August PPI Ups Probability of Fed Rate Cut Disappointment

Plus, a potential government shutdown and S&P 500 EPS growth prospects are on our radar.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

*The Fed is still likely to deliver a 25 basis point rate cut next week

*The August CPI report and Thursday's August PPI data add to our thinking that the Fed will see far fewer rate cuts this year than the market expects

*The risk of a partial government shutdown in October is on our radar

*Some are starting to join us in thinking S&P 500 EPS growth expectations for 2025 may be a bit lofty

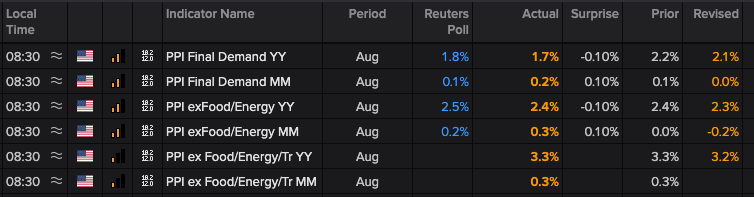

Round two for this week’s August inflation data, better known as the Producer Price Index (PPI), is out. And, much like Wednesday's August Consumer Price Index (CPI), it was a mixed bag.

While the core PPI came in at +2.4% on a year-over-year basis, below the market forecast of +2.5%, it was up from the revised July figure of +2.3%. Matching what we saw on Wednesday with the latest core CPI figures, the core PPI rose 0.3% in August, warmer than the market forecast and a jump from the revised figure of 0.0% in July.

The combination shouldn’t derail the Fed from kicking off a rate-cutting cycle, but it does reaffirm our thinking that a 25 basis point (BPS) cut will be delivered next week. It also backs our thinking that the Fed will signal more modest rate cut expectations for 2024 and 2025 in its updated set of economic projections compared to market expectations.

We’ve been sharing that view and the data leading up to next week’s Fed policy meeting points to an increasing probability for that outcome. We’re not alone in that thinking. Before the August PPI report, Sergio Ermotti, group CEO of UBS Group AG, shared that he thinks “the market seems to be a little bit too ahead of the curve in expecting the Fed to go so aggressively.”

That’s why, when we look at the Fed’s update projections, we’ll be looking at what the near-term rate cut expectations are as well as the cumulative ones for 2025.

Given the findings of these two August inflation reports, we will revisit the CME FedWatch Tool later on Thursday or Friday to see if market rate cut expectations have softened in response. If that’s not what we see, it will be a signal to us that the risk of disappointment remains and that we should proceed carefully in the coming days.

That path to that event also contains more management presentations, and we will continue to mine them for data points and signals for the Portfolio. That’s the very near term, but some things are bubbling on the horizon for the later near term and later this year that we are watching as well.

An October Government Shutdown?

As this week’s 2024 presidential debate fades, it appears that we may be facing another partial government shutdown on October 1, 2024. On Wednesday, House Speaker Mike Johnson canceled a planned vote on a stopgap funding bill that could keep the government open for the next six months after more than a dozen Republicans walked back their support for it.

What could make this round of debt-ceiling negotiations even more challenging is the presidential election and calls by some to include the SAVE Act, which would require people to show proof of citizenship to register as a voter. Congressional Democrats have vowed to vote against any spending plan paired with the SAVE Act.

While the likely outcome will be some deal to keep the federal government open, we wouldn’t be surprised if it turns out to be another nail-biter and something that helps September live up to its market reputation. As things develop or don’t, we’ll continue to share our updated thinking and position things accordingly.

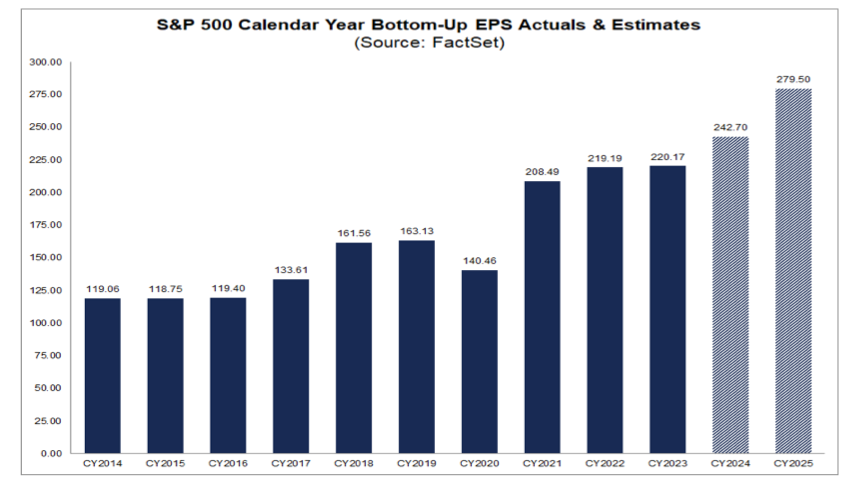

2025 S&P 500 EPS Growth Questions Are Beginning

Coming off Nvidia’s NVDA bullish comments at the Goldman Sachs Communacopia conference on Wednesday, folks may be paying a bit more attention to similar presentations on Thursday and as we close out the week.

They’ll be looking for insights for the soon-to-be-over September quarter and sharpening expectations for the December one. But some are already starting to take a hard look at 2025, including expected S&P 500 EPS.

We’ve shared our view about how aggressive the market consensus of roughly 15% EPS growth for next year is for that market barometer. Roth MKM is joining us in that thinking, sharing that history shows analysts’ 12-month earnings forecasts tend to be about 30% too high at cycle peaks.

As we think about it, if the Fed needs to deliver more than 200 BPS in rate cuts over the next nine months, it’s another reason to question such a degree of expected EPS growth re-acceleration.

More Pro Portfolio

- Buying More Stock of This Semi-Cap Equipment Position

- Weekly Roundup: Is the Market Setting Up for an April Repeat?

- The AI Conundrum, Cyber Threats, and Our Digital World: More News on Our Strategies

At the time of publication, TheStreet Pro Portfolio was long NVDA.