Producer Prices Pop, so Pay Attention

Let's see why these numbers are important, what they mean for the chances of a rate cut, and why someone always has to pay. Also, let's the chart of the Nasdaq and check on BlackRock's crypto position.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Some say that prices at the producer/wholesale level are a leading indicator. Some don't really look at them all that much. I am in the former camp. For if producer prices move higher, it makes sense that at least some of those higher prices would be passed on to the consumer. Either that, or profit margins get squeezed. There is no "good" outcome when producer prices rise, unless of course, you are the Federal government and happen to be keeping the whole operation afloat through exponentially increasing deficit spending. How long can that go on? It feels like forever that we have been asking that question, probably because we have.

Now, with the U.S. federal government off to the worst two-month start to any fiscal year in its long 248-year history, we must again go there. Just two months into fiscal 2025 (The federal fiscal year runs October through September), the U.S. government is already $624.3 billion in the hole. Federal debt stands at 123.4% of GDP. As recently as the year 2000, that ratio stood at 55%. Forty years ago, that ratio was in the mid-30% area. It happened rather quickly. One irresponsible presidential administration after another. One reckless, mindless congress after another. Now the Federal Reserve Bank is put in the awkward position

Where the U.S. likely is at this point is referred to as "fiscal dominance", which is where the government's fiscal needs unintentionally, or maybe intentionally, strip the central bank of its independence. The result is a forced fiscal reliance upon monetary policy to keep borrowing costs in check in order to help manage the federal debt-load and federal debt service expenditures, often at the expense of price stability.

Producer Prices Pop

On Thursday morning, after Wednesday had produced a November consumer price report that confirmed at least a two-month acceleration of consumer-level prices (with a third month certainly on the way), the Bureau of Labor Statistics released its November PPI report. November PPI was indeed hot, hotter than November CPI had been.

On a month-over-month basis, headline November PPI printed at growth of 0.4%, up from 0.2% in October, while core PPI actually slowed to growth of 0.2% from October's 0.3% print. The headline month-over-month print equaled the highest month pace of growth for the series since April. Incredibly, within the report, prices for eggs were up a stunning 54% month over month. That's incredible. Food as a category was up 3.1% for the month.

Now for the year-over-year data, which is arguably more important. For November, headline PPI was up a very surprising 3%, which was up from October's 2.6% print, which was above September's 2.0% print. That was a super-fast gain of 100-basis points on the index. That should rattle some cages. Core PPI crossed the tape at a second consecutive month of 3.4% annual growth after hitting a low of 2.6% this past summer.

So, some cages were rattled. The U.S. Dollar Index ran higher, taking on and topping the 107 level for the first time in a couple of weeks. The yield for the U.S. Ten Year Note gave up five basis points for the day, rising to 4.33%, as yield for the Two-Year Note gave back four basis points to go out at 4.2%.

Does That Jeopardize Next Week's Rate Cut?

No. Though Fed Funds Futures are now pricing in a 96% probability for a quarter-percentage point rate cut at next week's Federal Open Market Committee policy meeting and that is down from 98% the day prior, this cut is all but certain. That said, it stands to reason that the rate cuts that follow, as in the one currently priced in for March, could be delayed, or even not ever happen.

See the above reference to "fiscal dominance." I think we all know that the Fed is even considering rate cuts with inflation obviously moving in the wrong direction due to the fact that the federal government needs to be accommodated. The federal government needs lower borrowing costs and needs inflation to actually go the wrong way, regardless of what is said. There are not too many paths out of a fiscal mess and gradually debasing the currency while jawboning about fighting inflation is the least obvious way.

With labor markets now showing some overt signs of weakness, the medium-term future would be highly uncertain. That does, however, provide for the central bank the cover it needs to publicly pursue one of its dual mandates, as one must almost always be sacrificed to meet the needs of the other. Couple this week's rise in first time jobless claims and continuing jobless claims with two consecutive months of significant job losses according to the BLS Household Survey and you do have a deteriorating labor market. No matter what they tell you on financial TV.

Equities

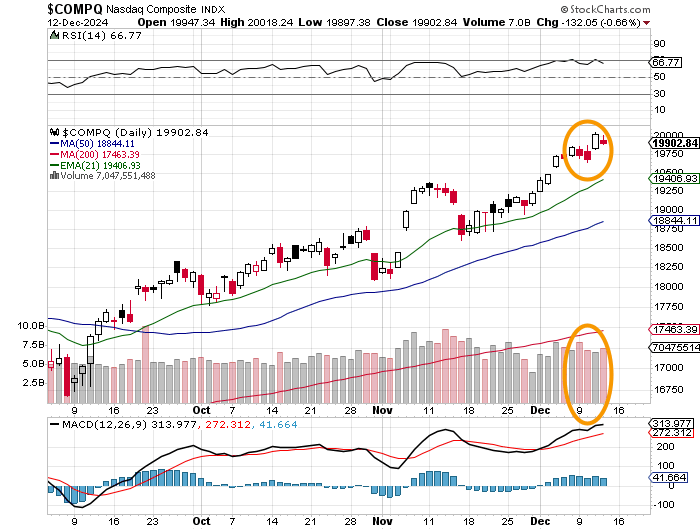

The hot PPI print put some pressure on stocks on Thursday, though futures are trading higher on Friday morning at least partially due to positive earnings releases late Thursday by both Broadcom AVGO and Costco COST. The tape during the regular session though, was painted a pale shade of red. The S&P 500 gave back 0.54%, as the Nasdaq Composite surrendered 0.66%.

Readers will see that despite the red candle day, the Nasdaq Composite still closed higher than it did prior Wednesday's rally and also that this index experienced an "inside day" which usually signals a coming period of reduced volatility,

Small caps underperformed broader markets. The Russell 2000 took a 1.38% hit, as industry specific indices stepped backwards as well. The Philadelphia Semiconductors surrendered 0.91%, as the KBW Banks gave up 0.51% and as the Dow Transports (the day's winner) dropped just 0.02%.

Nine of the 11 S&P sector exchange-traded funds shaded into the red on Thursday, but not one single fund among the 11 moved even 1% away from where it went out on Wednesday. The day's loser was the Consumer Discretionaries XLY at -0.83%. The discretionaries had been Wednesday's upside leader. The day's winners were the Staples XLP, but that group gained just 0.29%.

Breadth was rather ugly again on Thursday. Losers beat winners by almost 3 to 1 at the NYSE and by a rough 5 to 2 at the Nasdaq. Advancing volume took just a 25.5% share of composite NYSE-listed trade, but NYSE-listed trade in the aggregate dropped significantly from Wednesday's level. Aggregate Nasdaq-listed trading volume did end considerably higher on Thursday than it did on Wednesday, but advancing volume managed to take a 48.8% share there, so not really a lot of conviction for the session.

How About BlackRock?

I'm sure readers on Thursday noticed that BlackRock BLK, which is the planet's largest asset manager, had decided publicly that cryptocurrency does deserve a place in a multi-asset portfolio. The firm's Investment Institute released a paper on Thursday, suggesting that for Bitcoin a 1% to 2% weighting would produce a similar share of profile risk as would the Mag 7 growth stocks in a standard 60/40 portfolio. Hmm.

Enjoy The Game

On Saturday afternoon, Army and Navy will square off on the gridiron for the 125th time. This year both teams come in strong, Army at 11-1 and Navy at 8-3. Both teams are headed to post-season bowl games. Growing up, this game was the Super Bowl in my house and still is.

I was a West Point season ticket holder for about half of my life and outside of the Covid year and years where my own service prevented it, I have made it to at least one game a year most years since 1969. I also served at the base briefly. Yes, I was a Marine, but I was also a soldier. In football, in this game, or really in college sports, I root for Army.

No, none of us went to the schools, but all of us had served or would serve. I played college ice hockey, but my alma mater no longer has a team, so I tend to identify athletically with kids who also left home at 17 to serve their country. I don't know about you, but for me, for my father, and for my sons, the intensity of this game, as fans, is unmatched anywhere else in sports. Enjoy.

Economics (All Times Eastern)

08:30 -Export Prices (Nov): Expecting -0.3% m/m, Last 0.8% m/m.

08:30 - Import Prices (Nov): Expecting -0.2% m/m, Last 0.3% m/m.

13:00 - Baker Hughes Total Rig Count (Weekly): Last 589.

13:00 - Baker Hughes Oil Rig Count (Weekly): Last 482.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle had no positions in any security mentioned.