Apple and Universal Display Earnings: Here's What to Watch and Our Game Plan

While we like the longer-term opportunities, expectations continue to run high suggesting near-term caution.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

* Apple and Universal Display will report after today’s market close, here’s what we’re watching and our game plan.

* Findings from Canalys and IDC support a good quarter at Apple, while comments from Qualcomm and Qorvo do the same for the current quarter.

* Universal should benefit from the smartphone rebound, but we’re interested in other markets as well.

We have earnings after today’s market close from Apple AAPL and Universal Display OLED. As we get ready for those results, let’s review some recent quarterly results and other data for the smartphone market that suggest favorable June-quarter results from both companies.

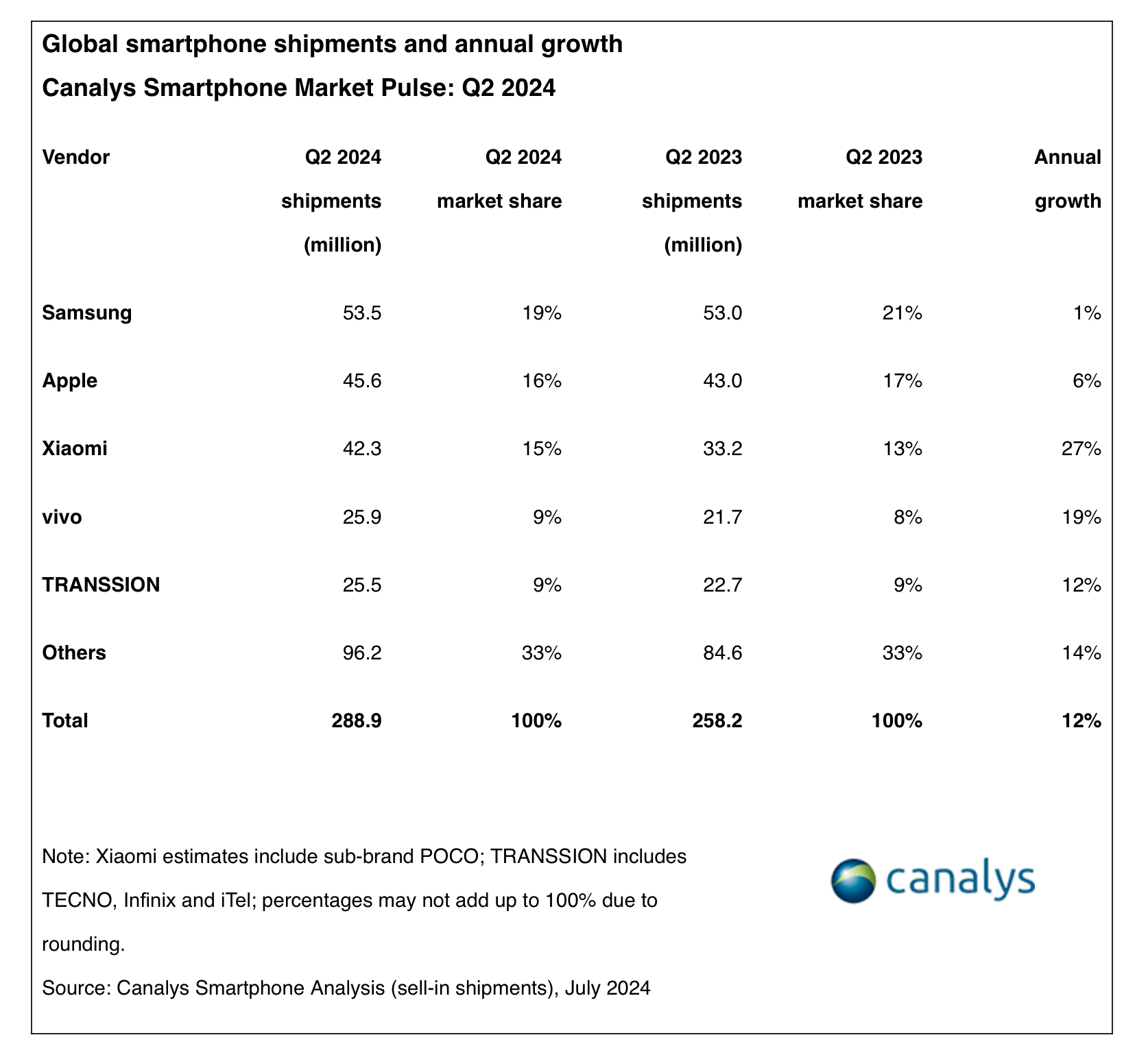

Setting the stage for these two reports from Apple and Universal Display, research firm Canalys shared its view that smartphone industry shipments rose 12% year over year to 288.9 million units in the second quarter. That figure supports what we learned from Qualcomm QCOM about its June-quarter results and bodes very well for what Universal Display is likely to report after tonight’s close. Universal will also benefit from the ramp of Apple’s newer iPad models that include light-emitting diode displays.

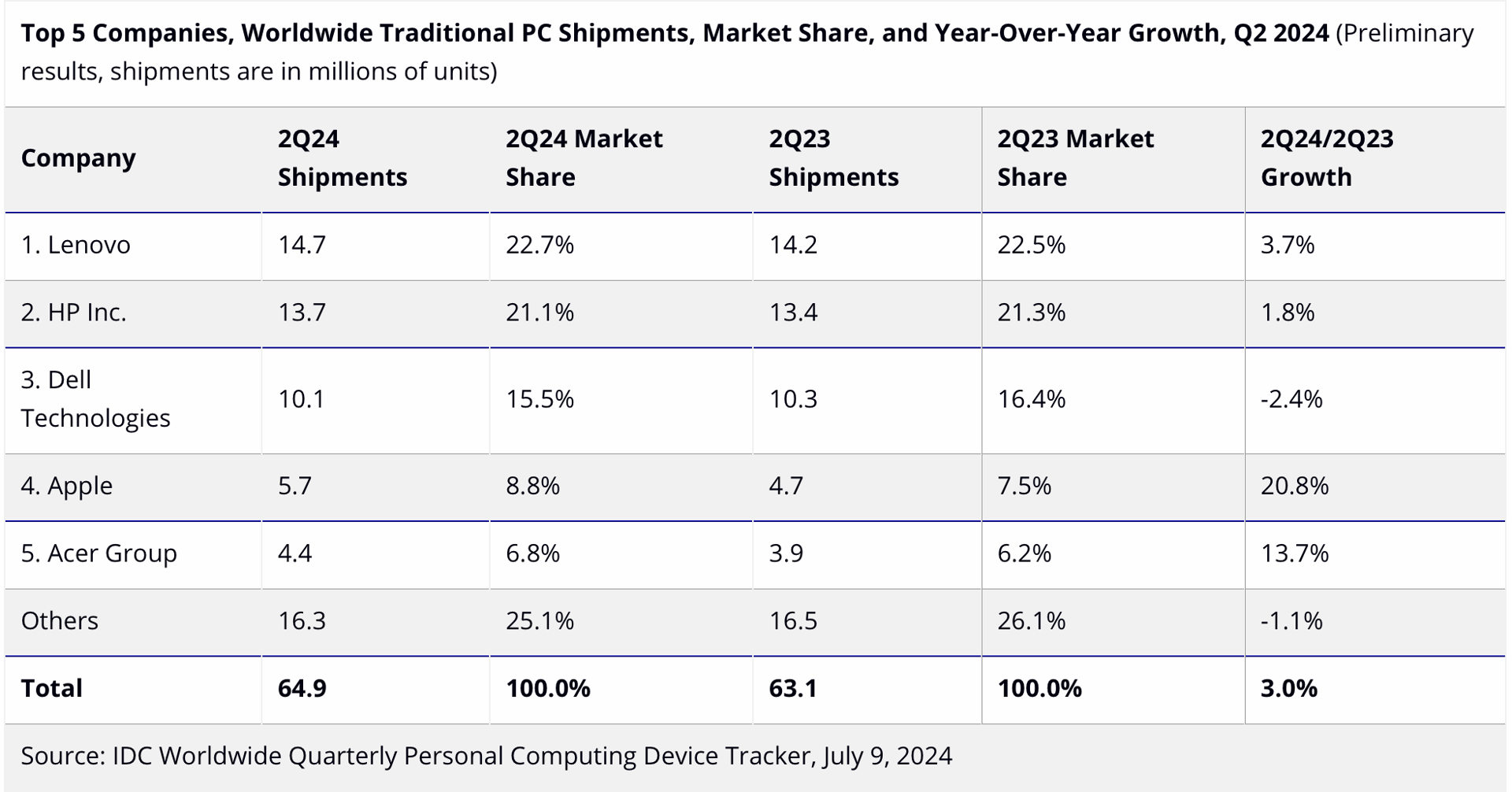

Canalys’s findings also put Apple’s shipments for the quarter at 45.6 million units, up 6% year over year, a positive for what the company is going to say about its iPhone business tonight. Another research firm, IDC, shared Apple’s PC sales rose just over 20% compared to year-ago levels in the June 2024 quarter.

As Apple’s install base continues to grow, we should see continued lift in its higher-margin Services business, which accounted for 26% of March quarter revenue. That easily made it Apple’s second-largest segment behind the iPhone’s 51%.

Looking toward Apple’s guidance, the market consensus pegs September-quarter EPS at $1.56 on revenue of $93.4 billion, compared to expected EPS of $1.35 on revenue of $84.5 billion for the June quarter. Most will be listening for the seasonal ramp in iPhone shipments as well as the expected launch of Apple’s new iPhone models. The focus of those questions will be how early in September they will launch. The reason is that the earlier in September they launch, the more of an impact those new models may carry in the current quarter. Still, the bulk of the impact will be had in the December quarter.

Earlier today, we discussed Qualcomm’s QCOM June quarter results and its comment that referenced Apple increasing its orders for the current quarter. Qorvo QRVO also said its net inventory rose as it prepares for the seasonal ramp at its largest customer, which is Apple. Both comments point to improving volumes for Universal Display in H2 2024. Apple’s Mac business should continue to benefit as the PC market rebound continues and as it brings Apple Intelligence to its newer line of Apple Silicon Macs, helping to foster the upgrade cycle.

Speaking of AI and upgrade cycles, RF chip company Skyworks SWKS had an interesting take on those relating to the smartphone market: “We expect new AI features will only be available on the latest next-generation smartphones, potentially fueling a multiyear upgrade cycle… Most significantly, we believe the rollout of compelling AI applications will drive a smartphone replacement cycle, one that is currently the longest in history, standing at over 4 years.”

That comment reinforces the view that in H2 2024, we are just beginning the first inning of AI smartphones. As the number of AI-enabled apps and use cases grow, the upgrade cycle is likely to accelerate like it has in the past when new features and technologies were included in new smartphone models.

It’s that upgrade cycle that keeps us bullish on AAPL and QCOM shares. We do expect Apple management to be questioned over the timing for Apple Intelligence to be released across its next OS platforms.

That upgrade cycle is also positive for our shares of Universal Display but there are other drivers as well for the adoption of organic light-emitting diode displays in other applications (PCs, tablets, automotive) that have larger surface areas. As that mix of end markets skews more toward larger format display sizes, we should see revenue at Universal accelerate. On the company’s earnings call tonight, we expect positive comments about the smartphone market, but it will be these other applications that we’ll want to hear much more about.

More Pro Portfolio:

- We're Adding to Two of Our Tech Positions

- Monthly Roundup: Can the Market Meet the Challenge?

- What McD's $5 Meal, an L.A. Court Hack and Demand for Perfume Tell Us

Game Plan

From a technical perspective, both stocks have support at their respective 50-day moving averages, but given what we’ve been seeing of late, we would suggest members stay on the sidelines into these two earnings reports.

Coming into this earnings season, we commented that company earnings reports would need to be picture-perfect because market expectations and the S&P 500’s valuation were high. While the pre-earnings commentary is favorable, the slightest wrinkle in either of their earnings reports could lead the shares to those 50-day moving averages or below them. If we see that, the smart move may be to let the post-earnings impact wash over AAPL and OLED shares and make our next move from there.

At the time of publication, TheStreet Pro Portfolio was long AAPL, OLED and QCOM.