Wall St. Takes Hit on Iran Fire, SpaceX Takes Off, Middle-Class ‘Struggle’

Iran ceasefire looks near collapse; SpaceX valuation at $1.75 trillion; Beige Book sees some in middle-income bracket ‘struggling more.’

You've reached your free article limit

You've read 0 of 1 free Pro articles.

U.S. financial markets took something of a beating on Wednesday. Crude oil prices moved higher throughout the session as did yields on Treasury debt securities. This pushed equity prices lower. The rather fragile ceasefire between the U.S. and Iran appeared to be on the verge of collapse on Wednesday. Iranian forces launched a large ballistic missile and attack drone assault on both Kuwait and Bahrain targeting U.S. military bases as well as civilian areas.

The Kuwaiti government said that the nation had dealt with 13 incoming ballistic missiles and 17 one-way attack drones on Wednesday and that both civilian infrastructure and diplomatic missions had been damaged. At least one individual, believed to be an Indian national, had been killed while several dozen individuals had been wounded.

The attacks were supposedly in response to the U.S. Navy having disabled an empty Iranian tanker that attempted to breach the blockade of Iranian ports and load oil at Kharg Island. Several civilian maritime vessels in the Persian Gulf were also attacked by Iranian drones and defended by the U.S. Navy. CENTCOM considers the truce to still be in effect and continues to behave in the defensive.

Investor Shift

Optimism clearly took a hit on Wednesday. Investors had hoped recently that every day would be the day that Iran agreed to a deal that would end the war for at least two months. Instead, Iran and its proxies continue to take on a far more belligerent stance. Pres. Trump was asked on Wednesday if he thought that the U.S. naval blockade of the Strait of Hormuz could still be in place on Labor Day. The president responded that he thought this to be “unlikely” but that he could not rule it out. That was not what investors, traders and keyword-reading algorithms wanted to hear.

Economic Uncertainty

A number of economic data-points hit the tape on Wednesday. The ADP Employment Report for May showed 122,000 private sector jobs created during the month with job growth across companies of all sizes. Consensus had been for 118,000 jobs, so this was seen as positive for the economy.

The ISM Services PMI for May, like the ISM Manufacturing PMI, also showed expanded activity during the month with a sharp acceleration in new orders, but an accelerated contraction in service sector employment. In addition, the Federal Reserve published its latest edition of the Beige Book on Wednesday afternoon. In the publication, it is clear that several regional Fed districts “specified in it that members of the economy that are in the middle-income bracket are struggling more.”

Marketplace

On Wednesday, the S&P 500 gave up 0.74%, ending a nine-day, record-setting winning streak. The Nasdaq Composite surrendered 0.89%, putting an end to the very same streak of green-candle days. Small caps were hit harder as the Russell 2000 lost 1.31% as were the KBW Banks (-1.44%) The Philadelphia Semiconductors, however, swam upstream (+1.39%) supported by strength in SanDisk (SNDK), Intel (INTC), and Advanced Micro Devices (AMD). Some of these names are not faring so well overnight.

Five of the 11 S&P sector SPDR ETFs closed out the regular session on Wednesday in the green, obviously led by energy (XLE). Communication services (XLC) and the financials (XLF) led the losers. In a negative turn for the markets and perhaps the economy, defensive sectors in general, outperformed cyclicals.

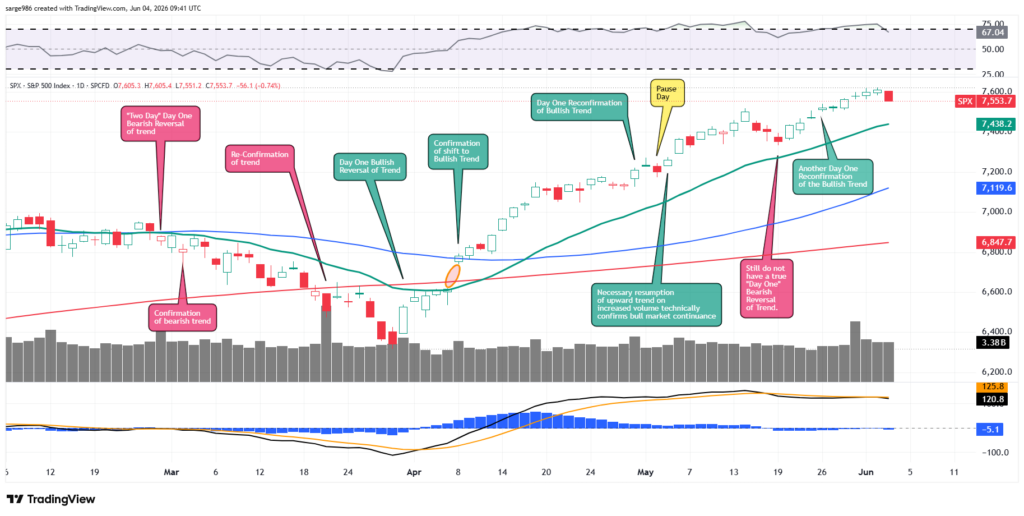

Breadth was nasty. Losers beat winners by a three-to-one margin at the NYSE and by a rough five to two at the Nasdaq. Advancing volume took a 38.7% share of composite Nasdaq-listed activity and a rather weak 22% share of composite NYSE-listed trade. The only saving grace here might be that aggregate trade contracted on a day over day basis as it has all week. This prevents Wednesday from presenting, technically, as a “Day One” bearish reversal of trend. Activity across Nasdaq-listings was down 4.2%, activity across NYSE-listings was down 2.6% and activity across the membership of the S&P 500 was lower as well.

We Have Liftoff?

SpaceX announced on Wednesday that it plans to sell 555,555,555 shares to the public at $135 per share. This will raise about $75 billion and value the company at a rough $1.75 trillion. SpaceX has about 12.9 billion Class A and Class B shares outstanding. CEO Elon Musk owns about 12% of the Class A shares and about 94% of the class B shares. The Class B’s have 10 votes per share, making them far more valuable from a “control the firm” viewpoint.

A valuation like this, should it come to pass, would value SpaceX at around 70-times projected 2026 sales and at about 265-times 2025 earnings before interest, taxes, depreciation, and amortization. Remember, SpaceX, as a company, is not yet profitable. The Starlink broadband business is a high-margin segment, but the AI business is losing money as are most AI-focused businesses due to aggressive capital spending. We have talked about this in recent days. Will highly valued IPO stocks like SpaceX, Anthropic and OpenAI draw investment capital away from the rest of our marketplace. I don’t see how they won’t.

No ‘Day One’

No, we do not yet have a technical “Day One” reversal due to the lack of trading volume. That said, for the S&P 500, Relative Strength dropped below the 70-level on Wednesday as the daily moving average convergence divergence took on a more bearish posture. Quite honestly, it would not take much to turn what we see right now into a head-and-shoulders pattern of bearish reversal. In fact, with equity index futures trading lower on Thursday morning, I’d say we’re at least halfway there.

Economics

(All Times Eastern)

08:30 – Initial Jobless Claims (Weekly): Expecting 211K, Last 215K.

08:30 – Continuing Claims (Weekly): Last 1.1786M.

08:30 – Non-Farm Productivity (Q1-rev): Flashed 0.8% q/q.

08:30 – Unit Labor Costs (Q1-rev): Flashed 2.3% q/q.

10:30 – Natural Gas Inventories (Weekly): Last +92B cf.

The Fed

(All Times Eastern)

1:10 p.m. – Speaker: San Francisco Fed Pres. Mary Daly.

Today’s Earnings Highlights (Consensus EPS Expectations)

After the Close: DOCU (.99), LULU (1.69), PL (-.04), ZUMZ (-.81)

At the time of publication, Guilfoyle was long PL, SNDK, AMD equity.