Why I’m Bracing for the Market to Cool by Fall

Nasdaq, the S&P and even the Russell are all up; but here’s why I think they’ll come back down to earth.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The artificial intelligence narrative that has powered the bull market rally in equities since late 2022 continued to take on some water last week. Bloomberg reported that Meta Platforms (META) is building a cloud business for its excess artificial intelligence compute capacity after Mark Zuckerberg stated AI agent development is not proceeding at the pace expected. Meta joins Space Exploration Technologies Corp. (SPCX) with this approach. SpaceX has already rented out the entire capacity of massive Colossus 1 data center complex and recently signed a deal to rent out some capacity from Colossus 2.

While the news moved the shares of Meta Platforms higher, it cast a significant cloud over much of the rest of the AI ecosystem. The semiconductor heavy Kospi sold off, Philadelphia Semiconductor Index (SOX) dropped 5.4% on Thursday, and neocloud providers Nebius Group N.V. (NBIS) and CoreWeave, Inc. (CRWV) also took significant hits to close out the holiday shortened trading week.

My regular readers know I believe we are in a similar bubble to the back half of the Internet Boom. The only question is whether it 1998 or 1999 right now. The overall market is certainly trading at 1999 like valuations viewed by myriad valuation metrics like the Shiller P/E, or price-to-earnings, ratio.

The potential pricking of the AI bubble is hardly the only major negative around the markets or the economy right now. Consumers not in the top of the K-shaped economy are struggling. We saw another sign of this late last week when June jobs report came in far lower than expected and previous month’s numbers were revised down. The unemployment rate did tick down 0.1% to 4.2%, but only because the labor participation declined further to an abysmal 61.5%. For comparison’s sake, it was roughly 600 basis points higher in 1999. The personal savings rate for May was a tepid 3.0%, despite higher tax returns this year and corporate year-end bonuses. Prior to the pandemic, the personal savings rate was around 7.5%.

The spring home selling season was largely a bust. Home sellers outnumber home buyers by the highest percentage since Redfin began tracking this metric in 2013. For one of the rare times in U.S. history, the median price of a new home is now lower than the median price of an existing home on the market. Single-family home inventory levels have hit a decade high and condo inventories are at 12-year highs.

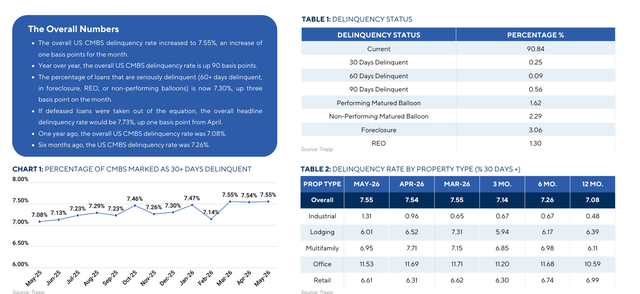

Things are no better with commercial real estate, which has some $5.1 trillion of debt outstanding. Most of which will have to be refinanced at significantly higher interest rates in coming years. There will be a significant debt maturity wall in the coming quarters as well. After being below 2% prior to the Fed starting to lift interest rates in March 2022, the delinquency rate for commercial mortgage-backed securities, or CMBS, has moved over 7%. The CMBS delinquency rate against office buildings is higher than the peak of the Great Financial Crisis. Multi-family is also notably deteriorating due to myriad factors. These two sectors account for roughly 70% of CRE debt outstanding.

Finally, we have the nearly $2 trillion private credit or shadow banking space. Fitch Ratings had the private credit fund default rate at a record 6% in April and May of this year. And remember these assets don’t trade on the public market and have their valuations determined by fund managers. The second quarter saw quarterly redemption requests severely gated for the second straight quarter at private credit funds run by the likes CliffWater, Apollo Global Management (APO) and Blue Owl Capital Inc. (OWL).

The private credit sector is substantially exposed to the mid-tier software sector and recently has expanded its footprint into the buy now, pay later space. What possibly could go wrong?

My portfolio remains very conservatively positioned as trading begins in the third quarter. The Nasdaq was up 20% in Q2 and the S&P 500 experienced a 14% rally. The Russell 2000 was up just over 21% in the first half of this year. I will not be surprised, however, if equities give back a decent chunk of those gains by the time we reach the end of summer. My portfolio is allocated accordingly.

At the time of publication, Jensen had no position in any security mentioned.