The Calm Before the Storm, Consumer Un-Confidence, Nvidia, Wingstop What!?

Let's see what the Consumer Confidence report just dragged into the economic picture, and check charts for NVDA and WING.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Wednesday morning. Nothing. The raccoons and bobcats are scarce. Even the wind has dropped off, though that will change. Weather should start moving toward the Gulf of Mexico from the Caribbean later today. By tomorrow, if the current models hold true, the west coast of Florida up into Florida's "big bend" will face a potentially major hurricane, and then Georgia, the Carolinas and Tennessee will likely face some flooding. I am on the east coast of Florida. We supposedly will face little more than some heavy rain and tropical storm force winds.

Still, I am told by neighbors that the supermarkets have been emptied by nervous shoppers. I have flashlights. I have batteries. I have potable water. I have Cheerios. I'm good for now. Let's keep in mind those that may get into some unwelcome trouble this week as we proceed with our daily routines.

Broader equity markets have closed higher this week on both Monday and Tuesday, though trading volume remains quiet. Equity index futures came in hot on Tuesday as global equity markets roared in response to the PBOC's (China's central bank) broad steps taken to loosen policy and shore up that struggling economy. While the initiative was broad and somewhat expected, it was not quite the "big bazooka" that at least some economists were looking for.

Just a day later, as the globally euphoric response to the easing of monetary policy across the planet's second largest economy wore off, Asian markets were mixed on Tuesday as European markets opened just slightly in the red. That said, Chinese markets spent a second day in the green after the new program was announced. The Shanghai Composite closed up 1.16% with the Hang Seng Index in tow at +0.68%.

Here U.S. equity index futures are struggling to hold Tuesday's levels and are trading just a tad to slightly more than a tad below fair value. The U.S. Dollar Index is trading well below Monday's levels, but is off of its overnight lows. Front month gold futures are still trading up from Monday, but are well off of the overnight high of $2,694 per ounce. As for Treasury debt securities, the U,S, Ten- and Two-Year Notes are yielding overnight just about what they both paid going out on Tuesday.

Equity Marketplace

The S&P 500 made small gains on Tuesday, closing up 0.25% for the session, which was good enough for yet another record high close of 5,732. The Nasdaq Composite gained 0.56% for the session, while the more elite Nasdaq 100 gained just 0.47%. Among major to mid-major equity indices on Tuesday, all of the small- to mid-cap indexes barely moved at all, while the Dow Transports soared 1.67% on the backs of Uber Technologies UBER and FedEx FDX. The KBW Bank Index, and the Dow Utilities, however, moved in the other direction.

For the day, five sector SPDR exchange-traded funds closed in the green led by Materials XLB as traders pondered a weaker dollar. Five of these funds closed the day in the red, led lower by the Financials XLF. If you've quickly figured out that five plus five makes 10, you win a gold star. The Real Estate Select Sector fund XLRE closed the Tuesday session unchanged from Monday. Cyclicals and growth appeared to lead defensives for the day.

Winners beat losers by a rough 3 to 2 at the New York Stock Exchange and by about 5 to 4 at the Nasdaq. Advancing volume took a 63.8% share of composite NYSE-listed trade and a more commanding 72.2% share of composite Nasdaq-listed activity. While aggregate trading volume across the listings of both of New York's exchanges did increase day over day from Monday's totals, the gains were minute. The market has still not fully digested Friday's overwhelming trading volume. The macro today is still on the thin side, though earnings could get serious this evening when Micron Technology MU reports.

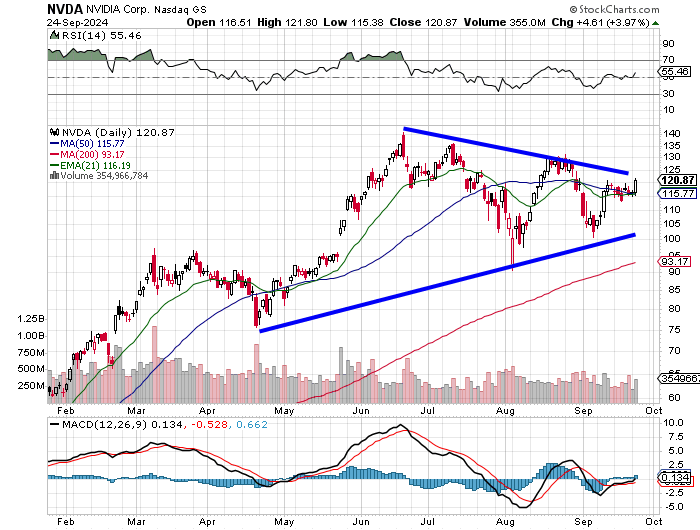

Nvidia Runs

Data center/gaming/generative AI elite-level chip designer Nvidia NVDA was suddenly thrust back into a market-leading role on Tuesday as the stock gained 3.97% for the session. The stock had been under pressure and had been moving sideways to lower since peaking just after the 10-for-1 stock split early this past summer. One reason for the pressure had been that CEO Jensen Huang had been monetizing part of his holdings, which he is certainly within his rights to do, especially after creating such titanic gains for us shareholders.

Well, on Tuesday, Barron's reported that Huang had completed a predetermined sale over time of six million shares from June 14 through Sept. 13 at prices ranging from $91.72 to $140.24. Huang is said to have grossed $713 million on those sales made through his Rule 10b5-1 plan at an average price of $118.83. The plan, which would expire this coming March is now complete. The account from which Huang sold those 6 million shares still holds 75.4 million shares, while Huang also owns 786 million additional shares through trusts and partnerships.

The stock rallied on Tuesday ... one, because Huang is done selling stock at least until March... two, because Huang still has such a large personal financial interest in the stock's performance, and three ... the Blackwell chips that had been delayed were reported across the Twittersphere to be on schedule to produce 450,000 units during the fourth-quarter of 2024, which implies a potential revenue generating opportunity of $10 billion for those chips alone.

Readers will notice the closing pennant pattern developed by NVDA since this past spring. This often foretells an explosive move in either direction. That said, the stock has just taken and moved off of its 50-day simple moving average to the upside, while Relative Strength has moved just north of neutral and the daily Moving Average Convergence Divergence indicator is very close to sending a bullish signal, though that signal has not yet been sent.

Within that daily MACD, the histogram of the 9-day exponential moving average has gone positive as the 12-day exponential moving average line has crossed above the 26-day exponential moving average line. That's a positive development but would pack more punch in my book if both of those lines were above zero. Currently, the 26-day line remains in negative territory.

Cries of Despair From the Conference Board

Did you hear that? I think that was the Conference Board's September read-out for Consumer Confidence. Jeekies, if the U.S. economy is still consumer-dependent and if this survey is accurate, the Federal Open Market Committee may not have cut the target for the Fed Funds Rate nearly as aggressively as it should have last week.

The headline number for the Consumer Confidence survey printed at 98.7 for September, down from an upwardly revised 105.6 in August and well below the 103.9 or so that had been the consensus view coming in. This number is often revised, so we'll hold our horses as far as taking what was reported as hard fact, but the implications within the report are terrifying.

First off, ahead of revisions, this is the second lowest headline reading for any month since mid-2022. Looking at past revisions, if this number held, it would be the third lowest. Just as a reminder, the average reading for 2019, the last pre-pandemic year, for the series was 127.9. Looking into the questions asked, those saying jobs were plentiful dropped to the lowest level since March of 2021, while those saying jobs were hard to get increased to the highest level since February of that year.

Additionally, consumer confidence dropped for the all-important 35 to 54 age group, decreased to levels not seen (ex-the Covid shutdowns) since 2014. The present situation for all age groups (ex-Covid) dropped to levels not seen since 2016.

September: Still Time to Blow It

Seasonality, Shmeasonality. To date, the S&P 500 is up 1.5% for the month of September. As I have mentioned in the past, going back to 1980, September has typically been a tough month for U.S. stocks, with the S&P 500 going negative for a majority of those years, while posting a negative mean return. The index has been "up" for nine of the past eleven sessions and I imagine that we owe much of this September's success to the FOMC and last Thursday's reaction to that group's shift in policy. Still a win is a win.

The S&P 500 closed out August at 5,648, and currently stands at 5,732. Counting today, there are four trading sessions left in the month. The last winning September for the S&P 500 came in 2019. The pressure is on.

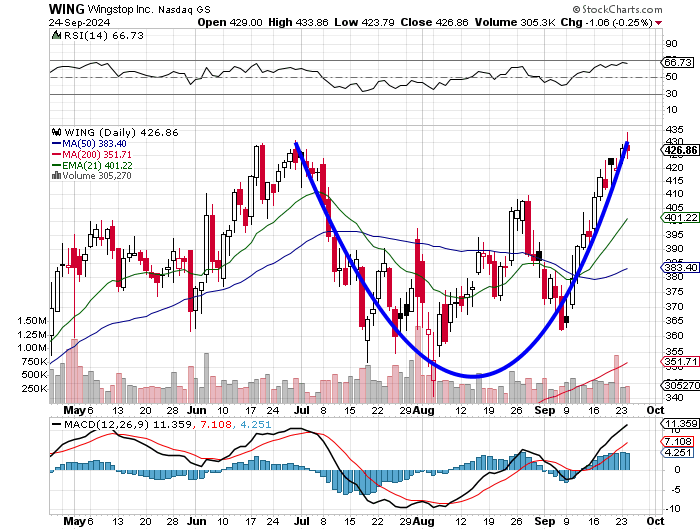

Anyone Else Notice Wingstop?

That Wingstop WING is either on the verge of trying to break out from a cup pattern with a $431 pivot....

.... Or is about to add a handle to that pattern, which would swing the pivot from the left-side apex of the cup to the right-side apex. Either way, both the Relative Strength Index and daily MACD are postured for success. I am not long this name. Not yet anyway. We could be talking about a $500-plus target price.

Economics (All Times Eastern)

07:00 a.m. - MBA 30 Year Mortgage Rate (Weekly): Last 6.15%.

07:00 - MBA Mortgage Applications (Weekly): Last 14.2% w/w.

10:00 - New Home Sales (Aug): Expecting 695K, Last 739K SAAR.

10:30 - Oil Inventories (Weekly): Last -1.63M.

10:30 - Gasoline Stocks (Weekly): Last +69K.

The Fed (All Times Eastern)

4:00 - p.m. Speaker: Reserve Board Gov. Adriana Kugler.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: CTAS (1.00)

After the Close: JEF (.77), MU (1.11)

At the time of publication, Guilfoyle was long NVDA equity.