The Rally Rocks On, Boeing Dives on the Chart & Whopped by Wells Fargo

Let's check the markets, whether a half percentage point cut is a dream, and the charts of Boeing and Wells Fargo.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

How interesting .... The rally in equities kicked off on Wednesday about an hour into the regular trading session and still has not let up. Nvidia NVDA CEO Jensen Huang spoke on Wednesday about the coming shipment of his new Blackwell high-end AI chips this year and plans to scale them out and the market took off. That was after some negativity on Wednesday morning when the August consumer price index print hit the tape a little bit on the warm side, at least at the core on a month-over-month basis.

On Thursday morning, the European Central Bank cut its deposit rate by a quarter point to 3.5%. That at first put some pop in the U.S. Dollar Index, but that did not last. The ECB also increased its expectations for inflation to accelerate again in late 2024, but then resume its weakness in 2025. The ECB also clipped gross domestic product expectations for this year, next year and 2026 as well.

The main focus for U.S. markets early on, though, was the August producer price index. Producer prices for August printed at little on the warm side month over month, at both the headline and the core. But producer prices printed below expectations at both the headline and the core on a year-over-year basis. The results were more or less in line with those expectations when factoring in revisions made to the July data. This not only relaxed traders concerned about the size of the rate cut that the Fed might kick off its change in trajectory for policy next Wednesday, but actually emboldened some traders.

During regular trading hours on Thursday, futures markets trading in Chicago moved the probability for a half-percentage point rate cut on Wednesday from 15% to 19%. Overnight, however, that likelihood jumped all the way to 41%, largely due to articles published at both the Financial Times and Wall Street Journal that made the idea of such a cut to lead off a new cycle of looser monetary policy much more realistic. Needless to say, gold futures are trading at their highs for the week (as well as all-time), as the U.S. Dollar Index retests the 101 level from above. Treasury yields have moved lower overnight as well.

Thursday on the Market

On Thursday, the S&P 500 and Nasdaq Composite, up 0.75% and even 1% respectively, both posted their fourth-consecutive "up" day or green daily candlestick for the week.

With overnight equity index futures pointed in an upward direction, both U.S. major equity indexes will complete the sweep for the week on Friday. Smaller caps participated this time, as the Russell 2000 tacked on 1.22% and the S&P Midcap 400 gained 0.79%. Interestingly, I thought, as the Thursday rally was broad, the Philadelphia Semiconductor Index was down 0.24% on Thursday, led lower by Texas Instruments TXN and GlobalFoundries GFS, but the Dow Jones US Semiconductor Index was up 1.08% led by Broadcom AVGO and Nvidia. Again, I quote Grant Williams... "Things that make you go hmmm."

All 11 S&P sector SPDR exchange-traded funds shaded green for the session, led by Communication Services XLC and the Discretionaries XLY. It should be noted that though all sectors rallied, four of the bottom five rungs on the daily performance table were occupied on Thursday by the sectors more defensive in nature.

Winners beat losers on Thursday by a rough 7-to-2 margin at the New York Stock Exchange and by about 7-to-4 at the Nasdaq. Advancing volume took a 70.6% share of composite NYSE-listed trade and a 63.8% share of composite Nasdaq-listed activity. The only fly in the ointment might have been that aggregate trading volume was lower on a day-over-day basis across listings of both exchanges, and quite sharply (-18.1%) for those names listed at the Nasdaq. It does appear that concerns over light trading volume possibly equaling a lack of conviction have dissipated overnight.

Foreign Demand

The U.S. Treasury held a third consecutive successful auction on Thursday. Maybe not quite as successful as the stellar auctions of Three Year and Ten-Year Notes earlier in the week, but solid, nonetheless. On Thursday afternoon, the Treasury Department sold $22 billion worth of 30-Year Bonds at a high yield of 4.015%. This trailed the "when issued" by 1.4 basis points at the time, which isn't wonderful, especially after the way the Ten Year Note auction on Wednesday has stopped through the "when issued."

That said, the internals were fine. Bid to cover was up from the August auction of this series, while Indirect (foreign accounts) Bidders took down an above-average 68.7% of the issuance. Direct (domestic) Bidders went home with 15.7% of the auction, which is not special. This left Dealers with a slightly below average 15.7% slice of the pie. Like I said: Not great, buy certainly not awful. Foreign demand has been the star of all three auctions this week. Can that continue as the U.S. Dollar starts to slide once again relative to its peers. A Fed that's more aggressive than anticipated on rate cuts will accelerate that process.

Two Ships Passing in The Night

Both Adobe ADBE and RH RH, which is the old Restoration Hardware, released quarterly earnings on Thursday night. RH is trading almost 20% higher overnight after gaining 3.8% on Thursday. The high-end bath-and-furniture retailer posted beats for both its top and bottom lines. While guidance on revenue was lackluster, guidance for demand is not. The company sees demand accelerating through the balance of this year through next year.

Adobe, on the other hand, is trading more than 8% lower overnight. Despite top- and bottom-line beats for the quarter reported, ADBE took current quarter guidance for both revenue and adjusted earnings below consensus.

News: Boeing's Bumpy Ride

Beleaguered U.S. industrial name Boeing BA is down almost 4% overnight, as the local chapter of the International Association of Machinists and Aerospace Workers Union voted down a new four-year labor deal with the aircraft manufacturer. The deal rejected included a 25% pay increase over four years. Average worker pay, with seniority, would have increased 33%. I root for anyone to get the best deal for themselves, so I don't take shots at anyone in that regard.

It's just that that was a decent offer and Boeing is not a company doing anything from a position of strength right now nor has it been doing anything from a position of strength for years. Should Boeing lose substantial business to their European, Brazilian, and even Chinese competitors due to being offline, this could end up being a situation of overplaying one's hand.

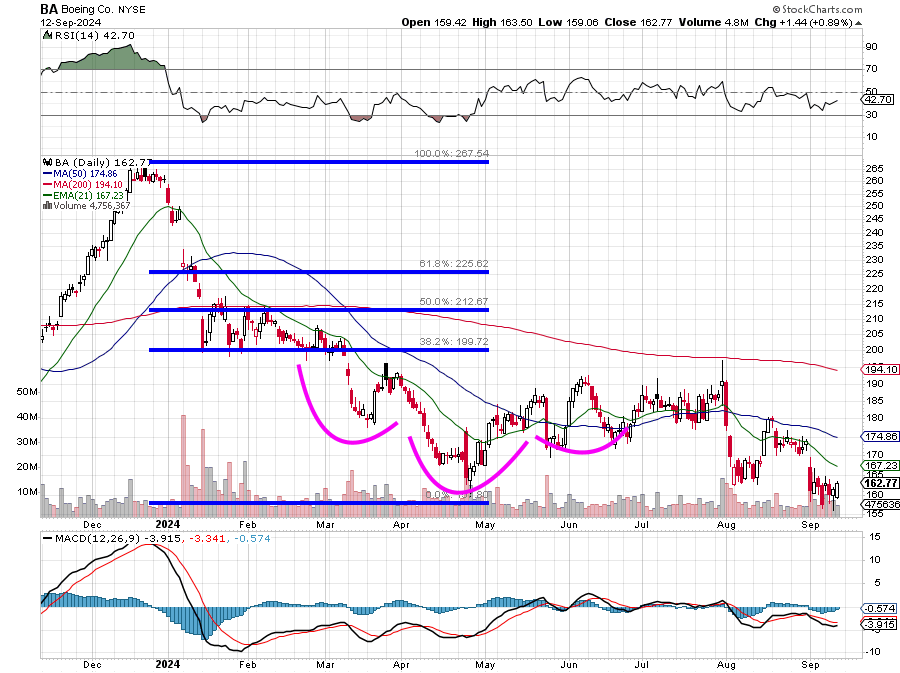

Readers will note that BA had put together an inverted head and shoulders pattern this past spring that failed at the stock's 200-day simple moving average, which also happened to be very close to a 38.2% Fibonacci retracement of the selloff that lasted from last December into April. Now the chart is very ugly. The last sale has moved to nearly two-year lows with a bearishly postured daily moving average convergence divergence.

Bloody Nose on the Wagon

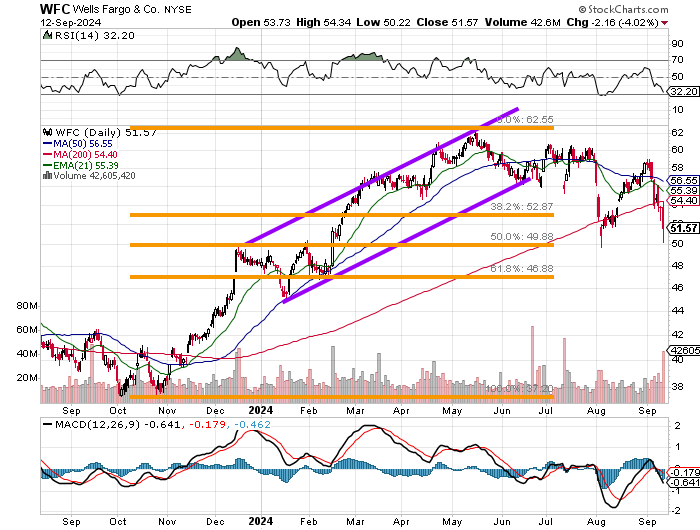

I have stuck with the one large bank in my portfolio as the group has shown weakness this September in the face of proposed increases to be made to its reserve requirements. On Thursday, I added to my long position in Wells Fargo WFC. Why? For one, they were not one of the banks warning on net interest margin this week, and two, I do believe that CEO Charlie Scharf is the one who can lead this firm away from its past.

Well, I got punched in the nose on Thursday. WFC gave up 4% on Thursday and is down 4.5% for the week after the Office of the Comptroller of the Currency issued an enforcement action against the bank due to deficiencies tied to its financial crimes risk management practices and anti-money laundering internal controls. The office and the bank have entered into a formal agreement requiring the lender to take comprehensive actions to enhance these practices.

Readers will see both "Relative Weakness" and a bearish daily MACD. They might also see twice-tested support for this stock at the $50 level. Though this spot is above my net basis, I see this "half-way" back spot of the October through May rally as a spot where perhaps one can trade short-term around a long-term core position. At least for now. Best case, I bail on the short-term trade at the 200-day simple moving average. Worst case, I'll puke it when the $50 support level cracks.

Economics (All Times Eastern)

08:30 a.m. - Export Prices (Aug): Expecting 0.5% m/m, Last 0.7% m/m.

08:30 - Import Prices (Aug): Expecting -0.2% m/m, Last 0.1% m/m.

10:00 - U of M Consumer Sentiment (Sep-adv): Expecting 68.1, Last 67.9.

10:00 - U of M One Year Out Inflation Expectations (Sep-adv): Last 2.8%.

10:00 - U of M Five Year Out Inflation Expectations (Sep-adv): Last 3.0%.

1:00 p.m. - Baker Hughes Total Rig Count (Weekly): Last 582.

1:00 - Baker Hughes Oil Rig Count (Weekly): Last 483.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle was long NVDA, WFC equity.