Why I’m Eyeing Prices, Biotech and AI in Q3

As the second quarter skims some froth off the technology trade, let’s see why these three areas are key to watch in Q3.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Some of the froth came off parts of the technology sector last week as the Nasdaq gave up 4.6%. The biggest weekly decline for the index since April 2025. We will come to the end of the second quarter on Tuesday. In today’s column, I will highlight three things I will be monitoring closely in the coming quarter.

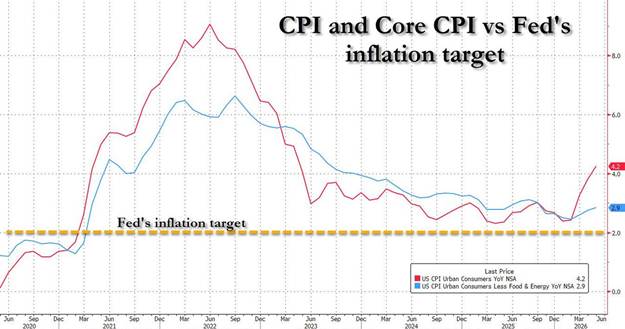

No. 1: Will Inflation Ebb?

The conflict in Iran and the effective closure of the Strait of Hormuz for over three months triggered a huge surge of price inflation for many energy and commodity products including crude oil, LNG, helium, and many components of fertilizer. This helped push May’s consumer price index reading up 4.2% over the prior 12 months. May’s producer price index print was even higher and at levels not seen since late 2022.

Since a memorandum of understanding has been agreed to with Iran, oil prices have fallen substantially. Gasoline is back under four bucks a gallon. Not surprisingly, both consumer sentiment readings and the approval rating for the U.S. president have ticked up on that news. Given the upcoming mid-terms, the administration should have an incentive to ensure this trend continues.

Of course, reopening this global choke point will do little to help with the surge in prices for DRAM and NAND memory as that is being driven by hyperscaler demand. I doubt it will allow any reductions to the Fed Funds rate in 2026, although hopefully if inflation ebbs it will take any prospects for a rate hike off the table as well. I will be watching events on this front closely in the coming quarter. The hope is things will continue to calm down in the Middle East and by the end of summer, the markets will start to price in a rate reduction in the first quarter of 2027.

No. 2: Biotech M&A Volume

Biotech has been a nice surprise in 2026 after being a laggard in the market for many years. The State Street SPDR S&P Biotech ETF (XBI) is up over 27% year-to-date. This rally has coincided unsurprisingly with a notable tick up in M&A volume this year. Last week, Apogee Therapeutics, Inc. (APGE) was taken out with a solid buyout premium by AbbVie (ABBV) in a near $11 billion purchase. Whether deal volume continues to be elevated in the coming quarter will largely determine if biotech continues to outperform in Q3.

No. 3: AI Narrative Takes Some Dents

The suppliers of the picks and shovels to the AI revolution like Nvidia (NVDA) and Intel (INTC) continue to print profits. The rest of the AI ecosystem has started to struggle. Hyperscalers have been very weak recently as capital budgets continue to surge, partly due to higher component costs. The stock of Microsoft (MSFT) is off better than 20% year-to-date and the shares of Meta Platforms (META) are not too far behind. The trading price of Oracle (ORCL) has been more than cut in half from its highs late last summer after it signed a five-year $300 billion deal with OpenAI to build and supply compute power. Notably, late last week, chatter spread that OpenAI would likely have to move its initial public offering to 2027. Will more chinks dent the AI narrative in the coming quarter? If so, how big of an impact will this have on the overall market and economy? This is one of several items I will be monitoring closely in the quarter ahead.

At the time of publication, Guilfoyle was long ABBV, XBI.