The Buck Muscles Up

The U.S. Dollar Index tiptoed higher by Friday, but that index fails to include two key currencies. Also, a look at Trump's Treasury pick, crypto, the S&P's chart and more.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The U.S. Dollar Index tiptoed above the 108 level very early on Friday morning. The index, also known as the "Dixie," is a weighted measure of the value of the dollar in relative terms, against a basket of peer-reserve currencies. The index was designed by and is published by Intercontinental Exchange Inc. ICE. The index is by far most heavily weighted against the euro, with the Japanese yen, British pound, and Canadian dollar all represented to a far lesser, but still significant degree. Much lighter weightings are borne against the Swedish krona and the Swiss franc.

Is this a fair and accurate measure of the dollar's strength? That's debatable, as the index does not include the two largest U.S. trade partners as measured by exports. No. 1 would be China, and Mexico would be in second place, with Canada in third. A better measure of dollar strength in my opinion, would have to include both the yuan and the peso. That said, by trend on a chart, the U.S. Dollar Index is similar in appearance to the WSJ (Wall Street Journal) Dollar Index.

This index, only around since 2021, is also weighted, but using data provided by the Bank for International Settlements (BIS) and includes 16-dollar-currency pairs. These 16 currencies include the yuan and the peso, and together account for about 80% of cross-border world trade. The index is re-weighted every three years.

King Dollar

Back to where I had started, before I got off on a technical tangent on measuring U.S. dollar valuations. That U.S. dollar index, mentioned above, is up more than 3% since the election (or is it re-election) of Pres. Elect (or is it former president?) Trump and almost 7% since it became fairly obvious that his election was becoming more and more likely back in September. Treasury yields are up fairly significantly over that time frame as well. One might have thought that with a central bank talking about easing ahead of reaching targeted levels for consumer level inflation, that the dollar and yields from the belly of the curve on out to the long end might have done the opposite.

Are Treasury yields pricing in a tariff-created wave of inflation? Not likely. Inflation was already re-accelerating and actually appears to be accelerating a little more slowly than it was several weeks ago, at least according to the Hedgeye model for the consumer price index, which is something I pay for and has not only been more accurate than other models, but ahead of them as far as timing is concerned as well.

Why the dollar strength? Expectations for organic economic growth due to a less stringent regulatory and a less vampirical fiscal environment? Pricing in less taxes and instead of fiscal largess, the insistence that the bureaucratic nightmare in D.C. become more efficient and behave more like a business? Just maybe. There is no doubt that something unforeseen only a few months ago is a foot and it surprisingly does not feel like the continued debasement of the fiat. Well, in relative terms anyway. Anyone long gold or bitcoin might still feel like a debasement is under way.

Oh, one other thing. If the value of the dollar rises vs. a trading partner, that of course works to offset the inflationary impact, as far as consumers are concerned, that might arise due to increased tariffs. Then again, much of the tariff talk might just be negotiated in nature, but with the threat of realism behind them as they have been used before, by this leader. Just some food for thought.

Monday Morning

U.S. equity index futures markets are trading higher as the clock ticks quietly through the zero-dark hours. The U.S. dollar that I just wrote of appears to be trying to pause and catch its breath, which in conjunction with rumors of a potential ceasefire agreement between Israel and Hezbollah, is pressuring oil prices. Financial markets appear, at least since Friday, but really for all of the past week, to be reacting well to the idea that Scott Bessent had been elected by Pres. Elect Trump to become, if confirmed, the 79th Secretary of the U.S. Treasury Department. Bessent runs Key Square, which is a macro-focused hedge fund and has worked as CIO for investor George Soros.

Bessent has been a frequent critic of this Fed's policies, and of current Fed Chair Jerome Powell in particular, having even suggested the creation of a "shadow" Fed Chair that might best imply where monetary policy might go when Powell's term at the Board of Governors expires in May 2026, rather than allow the current regime to impact markets through forward guidance. Does that happen? I have my doubts. Will it give us something to think about? Definitely.

The Week That Was

Last week was positive for U.S. financial markets. One might have expected otherwise as the week started out, as the war in eastern Europe intensified. Both Russian and Ukrainian armed forces seem to be trying to best position themselves ahead of the inauguration of the new administration in the U.S. The idea seems to both be taking advantage of the current lame duck administration and the belief that the new one will not tolerate the financial burden of the ongoing conflict.

Strange that markets would ultimately post a solid weekly performance after Russian Pres. Vladimir Putin would update Moscow's doctrine governing the use of nuclear weapons in combat in a veiled threat against the U.S. and its NATO allies. Just as strange that markets would do well after the U.S. had authorized the use of American long-range missiles into Russian territory. This did put a bid under both gold and Bitcoin last week despite the stronger U.S. dollar.

About Bitcoin, the digital asset (Is it a currency? Is it a commodity?) flirted with reaching the $100,000 level toward the end of the past week, sold off a bit on Sunday and appears to be readying another attempt at the milestone level in dollar terms this morning. I am not sure, which is the bigger deal for Bitcoin, the $100,000 per token level, or the $2 trillion in market cap level that run nearly together. The incredible thing about this latest run in Bitcoin and for "crypto" is that obviously broader acceptance of late as the incoming administration is clearly the most pro-crypto U.S. administration yet. Whatever the "Trump Trade" is, Bitcoin is quite overtly, a part of it.

From a corporate perspective, the event of the week was the release of Nvidia's NVDA third quarter earnings. The elite chip designer almost doubled it's quarterly revenue yet again, while setting records for its Data Center / AI business. The fly in the ointment, as NVDA did not participate in last week's robust equity market rally, was the fact that the firm's outlook for current quarter revenue generation, while above consensus, did not blow anyone away, and did not top the higher end of the range of professional estimates.

Additionally, the U.S. Department of Justice officially proposed the breakup of Alphabet GOOGL in its current form, with the idea of selling off some key pieces of the Google puzzle such as the Chrome web browser and separating the app store from the Android operating system for mobile devices.

Speaking of Bitcoin...

Anyone else notice that Bloomberg News, over the weekend, was reporting that the firm of the president elect's choice to run Commerce, Howard Lutnick (of Cantor Fitzgerald), was in talks with Tether to launch a multi-billion-dollar program to lend fiat to clients against Bitcoin? Apparently, Cantor is talking about funding a program that would start at $2 billion and might be projected to reach tens of billions. Interestingly, also over the weekend, the Wall Street Journal reported that Cantor Fitzgerald had agreed to take a 5% stake in Tether this past year for a rough $600 million at that time.

The GDP Game

Early last week, the Atlanta Fed revised their GDPNow model for the fourth quarter to growth of 2.6%, up from 2.5% (q/q, SAAR). Among other central banks running close to real-time GDP models for the current quarter, the New York Fed estimates Q4 growth at 1.91%, while the Cleveland Fed sees Q4 growth of 1.84% And the St. Louis Fed is down at growth of 1.55% for the current quarter. The Atlanta Fed model is the best known of the four. That said, Atlanta currently is by far the most optimistic among these four models created by regional Fed district branches, and that optimism appears to be an outlier view.

Charts

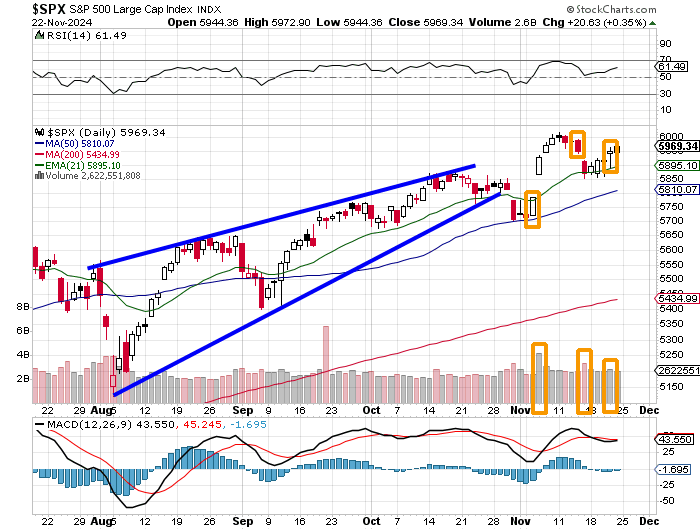

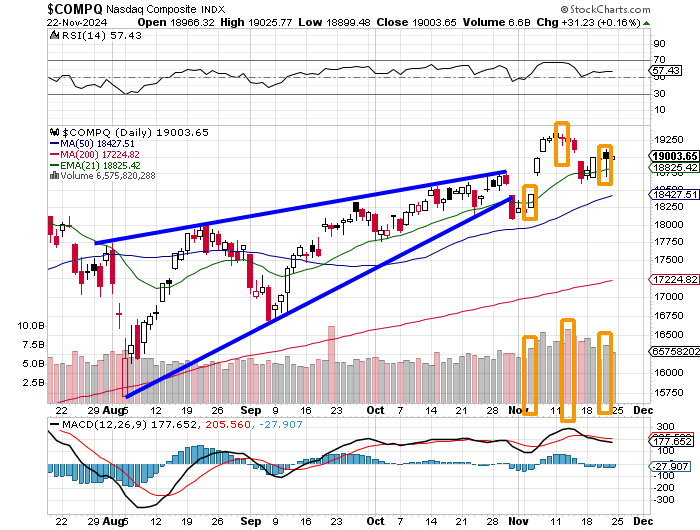

Right now, the major indexes, as we reminded readers late last week, are positioned for some short-term upside. Thursday, was for both the S&P 500 and the Nasdaq Composite a potential "day one" upside change in trend in search of confirmation...

Readers will see that for the S&P 500, Relative Strength he started to curl into a more bullish looking position, while the daily Moving Average Convergence Divergence for the index, not yet positive, appears to be ready to move into a more bullish posture.

The daily Moving Average Convergence Divergence indicator for the Nasdaq Composite seems a little further away from such a bullish posture as does the S&P 500. What both indexes need, from a bullish trader's point of view, would be a crossover of the 26-day exponential moving average by the 12-day exponential moving average, while the histogram of the 9-day exponential moving average moves above zero. A day of confirmation at some point this holiday week, would likely get that done. Note the outperformance last week by the small to midcap indexes vs. the large caps.

As for the major to mid-major U.S. equity indices last week....

- The S&P 500 gained 0.35% on Friday to close the week up 1.68%.

- The Nasdaq Composite gained 0.16% on Friday to close the week up 1.73%.

- The Nasdaq 100 gained 0.17% on Friday to close the week up 1.87%.

- The Russell 2000 gained 1.8% on Friday, to close the week up 4.46%.

- The S&P Small Cap 600 gained 1.68% on Friday to close the week up 3.72%.

- The S&P Mid Cap 400 gained 1.67% on Friday, closing the week up 4.19%.

- The Dow Transports gained 1.13% on Friday to close the week up just 0.81%.

- The Philly Semiconductors gave up 0.15% on Friday, but still closed the week up 2.53%.

- The KBW Bank Index gained 1.53% on Friday, closing the week up 1.96%.

On Friday, nine of the eleven S&P sector SPDR exchange-traded funds closed in the green, with the Discretionaries XLY out in front at +1.44%. The Industrials XLI and Financials XLF both gained more than 1% for the day as well.

For the week, all 11 S&P sector SPDR ETFs closed in the green as the Materials XLB gained 3.08%. Eight of these 11 funds gained at least 2% over the five days, as the Materials were followed closely by the Utilities XLU and Energy XLE. No fund among the eleven gained less than 1.64% for the period.

Earnings and S&P Valuation

According to FactSet, which is the service that readers know I rely on for all things earnings-related, third quarter results are just about finished. Currently, for the third quarter, with 95% of the S&P 500 having already reported, S&P 500 earnings are showing blended (results & expectations) year over year growth of 5.8%. Revenue growth is currently running at blended growth of 5.6%. Q4 earnings growth is now seen at 12.0% on revenue growth of 4.7%. Full year earnings growth is seen at 9.4 on revenue growth of 5.0%.

For the third quarter, double-digit earnings growth is now only expected from the Communication Services (+23.2%), and Health Care (+13.6%) sectors. Expectations for Tech sector earnings growth have dropped all the way from +15.6% to just +6.4% and then perked up a little to the current level of 8.8%. The Utilities, Materials, Industrials and Energy (-25.5%) sectors are all expected to post year over year earnings contraction.

The S&P 500 goes into this week trading at 22.0-times forward looking earnings, which is still well above the five- and ten-year averages for the index of 19.6- and 18.1-times, respectively. The S&P 500 also trades at 28.1-times trailing 12 months' earnings, which is also well above its five- and ten-year averages of 24.0-times and 21.9-times.

The Week Ahead

Traders and investors can look forward to working less this week. Though one cannot really call the week "holiday-shortened", this Thursday will be Thanksgiving Day in the US. Financial markets will be closed but will reopen for a "half-day" regular session on Friday. The closing bells at 11 Wall St. and up at Times Square will ring at 1 p.m. ET on Friday, which is three hours early. This, by the way, will force an economic data dump on Wednesday.

As far as coming macroeconomic data is concerned, this week it all lands on Tuesday and Wednesday. Tomorrow, we'll see the September HPIs from Case-Shiller and the FHFA, while New Home Sales for October hits. The November editions of the Conference Board's Consumer Confidence survey and the Richmond Fed manufacturing Index will both also cross the tape.

Wednesday will bring with it an absolute deluge of numbers as October Durable Goods Orders, October Wholesale Inventories, and October Personal Income and Spending all hit the tape. On top of that, Q2 GDP will be revised, the weekly numbers for jobless claims will print a day early and the data for September PCE price inflation will print. This one rarely surprises and more will be made of it by the media than it really warrants.

This will be a very thin week from a corporate earnings' perspective. That said, there are a few headliners in the mix. Tonight, we'll hear from Zoom Video ZM, Then Tuesday will bring with it most of the earnings we will see for the week. On Tuesday morning, Best Buy BBY, and Dick's Sporting Goods DKS will report. They will be followed on Tuesday afternoon by CrowdStrike Holdings CRWD, Dell Technology DELL, and HP Inc HPQ.

What Else? Fun and Games

- Somehow Army hung onto a top 25 ranking in both polls on Sunday after being bludgeoned by Notre Dame on Saturday Night.

- The fourth quarter of the Dallas / Washington game on Sunday might have been the most entertaining quarter of pro football I have seen in a very long time.

- Still nothing to report on the Juan Soto front.

Economics (All Times Eastern)

10:30 a.m. - Dallas Fed Manufacturing Index (Nov): Expecting 1, Last -3.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: BBWI (.47)

After the Close: A (1.41), ZM (1.31)

At the time of publication, Guilfoyle was long NVDA, CRWD, XLU.