Warren Buffett Seems to Understand That TINA Has Taken on New Meaning

In theory, TINA should have died with the monetary policy that created it. But she lives on in a new way.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The acronym TINA (there is no alternative) was born in the near zero-interest rate era and referred to the justification of keeping money in stocks even if the fundamental backdrop and prospective risk suggested it was aggressive to do so. In short, for almost two decades, TINA encouraged overzealous risk-taking because risk-off assets weren’t producing yield, and it worked tremendously for investors. This was by design; keeping interest rates low is a method of monetary policy intended to push dollars into riskier assets that promote economic growth, such as stocks. It was a winning strategy by central bankers.

In theory, TINA should have died with the monetary policy that created it, but she has lived on. When inflation struck, causing the Federal Reserve to flip from a low-interest rate regime to a high-interest rate regime, Treasuries paying 4% to almost 6% on various parts of the curve should have been enough to attract money away from stocks and into the safety of U.S. government bonds. That isn’t what happened.

Instead, market participants have become increasingly drunk on risk and alpha. I’m sure they ask themselves, “Who wants a comfortable 5% when stocks are churning out 20% years like clockwork?” Who could blame them? Anybody practicing risk management and diversification has been punished harshly, while aggressive portfolio allocations have worked like a charm. Is this the new norm, or is it a temporary anomaly that will eventually wreak havoc on our retirement plans? I hope I am wrong, but I believe the latter is probable.

A New TINA?

TINA may mean something far different in 2025 than in the past; at some point sooner than most believe, there might not be an alternative to Treasuries (not stocks). Stock market investors have been emboldened to take outsized risks despite relatively attractive Treasury yields because the strategy has paid off without real conviction tests.

Should volatility increase and persist, investors will indeed look for safer assets. With FDIC insurance covering $100,000 and SIPC insurance limited to $500,000, the best risk/reward play for larger players could eventually be boring U.S. bonds. At a current rate of +4% on the 10-year note, investors get paid to wait with a very high probability of return of capital if held to expiration. This isn’t as sexy as a tech stock or a triple-leveraged ETF, but investors should always be mindful of the risk taken to achieve reward. The risk of being long and wrong in the stock market is much greater than the prospects of further long-term gains. Warren Buffett seems to agree; the Oracle of Omaha is actively raising cash by selling risk assets.

Trump Trade Mostly Priced In?

Unlike the first Trump reign, which surprised markets from the get-go, this time around, the “Trump trade” has been playing out for weeks. The Trump victory wasn’t a surprising outlier event, and the world is bracing for tariffs. Thus, we may have seen the Trump policies largely priced in before the election and the remainder occurring in the days after.

The markets appeared to change their tone in late September and early October. Grains started selling off, interest rates rose sharply, bitcoin moved higher, the U.S. dollar roared higher and U.S. stocks defied gravity. These were telltale signs that the market was voting with their dollars. However, we must wonder if the Trump trade is nearly exhausted even before the president enters the White House. We might be setting up for a massive buy-the-rumor-sell-the-fact scenario. We believe market participants should look for potential reversals in the stock rally, the Treasury selloff and the grain selloff in the coming months.

Treasury Selling Overdone?

Regarding Treasuries specifically, expectations for inflation created by the Trump tariffs have been aggressively priced. Eight years into the Trump era (this is not a political statement or endorsement; I just don’t know what else to call it), we should be more aware of the art of the deal. He makes stunning policy comments to start the negotiations, but the final figure is generally less of a shock. Thus, the 60% Chinese tariffs he discussed on the campaign trail will probably be far lower once the rubber hits the road. Further, during the last Trump administration, interest rates probably would have ended the presidency near the same place it started if it hadn't been for the pandemic. We recognize that the Federal Reserve was actively buying its own Treasury securities to stabilize prices. Still, we aren’t sure that is enough reason to shrug off the market selling Treasuries to prepare for expectations of inflation and higher growth under the new administration in such a manner that puts the yield over a full percent higher than the last Trump presidency.

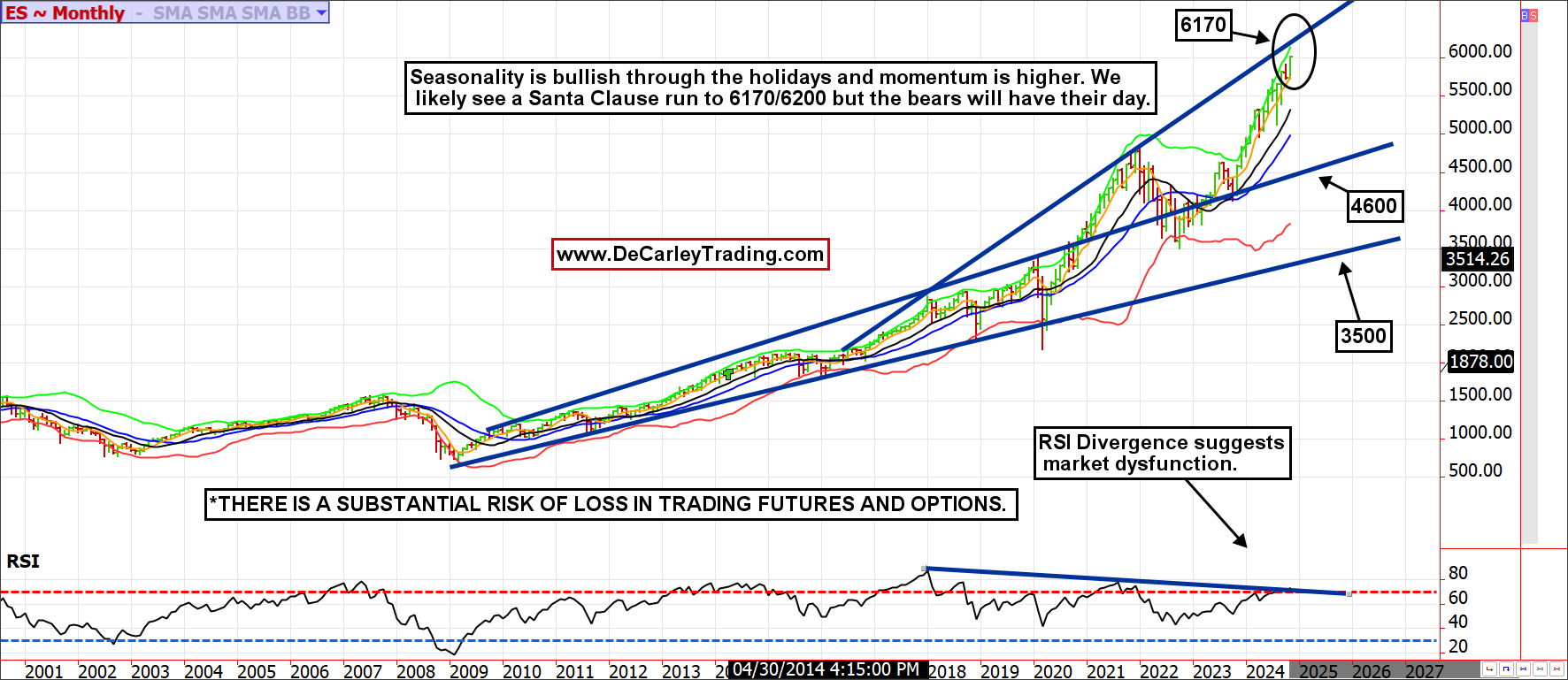

Santa Clause Could Exaggerate Rally

In equities, deregulation and animal spirits are compelling. Still, equity market valuations are near dot-com bubble heights, with most gains driven by loose monetary and fiscal policy as opposed to organic innovation and economic growth. What if the new administration just inherited a stock market dumpster fire? We need to look no further than Super Micro Computer SMCI, one of the largest customers of the biggest company in the world NVDA, looking like it could be the next Enron.

Nothing reveals the magnitude of our current financial situation more than a monthly chart of the S&P 500.

Before the financial crisis and the advent of the so-called Fed put, the stock market maintained a positive trajectory overall, but the slope was relatively unimpressive. Post-financial crisis: corrections were quicker and shallower. Finally, after the massive inflationary policy intended to fight the pandemic, we’ve seen elevated volatility, mostly skewed to the upside.

In the short run, prosperity can be manufactured, but we have yet to find out if it can be sustainable in the long run. China and Japan are two recent examples of how using monetary and fiscal policy without productivity as a long-term solution to generate to outsized growth can fail.

History Might Not Repeat, But It Rhymes

It took Japan decades of negative interest rates to allow its primary stock index to return to its 1990 elated high; this milestone was reached in 2024, almost 35 years later. The Chinese story is still being told, but the CCP has done everything possible to keep growth rates up; they have even gone so far as to build fake cities. However, despite the wildly aggressive stimulus unleashed on markets a few months ago, the country has stopped growing. Notwithstanding unprecedented efforts to keep the escapade going, the Shanghai index peaked near 5550 in 2007 at the height of the pre-financial crisis and hasn’t returned since.

I’m an optimist but I’m also a realist; we might not be immune to the same fate these two countries have experienced in the aftermath of risk asset bliss. Protect yourself.

At the time of publication, Garner had no positions in any securities mentioned.