Semiconductor Smackdown, Trading the Wreckage, Charting the Nasdaq, S&P 500

Two presidents tag-teamed the semis. As Biden held the semis' arms behind them, Trump came out of the corner with a flying elbow smash. Here's how I played it.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

And the only only only way you find it

Is if you're not digging too deep

Though it's easier said than done

You've got to feel it in your blood

Play the game like you've already won

And you only only only own it when you say

Easy Come Easy Go

This won't break my heart don't you know

Sometimes high, sometimes low

Easy Come Easy Go

- "Easy Come Easy Go" Charles "Kip" Winger (Winger), 1990

Smackdown

You kids see that? The pressure. The selling pressure. Sort of broad-based, but not quite. They just kept hitting bids. Across tech. Across the semis.

Traders tried to put together a rally about a half hour after the opening. Sold! Traders tried again early in the afternoon. Sold! The crowd gave it one last shot about 15 minutes ahead of the closing bell. Sold!

There was no letting up. Once the algorithms had made up their mind, it was "make sales" on any little pop, rather than "buy the dip." No. Some traders did try to buy those dips. Unless they were adding for a longer-term investment, that strategy was not working for the short-term, "go home flat" crowd.

We all know what happened. The two U.S. presidents tag-teamed the semis on Wednesday. As President Biden held the semis' arms behind them, fromer President Trump came out of the corner with a flying elbow smash. What really happened was that Bloomberg News had reported that the Biden administration was considering strengthening current export restrictions on chip companies to include non-U.S. companies making use of any U.S. technologies at all. That put Dutch firm ASML Holding ASML directly in the crosshairs.

Bloomberg News also published an interview with former president and current Republican nominee Donald Trump, where the potential next U.S. president stated that "Taiwan should pay us for defense." This put Taiwan Semiconductor TSM, by far the world's largest semiconductor foundry, on the backfoot, along with U.S. chip designers that lean on Taiwan Semi for that firm's foundry services. That was all she wrote for the semis on Wednesday, gang.

For the day, the Nasdaq 100 took a beating of 2.94%, the Technology sector SPDR ETF XLK gave up 3.89%, and the Philadelphia Semiconductor Index surrendered a stunning 6.81% on the session.

The five worst-performers in the Nasdaq 100 were semiconductor designers or semiconductor equipment providers. ASML Holding, Applied Materials AMAT, Advanced Micro Devices AMD, Marvell Technology MRVL and Lam Research LRCX all lost at least 10% during Wednesday's regular trading hours. Conversely, GlobalFoundries GFS and Intel INTC, both U.S.-based foundries, directly in competition with Taiwan Semi, managed to finish the day in the green.

Trading the Wreckage

What did I do during this semiconductor-focused meltdown? I exited a smallish, long position in Micron Technology MU and reduced my core long in Nvidia NVDA early in the session and redeployed that capital to AMD when I erroneously thought that maybe that name had bottomed for the day. Towards the end of the trading session, I picked up NVDA $118 calls expiring this Friday (tomorrow) just in case this morning's earnings release by Taiwan Semiconductor gave the industry group at least a temporary lift.

On that matter, TSM posted earnings per ADR and revenue beats while that top line print was good for year-over-year growth of 32.8%. The EPADR (as opposed to EPS) print showed profit growth of 36%. Robust demand for AI-capable chips was evident as 3nm chips accounted for 15% of shipments, up sequentially from 9% for the first quarter and chips labeled as high-performance accounted for 52% of shipments, up from 46% for Q1 and from 44% for Q2 2023.

It's very early, but TSM is trading 3.2% at last glance. That's with hours to go until U.S. markets reopen.

Marketplace

Of all the equity indexes I follow, only two closed the day higher: the Dow Industrials, on the strength of Johnson & Johnson JNJ and UnitedHealth Group UNH, and the KBW Bank Index. Everything else among the majors to mid-majors closed down on the day.

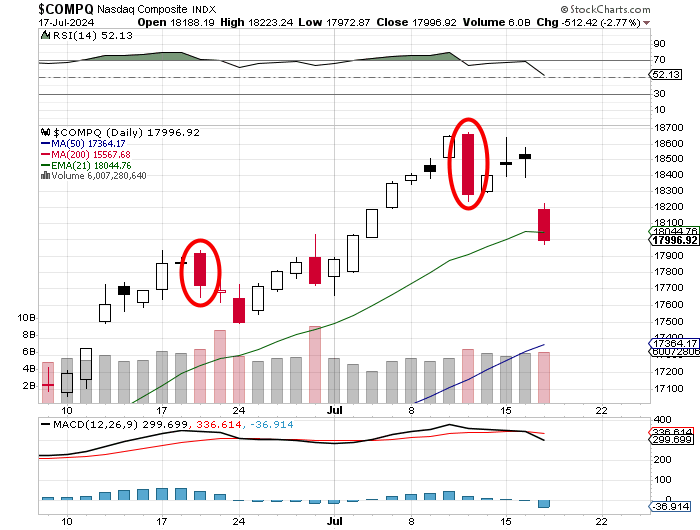

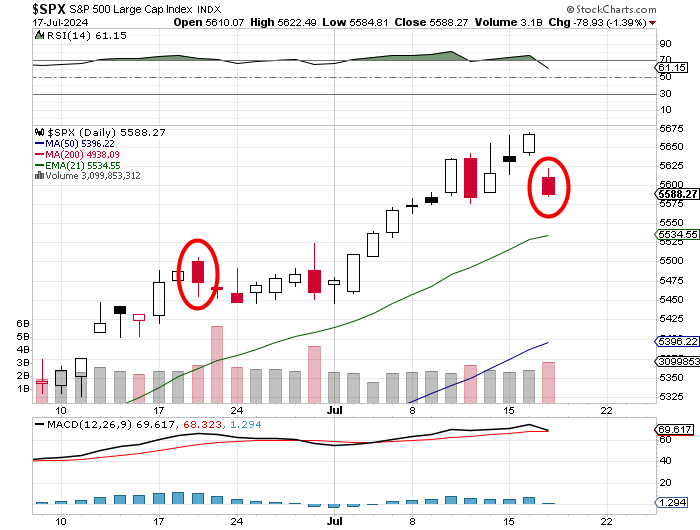

The Nasdaq Composite gave back 2.77%, posting its worst single day since September of 2022, while the S&P 500 lost 1.39%. Smaller stocks outperformed again, but still got hurt. The Russell 2000 gave up 1.06%, while the S&P 600 lost just 0.52%. The Dow Transports were tagged for a beating of 1.39%.

Somewhat incredibly, six of the S&P sector SPDR ETFs managed to close the day in the green, led by the Staples XLP and Energy XLE. Those two funds scored gains of 1.29% and an even 1%, respectively. I already told you that Technology gave up 3.89% for the day. Discretionaries XLY, Communication Services XLC and the Industrials XLI all also surrendered at least 1.27%.

As far as breadth is concerned, losers beat winners by about 7 to 5 at the NYSE and by rough;y 5 to 3 at the Nasdaq. Advancing volume took a 41.1% share of composite NYSE-listed trade and just a 34.7% share of composite Nasdaq-listed volume.

Trading volume in the aggregate, did increase, albeit just slightly, on a day-over-day basis across both NYSE and Nasdaq listings as well as across the memberships of both the S&P 500 and Nasdaq Composite. What this generally means is that professional money did in fact move out of equities on Wednesday.

So, was Wednesday a "day one" of a bearish change in trend? Take a look at this:

That "day one" actually happened last Thursday. According to the Nasdaq Composite, Wednesday was a "day two" confirmation separated by a few days from day one. It's a textbook example. However, the S&P 500 does not necessarily agree:

The S&P 500 traded higher than last Thursday's high for three successive days, negating that day as a valid "day one." That makes yesterday a potential "day one" and not a confirmation.

Readers should also be aware that we got "day ones" for both of these indexes in June that appeared to be confirmed by volume but were not as there was no break between the "day ones" and confirmation, hence that all became one move and the attempt to turn trend at that time failed.

Suddenly...

The macro started to look a little better. On Wednesday, June Housing Starts, while still fairly awful, especially in single-family unit starts, managed to beat expectations as June Industrial Production tacked a 0.6% month-over-month gain on top of May's 0.9% increase. This is the strongest two-month run for this series since late 2021. Capacity Utilization spiked as well to 78.8% from 78.3% a month ago.

The Atlanta Fed revised their GDPNow real-time Q2 model to growth of 2.7% (q/q, SAAR) from 2.5%. Atlanta entered this week at second-quarter growth of 1.5%. Really, I can't wait to see what the St. Louis and New York Feds do with these numbers over the weekend, as both of those models have been more accurate than Atlanta's in 2024.

The Beige Book

The Fed released its Beige Book on Wednesday, a couple of weeks ahead of their next FOMC policy meeting. In a nutshell, the report reads as...

On Labor Markets: "Demand for labor continued to ease, as most Districts reported flat to modest increases in overall employment."

On Inflation: "Price increases largely moderated across Districts, though prices remained elevated."

Overall Economic Activity: On balance, economic activity slowed since the previous report, with four Districts reporting modest growth, two indicating conditions were flat to slightly down, and six noting slight declines in activity."

Anyone Else Notice...

That Joel Anderson, the CEO that left Five Below FIVE as that firm warned for the quarter, ended the day as Petco's WOOF new hire for that same position? He starts on July 29. Wow. He said he was leaving to pursue other interests. That was quick. We thought that maybe he was fired. Maybe not.

This story certainly caused a double-take for me on Wednesday evening going over corporate headlines.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 235K, Last 222K.

08:30 - Continuing Claims (Weekly): Last 1.852M.

08:30 - Philadelphia Fed Manufacturing Index (July): Expecting -2.8, Last 1.3.

10:00 - CB Leading Indicators (June): Expecting -0.3% m/m, Last -0.5% m/m.

16:00 - Net Long-Term TIC Flows (May): Last $123.1B.

The Fed (All Times Eastern)

13:45 - Speaker: Dallas Fed Pres. Lorie Logan.

18:05 - Speaker: San Francisco Fed Pres. Mary Daly.

19:45 - Speaker: Reserve Board Gov. Michelle Bowman.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: ABT (1.11), ALK (2.37), CTAS (3.79), DPZ (3.63), KEY (0.24), MTB (3.51), TXT (1.48)

After the Close: ISRG (1.54), NFLX (4.77), PPG (2.48)

At the time of publication, Guilfoyle was long KEY, AMD and NVDA equity; and long NVDA calls.