The Dollar Gets Bucked While Traders Have a Yen for the Yen

Have you looked at USDJPY lately?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

For the past few weeks, I have been talking about the US Dollar. First, it started when the Yen carry trade became the talk of the town in early August. But as stocks rallied, the Yen went off everyone’s screen. Why did we have to pay attention to the yen when the S&P was back over 5600?

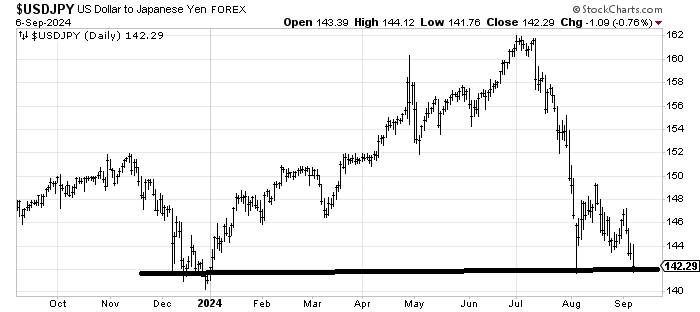

Have you looked at USDJPY lately? Of course, you haven’t. That’s because the talk is all recession or soft landing now, not yen carry trades. So please take a look: Dollar/Yen is where it was in early August. In fact, it is lower than where it was then because, on an intraday basis, it got down here (to 142) but never closed here. Yet, have you heard anyone chatter about it? I haven’t.

You can see 142 is a big level.

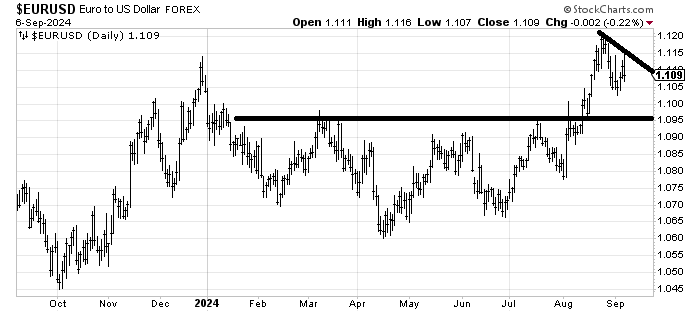

The Euro/USD looks a bit similar but notice that on Friday it could not reach the early August high of 1.12.

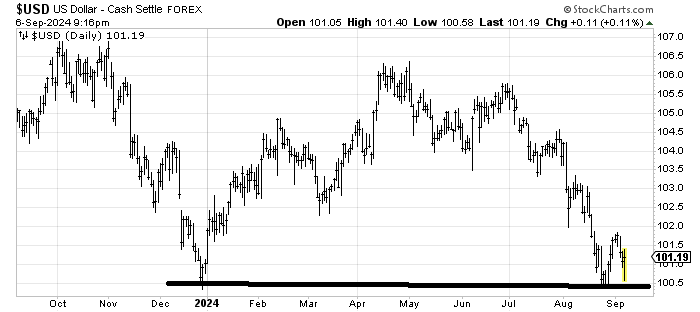

And that brings me back to the chart of the US Dollar Index. Friday it tried to break the early August (and late December) low and couldn’t. It actually closed green on the day. It has been my contention that this support should hold on the first trip back down (so far, it has).

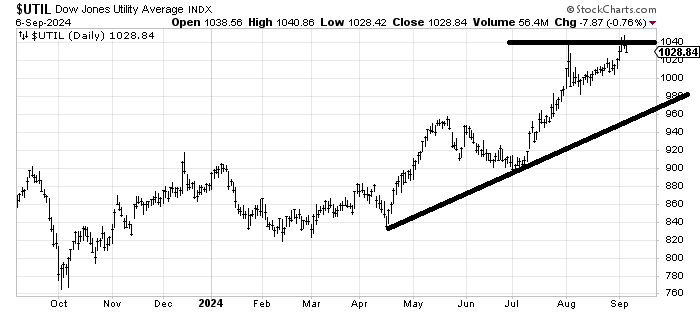

Now please take a look at the Utes. I thought they would not surpass that early August high but they did. Then Friday the rally became unsustainable and they closed lower on the day. I still think this 1040 area is a trouble spot for Utes and I do not like them up here.

Now let’s look at the Bonds, or the yield on the Ten-Year. Up until Friday, it had been hanging around the 3.8% support level, but that gave way on Friday. So we have to ask ourselves: are bonds the outlier as the leader (the buck and Utes will follow and Friday was an aberration?), or are interest rates out in left field and will realize that the others are not on the field with it? I think the latter, not the former.

As for stocks I still don’t think we have much panic, but we do, at least, have the put/call ratio back up over 1.0 on Friday. In early August, we had five straight days of readings over 1.0. But at least we finally saw some put buying which had been lacking most of last week.

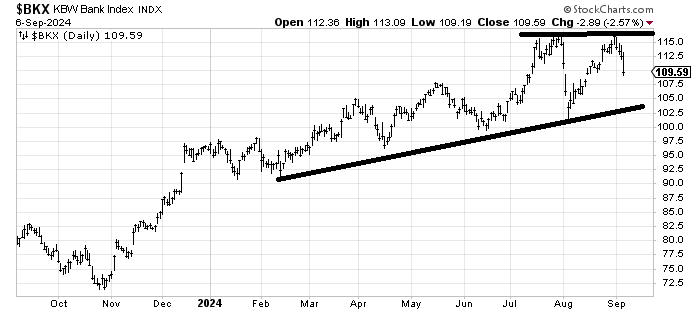

At least Friday, we saw folks finally sell their banks. That tells us something, too, when folks finally start selling their winners.

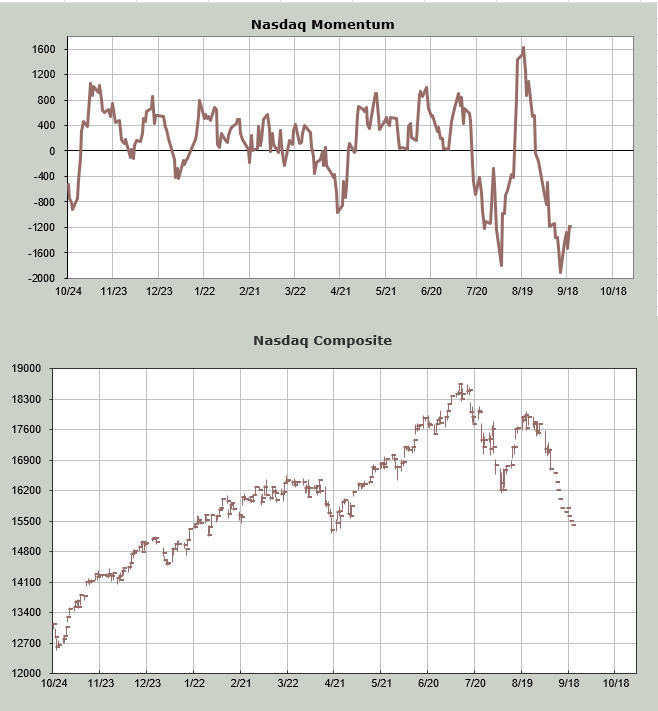

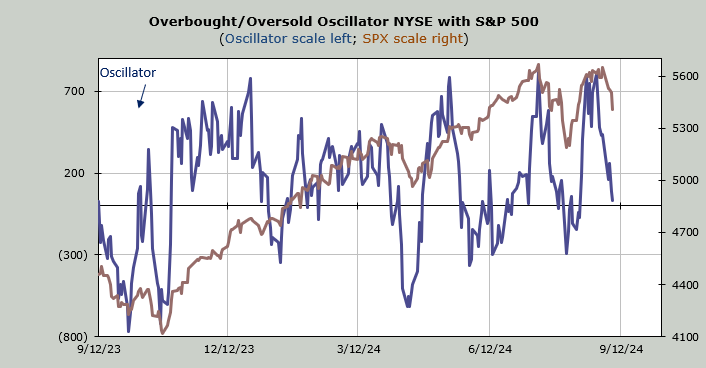

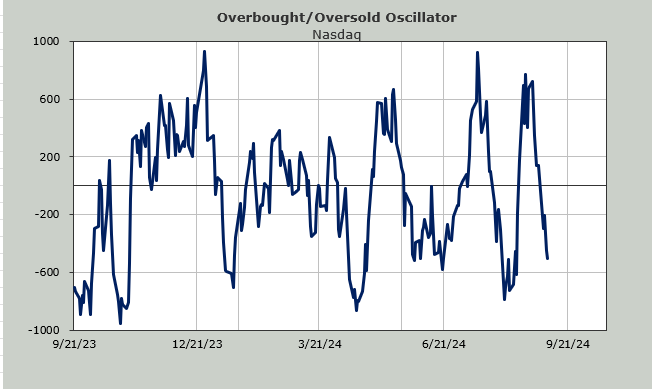

On an intermediate-term basis, we are nowhere near oversold but on a short-term basis, we’re getting a bit closer. My oscillator is based on breadth and, believe it or not, breadth on the NYSE has only been red five days of the last ten, so I can’t call it oversold. If I use the Nasdaq Momentum Indicator, which uses price not breadth I can make the case that we will be short-term oversold later this week.

If I do a what-if and walk Nasdaq down about 1500 points in the next week and change, this gets oversold on Friday. The exact day is not the point, it’s that I can finally find a general time frame.