Wall Street Gets Two Breaks in One Night

Let's check Tesla's earnings, the overnight bid for U.S. Treasury debt securities, small caps and Palantir.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Equity markets appear to have caught a break overnight.

On Wednesday, pressure on U.S. Treasury debt securities from the belly of the yield curve out to the long end, finally amounted to a decent sell-off across U.S. stock markets. The S&P 500 gave up 0.92% for the session, posting a third consecutive red candle and a fourth red candle in five days. This, however, was the first of those red candles of any real significance.

The more visible damage was done to the Nasdaq Composite. That index surrendered 1.6% for the regular session on Wednesday, ending a five-day winning streak. In fact, the daily performance for the Nasdaq Composite amounted to its worst day since taking a 2.55% beating on Sept. 6, which provided the recent low for this index headed into the recent rally.

Nine of the 11 S&P sector exchange-traded funds closed out that regular session with a loss. The worst of the selling for the day on Wednesday was saved for the Discretionary XLY and Tech XLK sectors that were down 1.57% and 1.43% respectively. The Discretionaries were led lower by hotels, restaurants and autos, while tech was led lower by the semiconductors. Yes, rising yields pressured these sectors, but the selling was accelerated by news that British chip designer Arm Holdings ARM was canceling a license deal that had allowed Qualcomm QCOM to make use of its intellectual property. ARM gave up 6.7%, while QCOM gave up 3.8% on Wednesday.

Hey, Sarge... didn't you mention a break?

Tesla and Treasury

... There are actually two positive breaks impacting overnight markets. Forget that Boeing BA employees don't seem to understand how much trouble their employer is in. The focus, at least from a Nasdaq perspective, is on Tesla TSLA. Elon Musk's company, which is both a tech company and a consumer discretionary company, posted a quarterly beat on earnings coupled with a revenue miss. The real news was in the gross and operating margins, which were at their best level since the fourth quarter of 2022, and the first quarter of 2023 respectively. In addition, the automotive ex-credits gross margin printed at 17.1%, well above expectations for something more like 15%. Musk also said during the call that its "lower-cost vehicles "with the advent of autonomy" should be available at some point during the first half of 2025 and produce 20% to 30% vehicle sales growth.

On top of that, U.S. Treasury debt securities have found a bid overnight. On Wednesday, the yield for the U.S. Ten Year Note went out at 4.24% (up 3 basis points) after peaking above 4.25%. Very early Thursday morning, U.S. ten-year paper is paying just about 4.2%, as the 4.25% level may have triggered some demand. The U.S. Two Year Note went out on Wednesday paying 4.07%. I see the Two Year paying less than 4.06% this morning.

Do these rising rates, moving in single basis point increments, really have an impact on the everyday economy? You bet they do. On Wednesday morning, the Mortgage Bankers Association reported a 6.7% drop in mortgage applications for the week ending Oct. 18 from the week earlier. This was the fourth consecutive weekly decrease for applications and came on the heels of last week's 17% drop.

Additionally, the National Association of Realtors reported September existing home sales of 3.84 million, at a seasonally adjusted annual rate, well below projections for 3.89 million and down from August's revised 3.88 million. Just an FYI, 3.84 million makes September of 2024 the weakest month for existing home sales in the U.S. in 14 years. That's right, 2010. What good times those were. By the way, existing home sales are on track to match 2023's full-year total. Should this slowdown continue and 2024 fall short of 2023 in total, that will make this year the weakest for existing home sales since 1995. How about that?

Charting a Small-Cap Move

While the Nasdaq Composite, even in weakness, continued to send mixed messages as far as trading volume is concerned, losers did beat winners by almost 3 to 1 at the NYSE, with advancing volume taking a 31.3% share of the composite NYSE-listed action. On top of that, aggregate NYSE-listed trading volume increased 5.7% on a day over day basis. That was with the S&P 500 shedding 0.92%, the Dow Industrials giving back 0.96% and the Dow Transports surrendering an even 1%. Something to chew on.

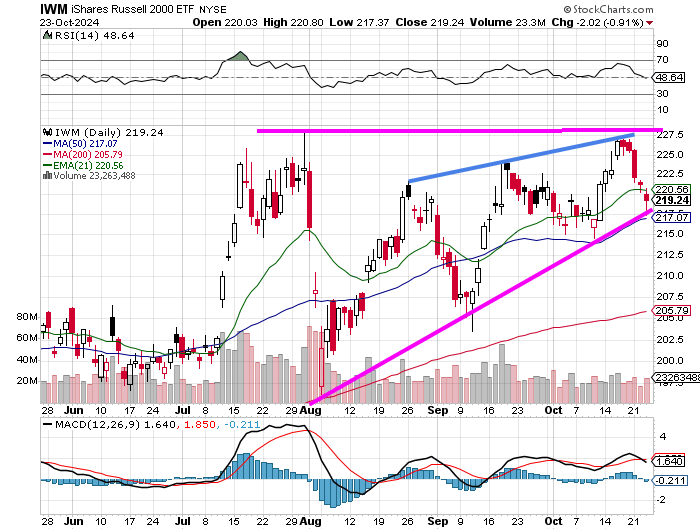

At least small caps stopped underperforming. The Russell 2000 "only" gave up another 0.79% on Wednesday, which put the iShares Russell 2000 ETF IWM on the brink of testing its 50-day simple moving average.

Readers will see two possible set-ups for the IWM ETF. In pink I have outlined an ascending triangle, which is bullish.

If I start the drawing in August, (adding the blue line) instead of July, then we are talking about a rising wedge, which is a pattern of bearish reversal. On Wednesday, the 50-day line proved to be support, keeping the dream alive. It's what happens when that line is next tested that will likely prove which of these patterns we look back on as being correct, completely forgetting that there was ever a fork in the road.

Beige Just About Describes It ...

On Wednesday afternoon, the New York Fed released the Fed's Beige Book, which is released in between Federal Open Market Committee meetings and compiles anecdotal economic information from across the Fed's 12 regional districts. Beige is a plain and rather boring color, as are most of these comments...

"On balance, economic activity was little changed in nearly all Districts since early September, though two Districts reported modest growth."

"Employment increased slightly during this reporting period, with more than half of the Districts reporting slight or modest growth and the remaining Districts reporting little or no change."

"Inflation continued to moderate with selling prices reportedly increasing at a slight or modest pace in most Districts. Still, the prices of some food products, such as eggs and dairy, were reported to have increased more sharply. Home prices edged up in many Districts, while rents were reported to be steady or down slightly."

I will attest that egg prices are still out of control. I do eat a whole lot of eggs. Readers will recall that I have stated that I believe consumer-level inflation had bottomed in September, so while I do see the somewhat tame comment on inflation as positive, I also expected it. It's going forward that I expect inflation to gradually accelerate. Of course, if the Fed holds its horses a little and does not force short-term rates lower while still inappropriate, thus compounding their September error, perhaps the long end of the curve could stop behaving as if inflation were headed to the moon. The debt-load I cannot help you with. Both sides of the aisle are more fiscally reckless and irresponsible than would be wise.

Palantir Partnership

On Wednesday afternoon, all-time Sarge fave Palantir Technologies PLTR and L3Harris Technologies LHX announced a strategic partnership to propel and accelerate L3 Harris' digital transformation. L3Harris' sensors and software systems will integrate Palantir's AIP (Artificial Intelligence Platform) to enable increased levels of capability that will include working on the U.S. Army's TITAN project. The two companies are already working together on integrating Palantir's platform into the L3Harris WESCAM system that provides for increased target detection and delineation.

Readers will note that PLTR has attempted to break out of the Pitchfork model I showed you three weeks ago and appears to possibly be consolidating at this lofty level. While my target price remains $48, I would welcome such a development as that would bring the pivot up from where I currently have it, which is $40 to the recent highs at a rough $44.40. That is where PLTR hit resistance on back-to-back days. Moving the pivot almost $4.50 higher would allow me to move my target about a dollar higher, so it's a positive.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 243K, Last 241K.

08:30 - Continuing Claims (Weekly): Last 1.867M.

10:00 - New Home Sales (Sep): Expecting 713K, Last 716K SAAR.

10:30 - Natural Gas Inventories (Weekly): Last +76B cf.

11:00 - Kansas City Fed Manufacturing Index (Oct): Expecting -16, Last -18.

The Fed (All Times Eastern)

09:45 - Speaker: Cleveland Fed Pres. Beth Hammack.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: HOG (.81), HAS (1.31), HON (2.50), NOC (6.05), R (3.42), TXT (1.51), UNP (2.78), UPS (1.63), VLO (.98)

After the Close: COF (3.76), LHX (3.27), WDC (1.71)

At the time of publication, Guilfoyle was long NOC, PLTR equity.