Scott Bessent, Milton Friedman, and Modern Monetary Theory

How will markets react to the new Treasury Secretary?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

You may have noticed a major change in interest rate expectations over the past several months. Not long ago, analysts and economists were anticipating multiple 50 basis point reductions in the Fed funds rate.

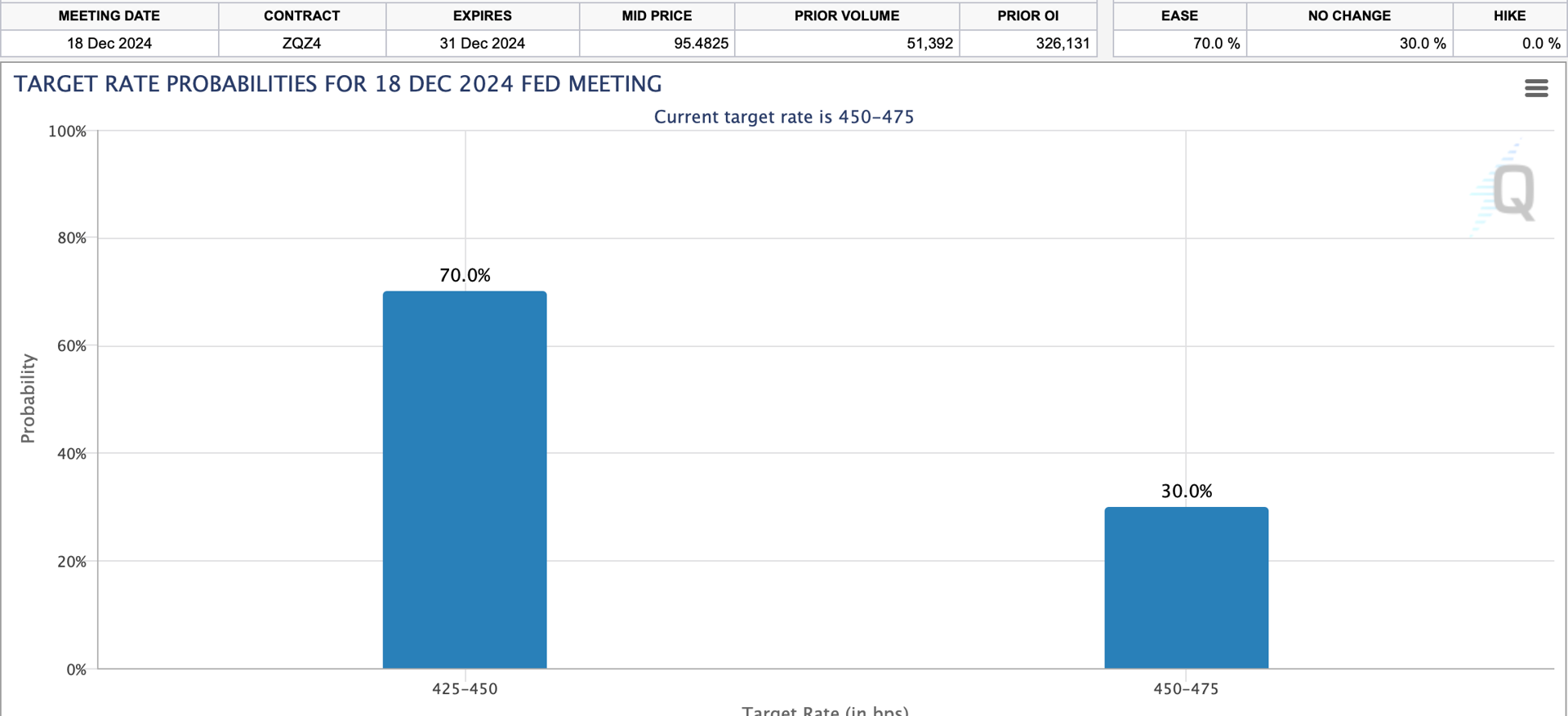

Now, there is some question as to whether the upcoming Fed decision will include even a 25 basis point rate cut. According to the CME FedWatch Tool, there is now a 30% chance that the FOMC will hold rates steady at its December 18 meeting.

What led to this change in expectations? Growth continues to be solid, as evidenced by Wednesday's GDP report. The U.S. economy is growing at a steady 2.8%, according to preliminary data for the fourth quarter.

Meanwhile, inflation remains elevated above the Fed’s 2% target rate. In October, the consumer price index ticked up to a 2.6% annual rate, from 2.4% in September. With the economy growing steadily, and with inflation still a concern, it makes sense to moderate expectations for rate cuts.

Fed Chair Jerome Powell is likely to remain at the central bank's helm until his current term expires in May of 2026. Two weeks ago, Powell stated he was "in no hurry" to cut rates.

While Powell remains a constant, the Treasury Department will soon have a new leader. Scott Bessent has been tapped to replace current Treasury Secretary and former Fed Chair Janet Yellen.

Bessent could replace Powell as Fed Chair in 2026. How could his influence affect monetary policy? Bessent, a hedge fund veteran, is a former partner at Soros Fund Management and the founder of Key Square Group.

How will markets react to Bissent in 2025 and beyond? The answer might be found in his approach to dealing with inflation.

Some of Bessent’s comments reveal an old school, Milton Friedman-esque attitude toward inflation. You may recall economist Friedman‘s famous quote, “Inflation is always and everywhere a monetary phenomenon.”

Compare this to Bessent’s quote from a recent appearance on WABC’s Larry Kudlow radio show, “Inflation comes through either increasing the money supply or increasing government spending.”

Bessent’s policies could mark a major change from the current deficit spending approach. An accumulation of massive debt suggests that governments can print and spend money at will without suffering major repercussions. This is in direct opposition to many of Friedman’s tenets.

Friedman believed that increasing the money supply and raising government spending would result in inflation. It’s a small sample size, but based on the past few years, he may have been on to something.

If Friedman was correct, inflation could be tamed by reducing the money supply and by cutting government spending. In other words, not necessarily via changes in interest rates.

It’s a logical theory, but what would be the ramifications if put into practice?

While a reduction in spending and in the supply of dollars theoretically could reduce the rate of inflation, it might also lower the value of some investment portfolios. If Friedman’s theory is correct, the same increase in money supply that drove grocery prices higher also drove stock, crypto, and real estate prices higher.

If the supply of U.S. dollars was to be reduced, the value of each remaining dollar would theoretically increase. This in turn would put pressure on commodity prices. Items which are valued in U.S. dollars, such as crude oil and gold, would likely fall in price.

If the dollar gains strength, import prices would likely decline. A strong dollar would create favorable exchange rates, both for trade and travel.

Theoretically, a reduction in the supply of dollars could tap the brakes on rallies in stocks and real estate, as it might become tougher to generate inflows.

Cash would be king. How long has it been since anyone’s uttered that phrase?

If any of this actually happens, it’s likely to happen slowly. There is no need to make changes now.

However, investors should pay attention to this situation as it evolves. It might make sense to increase cash allocations if these policies are put into place.