We're Turning a Corner on the Correction

The equity index charts are showing improvements -- with one catch.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

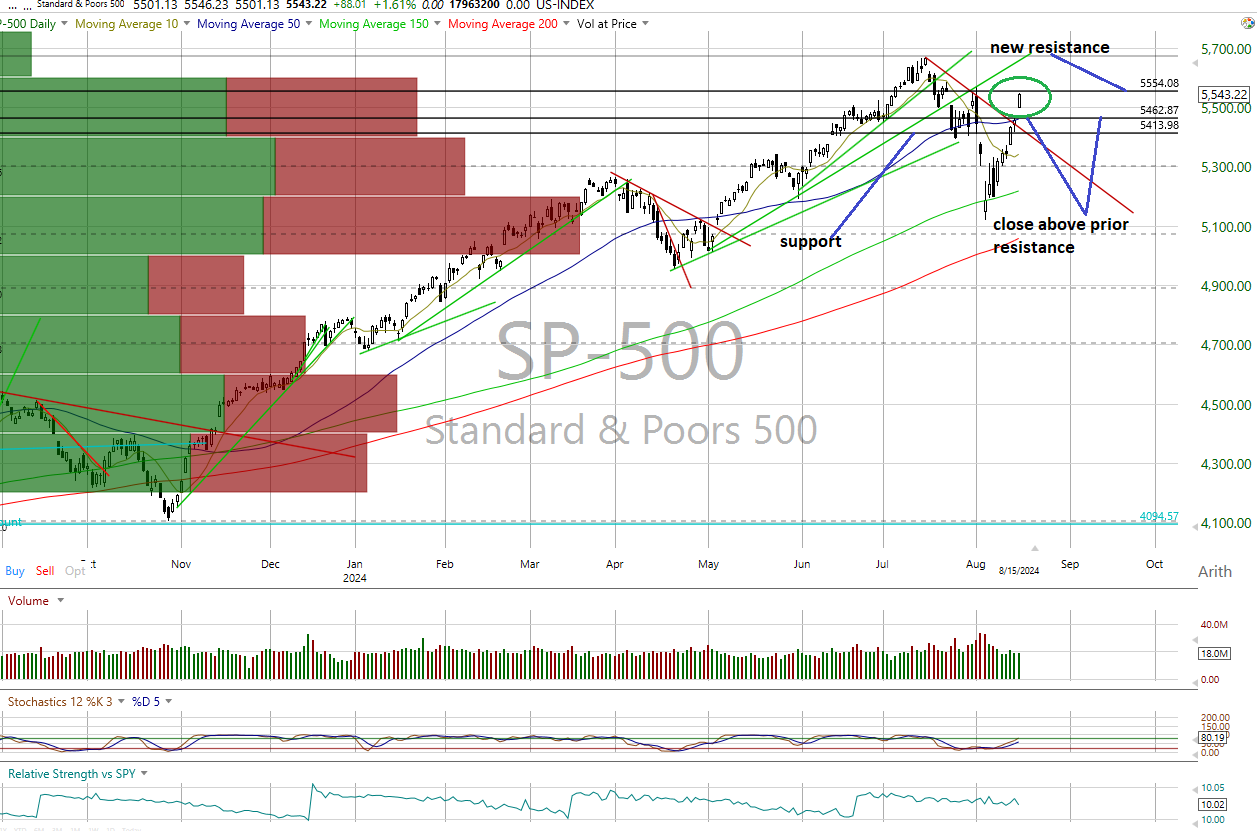

All the major equity indexes closed higher Thursday with positive New York Stock Exchange and Nasdaq internals, as trading volumes rose on both from the prior session. All closed near their session highs. And, guess, what? We now see several positive technical events appearing on the charts.

The Charts

We're seeing positive internals on heavier trading volumes, as equity indexes closed above their near-term resistance levels. The one exception was the mid-cap stocks.

The Nasdaq Composite Index and the Dow Jones Transports closed above their downtrend lines and are now neutral vs. their prior bearish trends.

Finally, the Russell 2000 saw enough gains to turn its trend to bullish from neutral, being the only index in that condition.

The Dow Jones industrial average is still in a downtrend, but the rest are now neutral, a notable improvement from a week ago.

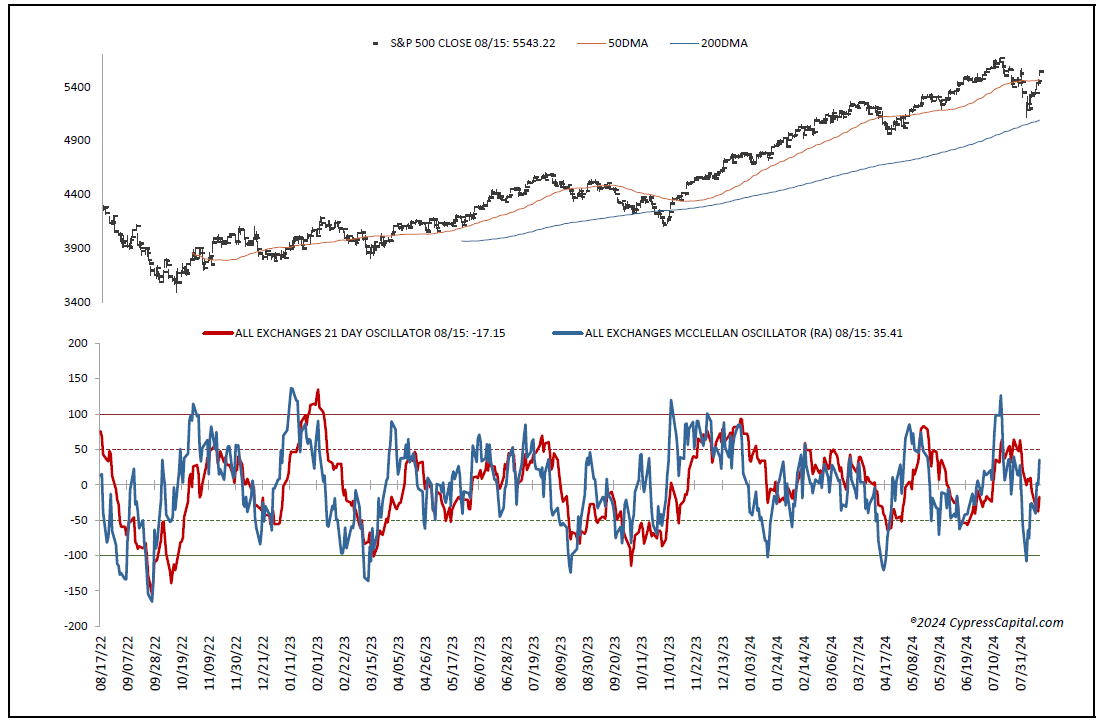

Cumulative market breadth remains bullish on the All Exchange, NYSE and Nasdaq while no stochastic signals of note.

The Technicals

Cumulative market breadth remains bullish, while the data is almost entirely neutral. This all suggests the recent market correction may have seen its lows. But we still have a jaundiced eye regarding the forward valuation for the S&P 500 vs. ballpark fair value. The 12-month consensus earnings estimate for the S&P from Bloomberg rose slightly to $250.52, leaving its forward price-to-earnings of 22.1 still well above the “rule of 20” ballpark fair value at 16.1; we believe this premium remains significant. Its earnings yield declined to 4.52%. This tempers our outlook a bit, and means we'll continue to honor sell signals on individual names when said signals appear.

The one-day McClellan overbought/oversold oscillators appear neutral, with only the NYSE mildly overbought (All Exchange: 35.41; NYSE: 53.16; Nasdaq: 24.17).

The percentage of S&P issues trading above their 50-day moving averages, a contrarian indicator, rose to 66% and is neutral. The detrended Rydex Ratio, also a contrarian indicator, rose to 0.83 and remains neutral, as well.

This week’s American Association of Individual Investors Bear/Bull Ratio, another contrarian indicator, rose to 0.83 and is also neutral.

But the Investors Intelligence Bear/Bull Ratio -- contrary indicator -- stayed bearish at 26.15%, with investment advisor bulls continuing to outweigh bears by a wide margin. We still believe the “wall of worry" needs to see some further strengthening.

The Open Insider Buy/Sell Ratio dipped to a neutral 42.0%.

Treasury and the Buck

The 10-year Treasury yield rose to 3.93%. Support is 3.79% and resistance at 3.97%. Its near-term trend is bearish.

The U.S. Dollar, via the U.S. Dollar Index Bullish Fund UUP, closed higher at $28.55. Its trend is bearish with support at $28.30 and resistance at $28.60.

The Bottom Line

In conclusion, the improvements in the chart trends and cumulative breadth combined with mostly neutral data suggest we may have seen the bulk of the correction already. But valuation is still a concern.