Something Big Is Happening in Treasuries — And It Can't Be Ignored

The wagers are enormous, and if these traders are right, the result would be disastrous to the economy, markets, and portfolios.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

If something wild happens in the coming months, we can’t say there weren’t signs.

The Commitments of Traders Report (COT) released last Friday by the Commodity Futures Trading Commission (CFTC) portrays an unfathomably significant net short position in the 10-year note Treasury futures contract held by large speculators and leveraged funds. Not only is it the largest bearish position ever held by these categories of market participants, but it also dwarfs most previous instances.

The last interest rate-cutting campaign was highly unusual in that the pandemic shutdowns accelerated it, but it is worth comparing position sizing to the current cycle.

The Fed began cutting rates in mid-2019, but the 10-year note futures bottomed out in October 2018, several months before the rate cuts were employed. At the 2018 10-year note low, large speculators held a net short position of about 680,000 contracts, a record extreme. As of last week, this group of traders was net short over one million contracts! Similarly, drilling further into the data, leveraged funds were net short a little over one million contracts in 2018, and they now hold double the number of short positions.

In summary, speculators are aggressively fighting the Fed and are outright insulting them with blatant expectations of higher yields. Perhaps their position is motivated by expectations of another wave of inflation, or it might be a lack of confidence in the Treasury’s ability to pay its obligations due to ballooning debt, or maybe a little of both. Either way, the wagers are enormous, and the eventual market volatility that comes with the unwinding of the trade could be stunning. Of course, if these traders are right about what comes next, the result (wildly higher interest rates) will be catastrophic to the economy, markets, and portfolios.

We Must Know Where We've Been to Guess Where We're Going

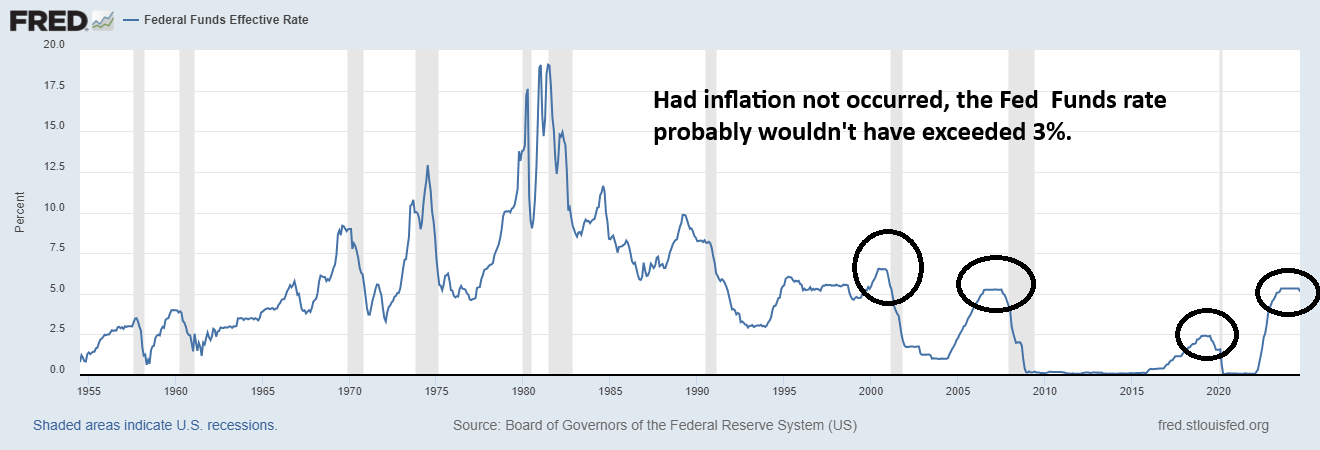

We can’t see the future, but we can review the past. Since entering the era of the 2000s, the Federal Funds rate (overnight borrowing rate set by our central bank) has spent most of its time below 1%. Despite attempts made by the central bank to “normalize” interest rates, things have gotten in the way (the financial crisis and the pandemic).

We don’t know if there will be another game-changing event, but even if there isn’t, we know that even the 2001 rate-cutting cycle (exacerbated by September 11, 2001) landed interest rates near 2% for about four years.

Thus, while short-term interest rates were dramatically higher in the 1970s and 1980s, we live in a completely different world: one in which inflation is combatted by domestic oil production, more efficient farms and ranches, and one in which central bankers feel obligated to adhere to a low interest rate environment to avoid natural economic bust cycles.

We don’t know what series of events will lead us there, but the odds are the Fed Funds rate will make its way sharply lower, just as it has done for the last 20+ years. Without historically rampant inflation in 2022 and 2023, the Federal Funds rate probably wouldn’t have exceeded 3%.

The last rate hike cycle (2019) topped nearly 2.5%, quickly falling back to zero. In 2000, rates peaked at 6.5% before being lowered to 1% and the 2007 peak was near 5%, followed by rate cuts to a target rate of zero. Will this time be different? We might not see zero, but 1% to 2% is highly likely. If this is the case, traders short the 10-year note could be in for a significant surprise.

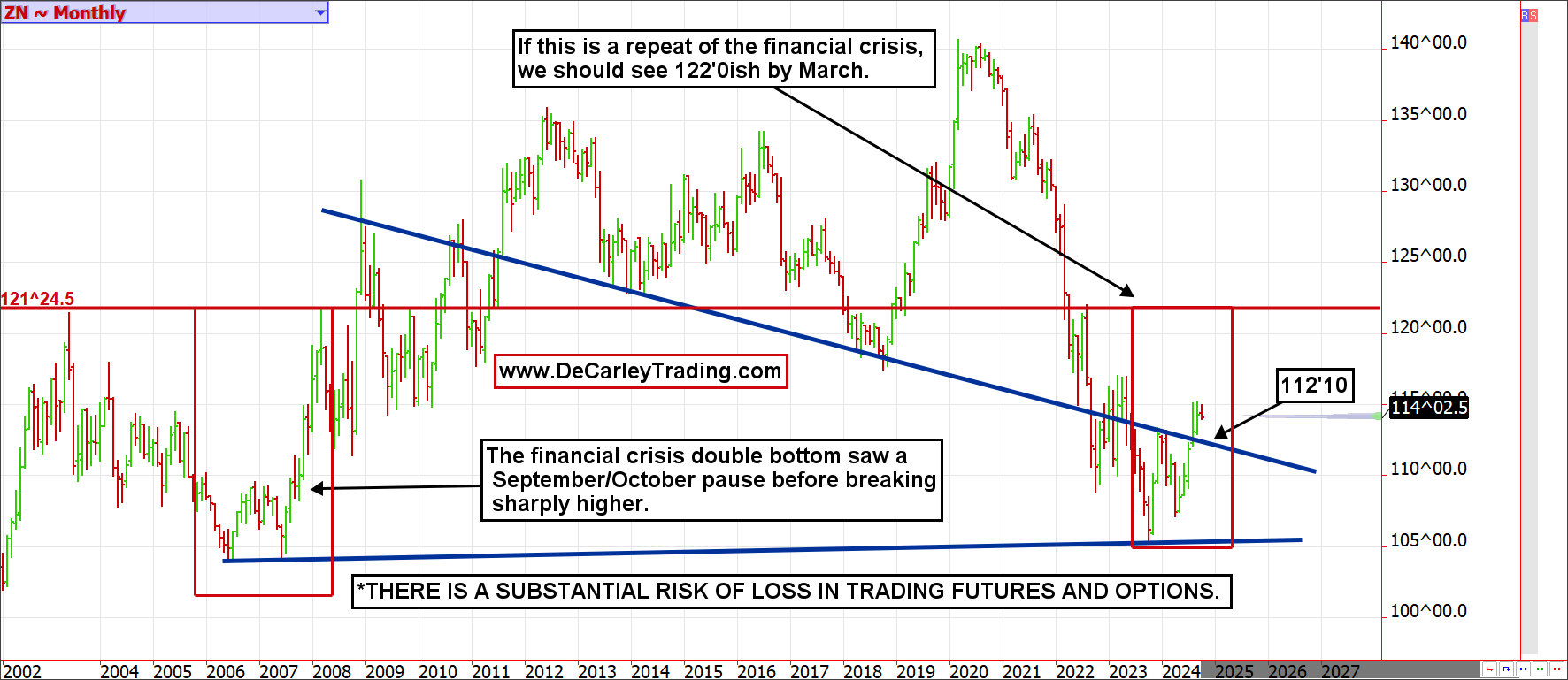

Lastly, we have pointed out the similarities between the financial crisis and today’s circumstances. The 10-year note (as opposed to the Fed Funds rate) appears to behave much like it did in 2007. We are coming off a double bottom near 105’0 and are seeing a September/October pause in the rally. If this is a repeat, the rally should eventually resume toward 122’0 or 2.25% to 2.50% for yield followers.

If you are looking for an entry point, a natural place would be about 112’10 in the December futures contract; this is where a 20(ish) year pivot line comes into play.

Bottom Line

Market participants are aggressively positioned against the Federal Reserve on the short side of the 10-year note. Either they know something we don’t, or they risk being victimized by a short squeeze. We are leaning toward the latter, but two-way volatility should be expected.