Where's the Market Headed Next? Let's Weigh the Evidence

We looked closely at the major indexes and key market data. Here's what we found.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The major equity indexes closed mixed Tuesday with mostly negative market internals as NYSE volumes dropped and Nasdaq volumes rose from the prior session. The only technical event of note was one index closing back below its near-term downtrend line and reverting back on a bearish trend.

The trends, as a whole, remain a mix of bullish and bearish projections. Cumulative market breadth weakened with two of the three of the exchanges in negative trends as well.

The data still find the McClellan 1-day OB/OS Oscillators neutral. However, most of the investor sentiment data (contrarian indicators) are flashing red lights due to the excessive amount of bullish investor expectations. Also, the forward valuation of the S&P continues to stay well above ballpark fair value.

Index Trends Stay Mixed as Breadth Deteriorates

On the charts, the S&P 500 (see above), Nasdaq Composite and Nasdaq 100 closed higher Tuesday as the rest posted losses.

Market internals were mostly negative with negative breadth and negative up/down volume on the NYSE.

The only technical event of note was the Dow Jones Transports closing back below its near-term downtrend line and now bearish (see below) as are the MidCap 400 and Russell 2000. The rest are in near-term uptrends.

Yet we do not like the underlying structure as the cumulative advance/decline lines for the All Exchange and Nasdaq remain bearish with the Nasdaq’s A/D making another lower low. Only the NYSE’s breath is positive. The market’s foundation continued to erode.

No new stochastic signals of import were generated.

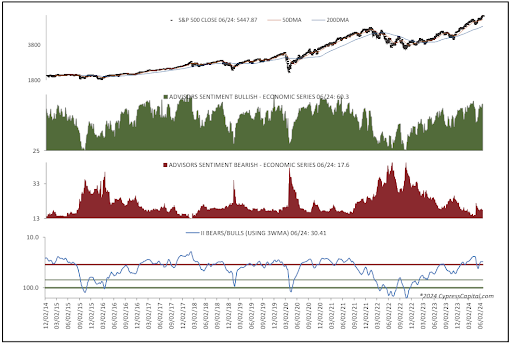

Sentiment Data Still Cautionary

The data remain mixed.

The 1-Day McClellan Overbought/Oversold Oscillators are still neutral (All Exchange: -27.38 NYSE: -19.38 Nasdaq: -31.69).

The percentage of S&P 500 issues trading above their 50-day moving average (contrarian indicator) dropped to 49% from 57%, staying neutral.

Of note, the detrended Rydex Ratio (contrarian indicator) remains bearish at 1.18.

Thus, two of the three sentiment indicators are still cautionary with this week’s AAII Bear/Bull Ratio (contrarian indicator) a neutral 0.69, but the Investors Intelligence Bear/Bull Ratio (contrary indicator) (see below) stayed bearish at 17.6/60.3 as bulls well outweigh bears.

The Open Insider Buy/Sell Ratio remains neutral but dropped to 31.5 as insiders did some selling.

Leveraged ETF sentiment is 5.9, remaining neutral.

Valuation Remains Extended

The 12-month consensus earnings estimate for the S&P 500 from Bloomberg rose slightly to $253.51 per share. Yet its forward P/E multiple of 21.6x remains well above the “rule of 20” ballpark fair value at 15.8x. It remains an important concern for us as an almost 600-basis point premium remains significant.

The S&P's earnings yield is 4.64%.

The 10-Year Treasury yield slipped to 4.24%. Support is 4.18% and resistance is at 4.35%. Its near-term trend is bearish.

The U.S. dollar, via the UUP ETF, closed higher at $29.03. Its trend remains bullish. Support is $28.89 and $29.23 is resistance.

Bottom Line

The weight of the evidence suggests we remain cautious in our near-term view.

Sell signals on individual names should be honored while buying should be extremely selective.