well-positioned companies poised to generate outsized EPS at better risk-to-reward levels.

Now let’s dig deeper into what’s backing these thoughts of ours and share a few charts as well.

U.S. Economy: Good for Earnings, Not for Rate-Cut Cadence

Coming into this week, consensus second-half 2024 EPS growth expectations for the S&P 500 were revised to just 5.3% compared to the first half of 2024. Back in July, that expectation was above 11%, but the U.S. economy is also on far stronger footing than was thought at that time.

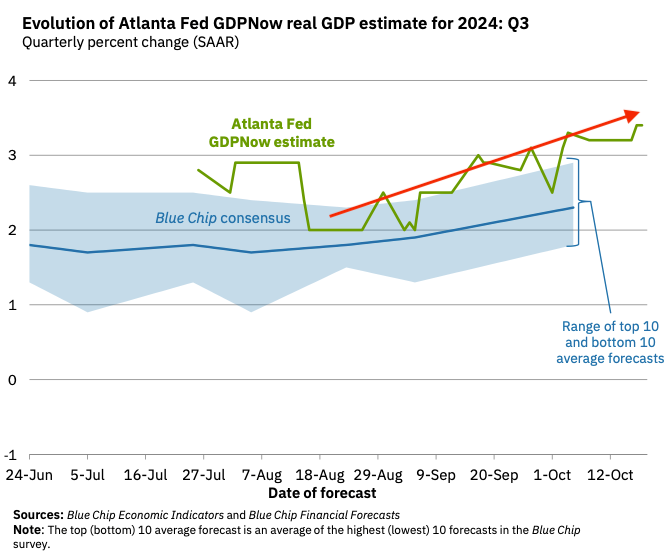

With only a few September data points remaining, the Atlanta Fed’s rolling GDPNow model pegs Q3 2024 at 3.4% compared to 2.0% in mid-August. That suggests those downward EPS expectation revisions for H2 2024 may have been a tad excessive for some parts of the economy.

While potentially good for the current earnings season, a stronger economy is leading traders to pare back bets on aggressive easing by the Federal Reserve. More cautious comments from Fed officials over the pace of future rate decreases are also influencing this latest rate-cut cadence re-think. That includes Minneapolis Federal Reserve President Neel Kashkari hinting Monday the central bank may take a more modest approach from here.

We have just a few more Fed speakers between Tuesday and Wednesday, but the latest edition of the Fed’s Beige Book out Wednesday afternoon, and Thursday morning’s Flash October PMI data from S&P Global (SPGI) will bring the next snapshot of the economy. Should they show more evidence of a strengthening economy, the more likely we’ll see the 10-year Treasury yield tick higher, rate-cut expectations slow, and a valuation-stretched stock market sag.

Should that come to pass, we’ll aim to cherry-pick opportunities for the portfolio in existing positions and from the Bullpen.