Stocks Swim in Boots, Tesla Stalls Out, Rotation Back in Motion, Global Weakness

Perhaps the real reason for overnight pressure did not come from either Tesla or Alphabet. Just beneath the surface of those headliners, lurked something else more troubling.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Ever try to swim fully clothed? Or in boots? You get really heavy really quickly.

That's what happened to equities late in the Tuesday regular session. That's what happened after-hours after Tesla TSLA and Alphabet GOOGL reported. That's what happened overnight as U.S. equity index futures softened, global equities sold off and U.S. Treasuries found a bid.

We can put the blame wherever we want to, but I thought on Tuesday afternoon that the optimism for U.S. equities had been sucked out of the room ahead of those earnings reports. The market had, it seemed, flipped from moderately hopeful mode to preservation of capital mode. Sure, the day ended only slightly in the red for the major large cap indexes, but stocks put the rotation out of most large-caps and into smaller-caps back into motion a little ahead of lunchtime and then in earnest later in the afternoon.

I can understand the overnight disappointment in Tesla. Yes, we knew Tesla had a rather tough quarter coming in. That made no difference. Tesla earnings fell short of consensus for the fourth consecutive quarter, and though revenue generation did manage to beat Wall Street expectations for the second quarter, ending a three-quarters long losing streak, margins still suffered. That stock is trading 7% lower overnight.

Alphabet, on the other hand, had an undeniably solid quarter. The company posted top and bottom-line beats, and impressive growth in operating income across Google Services and Google Cloud. YouTube ads, however, fell short of expectations. Alphabet also warned that expenses would rise during the current quarter. GOOG and GOOGL are down almost 3% overnight.

Perhaps the Real Reason?

Perhaps the real reason for this overnight pressure did not come from either Tesla or Alphabet. Sure, those two stocks were the headliners, but just beneath the headline level, Visa V disappointed for the quarter on both the top and bottom lines.

The issue is this... growth in total payment volume, cross-border volume, and processed transactions all decelerated form the previous quarter. During the call, CFO Chris Suh spoke of stabilizing U.S. demand for goods through e-commerce post-pandemic and expressed a lack of certainty on whether or not that stabilization will come at pre-pandemic levels.

Weakness Went Global

Asian stocks were already weaker following U.S. overnight weakness. Then it was Europe's turn. European equities opened on weakness as German, French, and EMU July manufacturing PMI, already expected to print in contraction, hit the tape in an even deeper state of decline than expected.

Services PMIs, while still in expansionary territory, decelerated from June in Germany, as well as across the EMU. One bright spot was outside of the European Union. July manufacturing and services PMIs for July both crossed the tape in expansion for the U.K. This at least slowed the early selloff across the continent.

Tuesday's Market

The rotation that had appeared last week, that then disappeared for a couple of days, came back with a vengeance on Tuesday. The Nasdaq 100 gave up 0.35% for the session after having been up earlier in the day. The same can be said for the S&P 500 (-0.16%) and Nasdaq Composite (-0.06%), led lower by the Philadelphia Semiconductor Index (-1.46%).

There was joy in small-cap land as the Russell 2000 gained 1.02% and the S&P 600 gained 0.72%. Unfortunately, the Dow Transports did not join the small-caps in the winners' circle on Wednesday as they had in the past. That index was down 1.54% as United Parcel Service UPS was severely beaten for a loss of 12.05%.

Nine of the 11 S&P sector SPDR ETFs shaded into the red on Tuesday, with Energy XLE leading the way lower at -1.59%. No other fund among the 11 even gave up more than 0.65%. Materials XLB were the day's winners, up 0.39%.

Breadth did not really tell much of a story on Tuesday. Winners beat losers at the NYSE by just a smidge, and by almost 4 to 3 at the Nasdaq. However, advancing volume took a minority share of composite trade for names listed at both exchanges. Aggregate trade was up small day over day for NYSE listings, but down small day over day for Nasdaq listings. They say that "Dead men tell no tales." On Tuesday, the numbers simply did not tell a tale.

Tremendous Demand at Auction

Anyone else notice Tuesday's auction of $69 billion in new U.S. 2-Year Notes? Wow. Kind of like opening a two-pack of Hostess cupcakes thinking you'll just eat one.

The high yield printed at 4.434%, stopping through the "when issued" at the time and the lowest such yield since January. Bid to cover hit the tape at 2.814, well above the six-month moving average of 2.58. That's all good, but the internals were stunning.

Indirect (foreign accounts) bidders took down a whopping 76.6% of the auction, which was their highest slice of the pie for this series on record. Direct (domestic accounts) bidders grabbed just 14.4%, but that did not matter much as dealers were "stuck" with a mere 9% of the issuance. This too was an all-time record, on the low side, for this series. All ahead of next week's FOMC policy meeting.

Tough Day for the Macro

Tuesday was a rather rough day for the U.S. economy. The Richmond Fed Manufacturing Index for July printed at a headline -17, down from -10 in June and well below expectations. New Orders, Shipments, Order Backlog and Capacity Utilization were all exceedingly weak. Wages were higher, as were prices paid and prices received. Not surprisingly, the number of employees fell into a deeper state of contraction. The Richmond district has not had a month of positive growth for its manufacturing sector since January.

Perhaps even more startling, the Philadelphia Fed posted its non-manufacturing (services) survey for July. At the headline, Philly's service sector fell into contraction after having been in expansion in June. New orders, Unfilled Orders, Inventories, Full-Time Employees, and Average Workweek all moved from expansion into contraction. What continued to grow? Exactly what you feared... prices paid, prices received, and wages.

Additionally, June Existing Home Sales dropped 5.4% from May to 3.89M SAAR (seasonally adjusted annualized rate). Though this was the weakest print for this series this year, that did not stop the median home sales price from rising 4.1% to $426.9K.

After this morning's releases of June Wholesale Inventories, June New Home Sales, and June Goods Trade Balance, the Atlanta Fed will revise their GDPNow model for the second quarter for the final time ahead of the BEA's first estimate for the quarter on Thursday morning.

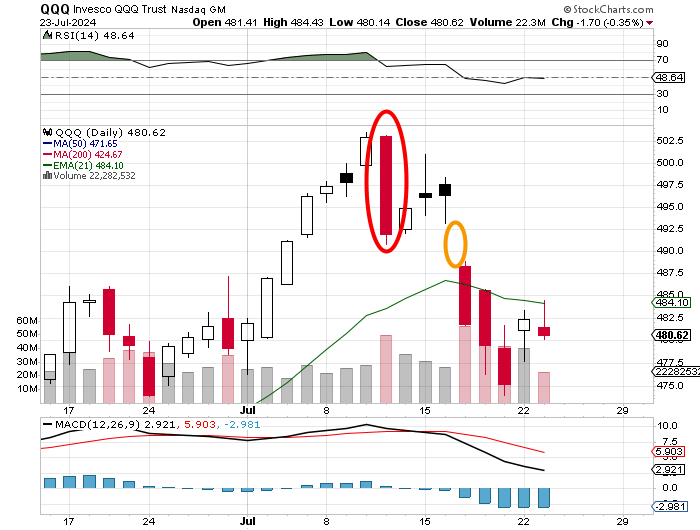

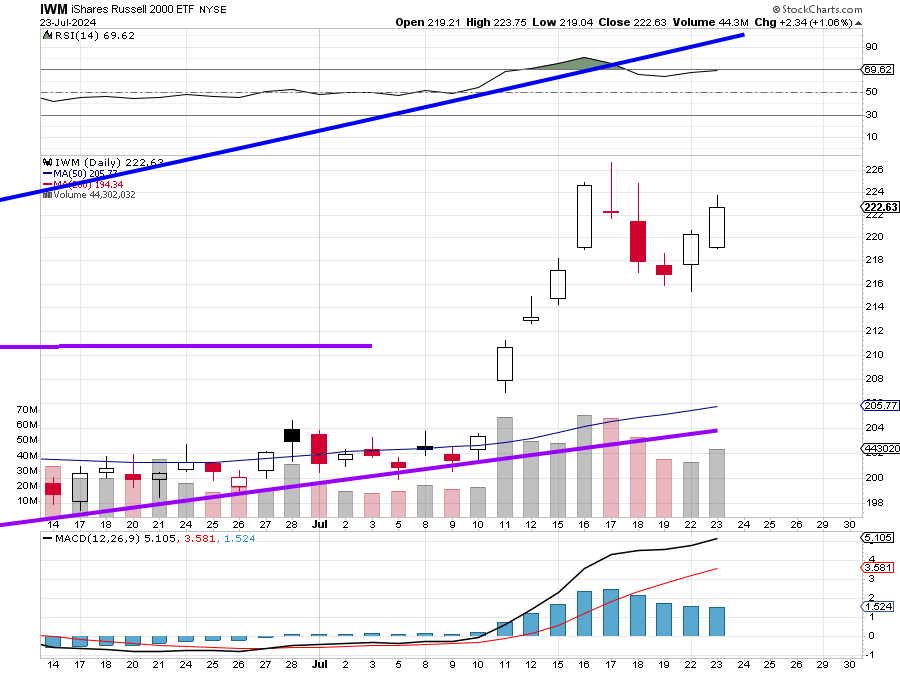

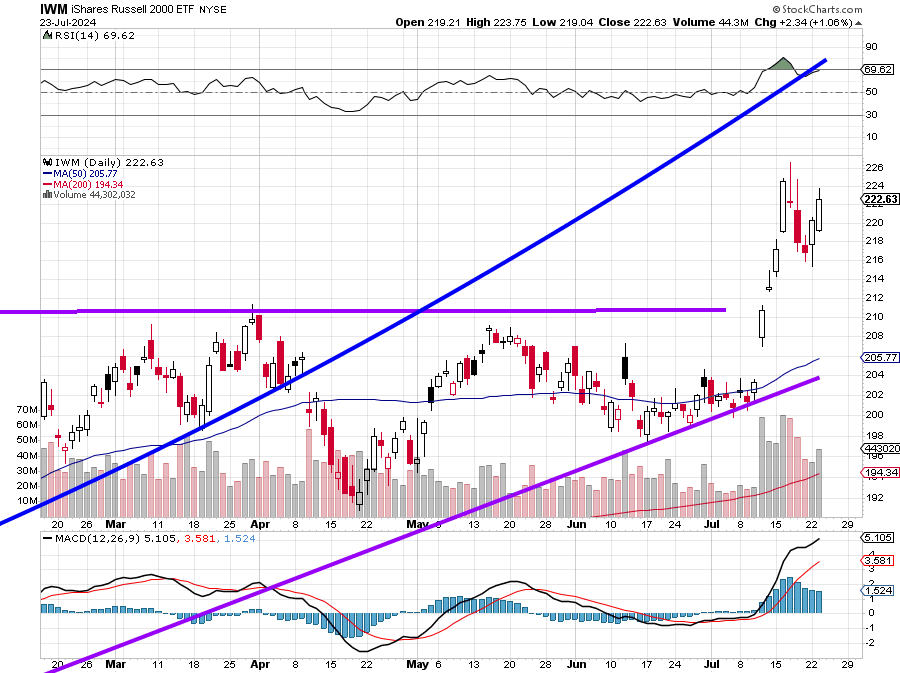

The Rotation in Pictures

The Invesco QQQ (Nasdaq 100) Trust QQQ remains a swing traders' game, maintaining contact with its 21-day exponetial moving average (EMA), as Relative Strength hangs on to a neutral reading and the daily Moving Average Convergence Divergence (MACD) sends an increasingly bearish message.

While the iShares Russell 2000 ETF IWM feels around for support at its former line of resistance, check out the strength in the RSI reading and the overly bullish look of the daily MACD:

To put that former line of resistance, now potential support, in perspective, take a look at this:

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.87%.

07:00 - MBA Mortgage Applications (Weekly): Last 3.9% w/w.

08:30 - Goods Trade Balance (June-adv): Last $-100.62B.

08:30 - Wholesale Inventories Income (June-adv): Expecting 0.5% m/m, Last 0.6% m/m.

09:45 - S&P Global Manufacturing PMI (July-Flash): Expecting 51.5, Last 51.6.

09:45 - S&P Global Services PMI (July-Flash): Expecting 54.8, Last 55.3.

10:00 - New Home Sales (June): Expecting 641K, Last 619K SAAR.

10:30 - Oil Inventories (Weekly): Last -4.87M.

10:30 - Gasoline Stocks (Weekly): Last +3.328M.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: TMO (5.12), ROP (4.46), GD (3.28), T (0.57), IP (0.41)

After the Close: NOW (2.82), KLAC (6.15), WM (1.83), F (0.68), IBM (2.17), CMG (0.32), URI (10.55)

At the time of publication, Guilfoyle was long GD and NOW equity; long TSLA puts; and long GOOG puts.