We Should Have Bought the Dip, but the Bounce Was Too Fast and Too Far

After a "surprise" 50 BPS cut by the Fed, we're projecting higher rates.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The Fed finally cut rates last Wednesday and two-year yields finished the week higher. But ten-year yields didn’t have the decency to rally on Fed day, and according to the Bloomberg WIRP function, the market is pricing in 2.92% by the end of the September 2025 meeting (instead of the 2.84% it had on Monday).

So, while the cycle is “new” in terms of actually cutting, with a “surprise” 50 BPS, it is difficult to argue that the bond market hasn’t already been pricing this in, perhaps too aggressively!

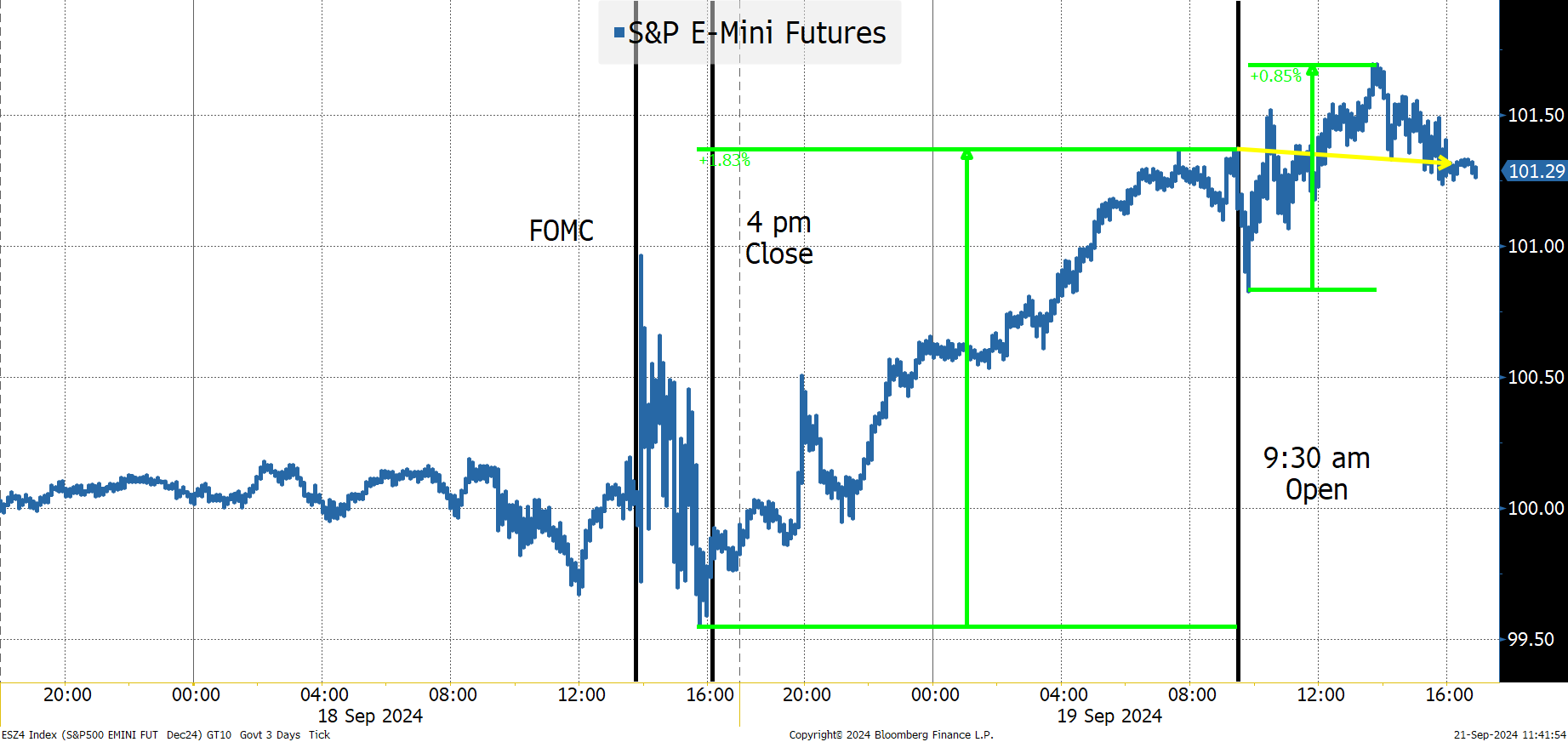

Stocks were more interesting last week, as they rallied, faded, rallied and then faded on Fed day. We then had one of the “crazier” Thursday’s I’ve seen in a while, but on Friday, it seemed like we were back to some buying fatigue, though we did have one decent rally off the lows (though it wasn’t even 1%).

Not only did all of the gains on Thursday occur before the open, but also, Friday had little volatility and finished lower, making the market precarious, at least from a technical standpoint.

Following Up on Our FOMC Analysis

We sent a lot of information out on the day of the Fed's cut announcement, where we had our top-two probabilities as being a “neutral 50 basis-point cut” followed by a “hawkish 50 basis-point cut.”

We actually felt that the Fed would try for the hawkish 50 (I think they did), but the market would interpret it as a neutral 50 (because, as much as you jawbone, you did actually just cut 50). Our conclusion was that it was somewhere between a neutral and hawkish 50 BPS cut, leaving us with two choices on market reaction from our earlier report:

- Neutral 50. Some initial wavering in stocks and bonds, but then “rally mode.” We got the “initial wavering” but seemed to hit rally mode way faster than expected.

- Hawkish 50. Stocks and bonds sell off, maybe for a day or two, then we can start watching the data and earnings. While we were on edge for a hawkish 50, we certainly didn’t get two days of selling.

Based on our own pre-FOMC thinking, with a 50 BPS cut, we should have been looking to buy the dip. We did not, as the bounce came faster and further than anything we expected (especially after Wednesday’s price action seemed to confirm our view that the market was already positioned too bullishly).

The fact that the rally on Thursday didn’t continue to scream higher is a minor miracle given that we seemed to miss our own takeaways, and Friday’s weakness encourages me to believe that we have yet see the post-FOMC lows.

So, what I think happened:

- On very low overnight volume, shorts got squeezed out. Traders who didn’t like the market’s initial response and shorted or kept shorts that were stopped out. Anyone hoping for a yen rally to help stocks got stopped out.

- The fact that the yen didn’t rally gave a sigh of relief for some traders who were worried about the possibility of a stronger yen and more unwinding of the alleged yen carry trade (I think that fear is heavily overstated).

- Retail (presumably across the globe) which associates Fed cuts with lower yields (though this isn’t always the case, especially out the curve) and in turn sees that as a sign to buy (despite the fact that, historically, it has often not worked out well), also helped push the buying (which probably explains the initial post-opening rally) to the highs of the day.

- Then, as the day went on, many longs decided to take profits, rather than trying to ramp things higher into the close (which surprised me as that has been a reasonably consistent trend).

- Liquidity is abysmal in both directions. The moves to the downside still tend to be more severe, but there is little true depth of liquidity in this market, largely due to market structure.

Bottom Line

I project moderately higher rates from two years on out as we price in a slower Fed, a smaller Fed and an end point that is higher and takes longer to reach. Look for the 10-year get back to at least 3.9% with far more risk of moving 50 BPS higher than 50 BPS lower from here.

On equities, let’s watch the great AI debate, the election, earnings and the economy. While I’m nervous, the price action since late Thursday morning gives me confidence that we have an opportunity to buy this market cheaper, and remaining small is important when volatility is so high. Adding to disruption, commercial real estate and small caps/value make sense, but again, I think we have to build smaller positions.

On credit, I’m comfortable with credit as I think the risk in equities is far more about valuation on a small subset of stocks, rather than economic and earnings risk. Add back to muni closed-end funds on weakness (and increased discounts to NAV), as I don’t think the tax situation is likely to get better in the coming years.

At the time of publication, Tchir had no positions in any securities mentioned.