Thanksgiving Week Data Dump

Let's take a look at the numbers landing today on housing and the consumer, Trump's picks, the Nasdaq Composite's charts and how even defense could go on a diet soon.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Welcome. The poem says that Tuesday's child is full of grace. I'm not sure that I know anything about Tuesday's child, but I do know that for this week at least, Tuesday is the first day of a two-day data dump. That's because Monday was quiet, Thursday is a federal holiday, and Friday is Black Friday. While we will work a half-day this Friday and many of those working at the retail levels will probably work more than full-time that day, the economic schedule will be almost non-existent.

This week's corporate earnings release calendar is almost completely confined to this morning, starring a few retailers and this afternoon starring among other tech stocks, CrowdStrike Holdings CRWD, which is still a Sarge name, and caught a bit of a beat-down (-2.3%) on Monday. Though the heavier day from a macroeconomic perspective is Wednesday, there will be enough domestic data-points released this morning to talk about.

Headlining the macro on Tuesday will be the two home price indexes for September, and November consumer confidence. That last item, the consumer confidence survey for November, released by the Conference Board, will likely be put under something of a microscope this morning. Why? Well, the semi-similar November consumer, which is released by the University of Michigan, was revised significantly lower this past Friday, showing improvement from October, but far less improvement than the advance release of that month series showed.

Foreign Policy-Elect

How interesting Monday's action was. Over the course of my long career, Fridays have tended to be busier days than Mondays. Mondays have often been among the quieter days of the week. We saw a development across our marketplace on Monday that I am not sure fits neatly into what I am seeing as the zero-dark hours pass on Tuesday morning, but what is there, is there. Let's explore.

Domestic-equity-index futures are trading a little lower early on Tuesday morning, as European and Asian markets have both sold off a bit. On Tuesday evening, Pres.-Elect Donald Trump threatened to impose 25% tariffs on all products imported from both Canada and Mexico because of what he called the level of drugs and criminals coming across U.S. borders. The president-elect also threatened to place an additional 10% tariff on goods imported from China because of the amount of Fentanyl believed to be coming in from that country.

The president-elect may be trying to provoke increased cooperation from these key trading partners, and this may be a negotiatory tactic. We do know that Pres.-Elect Trump is both more than willing to bargain and more than willing to act if not satisfied. That is having an impact on global equities and U.S. equity index futures this morning.

What we do know is that Scott Bessent, who is Trump's pick to run the Treasury Department, which is responsible for the imposition of tariffs, has written recently (in an op-ed at the Fox News website that tariffs are a "useful tool." Bessent sees tariffs as a means to an end, potentially playing "a central role" in reaching Trump's "foreign policy objectives."

Speaking of Scott Bessent ...

U.S. financial markets have fallen in love with his "3-3-3" plan. The plan includes reducing the federal budget deficit by 3% by the year 2028, increasing GDP growth by 3%, mostly through deregulatory policies and boosting domestic oil production by 3 million barrels per day. Is this the way to grow the U.S. economy organically (as opposed to fiscal recklessness that aided the few at the expense of the many), while keeping inflation in check? The markets appear to think so.

Market Developments

Regardless of what else makes headlines, charts are charts, and the charts tried to tell us something on Monday. The major equity indexes may have been up moderately, but broader markets were rather hot on Monday. Forget that Bitcoin and gold took a gut punch on Monday. Yes. I am long gold and that was severe, but not entirely out of left field. Treasuries were in huge demand on Monday. By day's end, the U.S. Ten Year Note and Two Year Note both paid just 4.26%, threatening to re-invert that spread. That was down 14-basis points for the yield of the Ten Year and down 11 basis points for the yield of the Two Year.

The S&P 500 gained 0.3% on Monday, while the Nasdaq Composite and Nasdaq 100 gained 0.27% and just 0.14% respectively. Once we got past the majors, however, the less focused upon equity indexes all did better. The Dow Industrials gained 0.99% on the day, setting a new closing record high. The Dow Transports soared 2.23%, while all of the small to midcap indexes gained at least 1.45% for the session.

Nine of the 11 S&P sector SPDR exchange-traded funds shaded into the green on Monday, led by the REITs XLRE at +1.34%, and followed by the Materials XLB and Discretionaries XLY. Both of those funds gained more than 1% as well. Energy XLE took a serious beating (-1.97%), while Technology XLK closed unchanged.

Very oddly, within tech, the Philadelphia Semiconductor Index was up 0.65%, while the Dow Jones U.S. Semiconductor Index, in theory measuring the same activity, was down 1.93%. Things that make you go hmmm? Nvidia NVDA took a 4.18% pounding, followed by Taiwan Semiconductor TSM, which was down 2.63%.

Pay Close Attention Here

Winners beat losers by almost three to one at the NYSE and by more than two to one at the Nasdaq, Advancing volume took a 66.7% share of composite NYSE-listed trade and a 66.1% share of composite Nasdaq-listed activity. Now, I often write that we like to see a break between the "day one" of a market change in direction and a "day of confirmation." While it is true that Friday was an "up day" for US equities, trading volume took that day off.

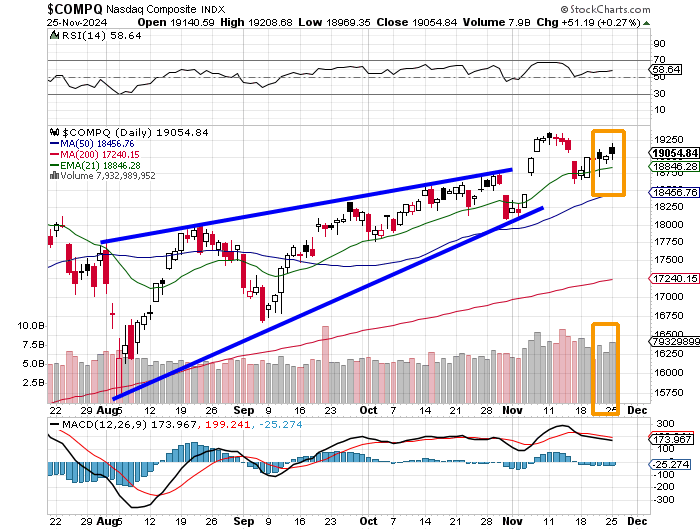

On Monday, aggregate trade across NYSE-listed securities was up 36% day over day, while aggregate trade across all Nasdaq-listed securities was up 20.6% day over day. Those are huge jumps in activity on the Monday of a holiday week. Hmmm. What do the charts say? I'm glad you asked. The charts are similar, but what I am trying to show is more pronounced in the daily chart of the Nasdaq Composite. Let's have a look:

Readers will see that while the market technically turned in a northerly direction last Wednesday, the more significant move and the trading volume showed up on Thursday, Day One. Then look at that drop-off in trading volume on Friday, only to be followed by another up day on huge trading volume on Monday. I would have preferred a couple of days in between or maybe even a red candle session, but we do have what looks like a volume-based confirmation of an uptrend going into the holiday season. Now, it's up to the market not to make a liar out of me.

Defense: Slow to Add Exposure

Yes, I see the weakness of late across aerospace and defense contractors. No, I have not been adding on this dip. One reason I have almost always been long this group was because I knew how large a part of the fiscal pie this is / was, with very little done to make sure these dollars were well-spent.

On Monday, three-star rated (by TipRanks) analyst Douglas Harned of Berstein wrote, "We expect Trump to seek a strong defense as he did in his first term, even if he seeks to avoid involvement in overseas conflicts. Trump has been vocal about the need for strong nuclear deterrence, missile defense, and expansion of space capabilities."

Harned is not wrong in these thoughts. We also know that there is talk in Europe about increasing defense spending across the NATO alliance. What has the war in eastern Europe told us, though? That perhaps the peak days of fighter aircraft, tank formations, and, gulp, naval fleets patterned around aircraft carriers are relics of the past. If we ever fight World War II again or engage in a war against a technologically inferior opponent, we are all set.

This Department of Government Efficiency to be led by Elon Musk and Vivek Ramaswamy will be for real. So will be the appointment of Russ Vought to lead the U.S. Office of Management and Budget or "OMB", where Vought has led before. There is going to be an overhaul in overall fiscal spending, and I do not plan to be surprised when the Pentagon is no longer untouchable.

Yes, certain weapons systems should and will remain untouchable, but others? We all know there is some fat here.

Musk tweeted on Monday. "The F-35 design was broken at the requirements level, because it was required to be too many things to too many people."

Later in the same post, Musk expanded, "And manned fighter jets are obsolete in the age of drones anyway. Will just get pilots killed." I must admit that I have wondered that same thought for some time. Do drones take over for fighter aircraft? That's possible.

Do drones take over in the sense that one jet fighter is guarded and protected by a small group of drones? I find that extremely likely. How about using the same thesis for tanks or naval vessels? Why not? Defense contractors are not going away. I remain long, but I am not adding on this dip, and I have taken some profits in order to right-size this group as we go into something we don't truly understand. That is the transition of defense spending from big ticket items to more effective, less bulky systems.

Don't get me wrong. I absolutely loved the rumble of a column of M-60A1 main battle tanks from a couple of miles out as they pull up into your unit's position and stop with one on each side of each foxhole. I felt like nothing could stop us in those moments. Ever call in an airstrike and just watch the fireworks? Those things were wonderful, but I have become an old man. That way of thinking, that way of fighting, will only mass troops and equipment for slaughter for the style of warfare that comes.

We must evolve. So must the troops. The invincible tortoise must once again become swift, silent, and deadly. Always Faithful.

Economics (All Times Eastern)

08:55 - Redbook (Weekly): Last 5.1% y/y.

09:00 - Case-Shiller HPI (Sep): Expecting 4.9% y/y, Last 5.2% y/y.

09:00 - FHFA HPI (Sep): Expecting 0.2% m/m, Last 0.3% m/m.

10:00 - CB Consumer Confidence (Nov): Expecting 727K, Last 738K SAAR.

10:00 - New Home Sales (Oct): Expecting 112, Last 108.7.

10:00 - Richmond Fed Manufacturing Index (Nov): Expecting -9, Last -14.

4:30 p.m. - API Oil Inventories (Weekly): Last +4.753M.

The Fed (All Times Eastern)

2:00 p.m. - FOMC Minutes.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: ANF (2.35), ADI (1.64), BBY (1.29), BURL (1.55), DKS (2.69), SJM (2.51), KSS (.28), M (-.01)

After the Close: CRWD (.81), DELL (2.05), HPQ (.93), JWN (.22), WDAY (1.76)

At the time of publication, Guilfolye was long CRWD, NVDA equity.