A Sound Fundamental Outlook Means We're Sticking With This Name

A gap in the chart could bring a compelling risk-to-reward entry point.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

* Shares of United Rentals moved past our $625 panic point, triggering a thorough review.

* Multiple stimulus programs are expected to see infrastructure outlays peak in 2028.

* We’ve seen URI pull back multiple times despite the improving fundamental picture.

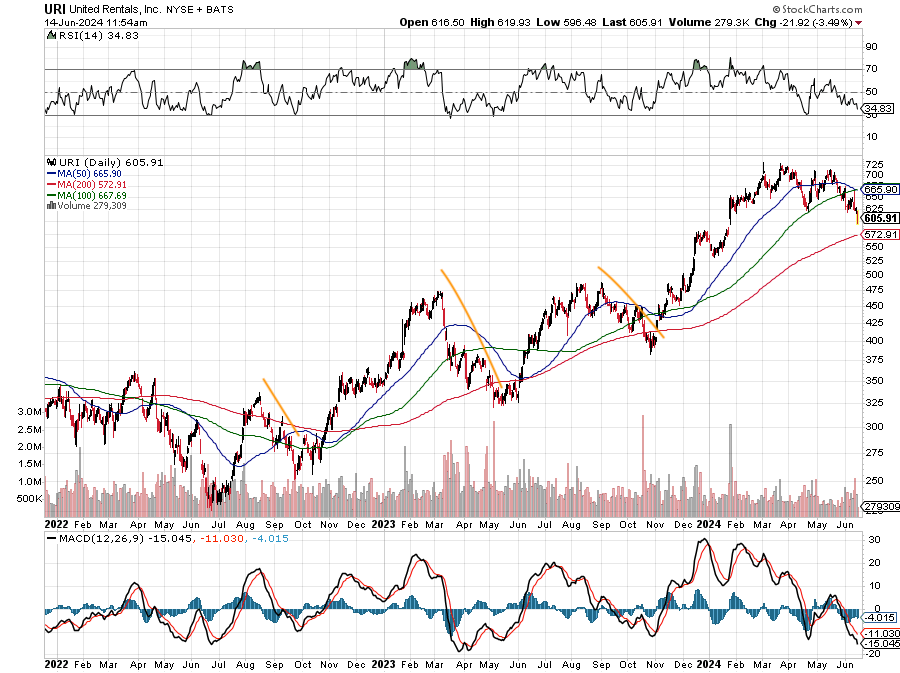

* There is a gap in URI's chart that could be filled, offering a compelling risk-to-reward opportunity.

Shares of United Rentals (URI) are moving lower, passing through our $625 panic point, leading us to take a hard look at the name. There are times when weakening fundamentals start to rear their head, requiring a re-think of things. That is what our panic points are designed for, and the process could sometimes trigger a change in our opinion. However, that is not the case for United Rentals.

Here’s why:

Despite the retreat in URI shares, the fundamental picture for non-residential construction remains vibrant, backed primarily by infrastructure spending. Previously, we’ve discussed the multi-layered benefit of the Biden Infrastructure, Inflation Reduction Act, and the CHIPS Act, and those tailwinds remain. The Dodge Momentum Index, a monthly measure of the initial report for nonresidential building projects in planning, which leads construction spending by 12 to 18 months, remains elevated and supports a positive outlook for construction activity. That fundamental outlook keeps us bullish on URI as well as Vulcan Materials VMC.

Since we started the portfolio’s position in URI back in mid-2022, there have been a few times in which we’ve seen larger drops in the shares, much like we’re seeing now. We can see those in the chart below, but the larger moves in the stock have been higher as non-residential infrastructure spending has steadily grown.

That prospect isn’t expected to change anytime soon.

A new quarterly construction report from Wells Fargo Bank found that infrastructure and mega project spending, mostly the result of recent federal legislation, will be a key driver of equipment demand. The most noteworthy spending will come from the $1 trillion infrastructure legislation passed in 2021, which will provide a springboard for activity with the bulk of the spending to occur during the next four years. That report finds we will not see a peak in infrastructure outlays until 2028 given the combined impacts of the Biden Infrastructure Law, the Inflation Reduction Act, and the CHIPS Act. In terms of the CHIPS Act, projects must start before December 2026 to qualify for funding, which supports that 2028 peak.

We also think the eventual loosening of monetary policy will be a positive for construction projects as well as the housing market. Better borrowing costs and lower project hurdle rates are likely to spur additional activity.

Getting back to the URI chart, we see a gap, which helps explain some of the recent share pressure. However, not all gaps get filled, but should we see the shares move closer to that level, it would be a favorable level for us to pick up some additional URI. A successful test of the 200-day moving average near $573 would be another reason.

JPMorgan recently initiated coverage of United Rentals with an "Overweight" rating and a $780 price target. Its thesis, paraphrased here, is going to sound familiar to you: The equipment rental industry is expected to be a key beneficiary of multi-year non-residential and infrastructure projects in the US with United Rentals' scale driving above industry-average growth and returns. This suggests that because of the fundamental picture, there is a high probability that JPMorgan and others with similar targets and ratings will come out in support of the shares given the pullback.

Putting all the above together means we are not going to exit the portfolio’s position in URI. Instead, we will look to opportunistically pick up more shares should reach they levels discussed above. Having scrutinized the situation, we will also drop our URI panic point to $550, which is modestly above the January low point in the shares.

More Pro Portfolio:

- We Are Calling Up a New Portfolio Position From the Bullpen

- Weekly Roundup: 5 Stocks Power the Portfolio

- Signals From Our Investing Notebook

At the time of publication, TheStreet Pro Portoflio was long URI and VMC.