Nasdaq 100 Passes Technical Test; Semis’ Tough Week; Iran Spat Calms?

Let’s dive into the charts and why they point to a possible a.m. tech rally; look down at ON Semiconductor, Arm Holdings and Qualcomm; and check the latest on Iran.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Adapt. Overcome. That’s what you and I have, above all other abilities. If you’re in these markets and you have managed to survive on your own for a bit without having to go find a salary and benefits somewhere, then you have shown the ability to understand, identify, adapt and overcome. This is one job that is certainly not for everyone. U.S. equity markets are coming off of a tough week. The S&P 500 and Nasdaq Composite both posted their respective second losing week in the past four. In fact, both of those induced put five losing sessions out of five, to the tape last week.

The interesting thing that readers will see, as they make their way through this article, is that while the S&P 500 was tested, technically, last week, and the Nasdaq Composite looked possibly to have broken, the perhaps more important Nasdaq 100 was not only tested, but appeared to have passed that test, setting up a Monday morning rally. It is important to understand as well, that while Friday’s trading volumes were exceedingly high, because that elevated pace of activity was largely due the mechanics of index reconstitution, the results of the day’s price discovery process bears far less technical significance than it would have otherwise.

In fact, breadth was quite positive on Friday despite the negative-looking performance of these markets at the large-cap headline level. Readers must keep in mind that last week, crude oil prices moved sharply lower, at least until Iran’s beleaguered military started shooting at everyone again, forcing a U.S. response. Readers must also keep in mind that yields paid by Treasury debt securities moved lower as well last week. These two forces are distinctly bullish forces that would normally push ask asset prices higher.

That said, with hostilities flaring and with a fierce rotation out of what had worked this year (AI, high-tech, memory / storage) a large number of market participants may not have noticed that a decent-sized swath of our marketplace survived last week quite well. Small caps, mid-caps, the banks, the transports and of course, defensive-types all out-performed the growth stocks that many trader-investors, yours truly had become over-exposed to.

Last Week

See those semis? Yikes. For the week, ON Semiconductor (ON) gave up 25.5% after announcing a proposed deal to acquire Synaptics (SYNA). ON was followed to the downside for the week by Arm Holdings (ARM), Western Digital (WDC) and Qualcomm (QCOM). Those three names gave back 23.9%, 21.4% and 16.2% respectively.

The macro was strong last week as core personal consumption expenditure inflation for May landed on consensus view, but personal income and personal spending for the month both exceeded expectations. Additionally, Q1 gross domestic product was revised substantially higher, from growth of 1.6% (q/q, SAAR) to growth of 2.1%. While I was able to poke some holes in that revised GDP print last week, that’s not what keyword-reading algorithms see.

Those algos see increased economic activity, which in their simplified logic, results in inflation, and therefore decreases any chance at a short-term rate cut at any point in the short- to medium-term future. Not that I think there is a good case for a rate cut in the short-term, I don’t see the logic for a hike either; I just do not think that the revision to Q1 GDP was any reason for a market reaction.

Of course, by week’s end, Iran’s Islamic Revolutionary Guard Corps had broken the truce, yet again, and started shooting at civilian cargo ships, yet again, as well as at its neighbors, yet again. That temper tantrum, which that caused almost no damage, yet again, and was met by a U.S. military response and by the end of the weekend, Iranian leadership wanted to talk about peace, yet again.

Lo and Behold…

Equity index futures markets are indicating early gains on Monday morning as it appears that Washington and Tehran had agreed to halt military strikes in that region. Technology stocks, which were pummeled last week, look ready to lead this potential rally. The U.S. and Iran, according to the Wall Street Journal, have agreed to end days of semi-contained combat in and around the Strait of Hormuz and resume peace talks. This most recent exchange of hostilities had marked the most serious breaches of the existing “ceasefire” for lack of a better word, since both sides signed the famous or infamous “memorandum of understanding” on June 17.

Oh, This…

Toward the end of the week, Pres. Donald Trump threatened to impose a 100% tariff on goods imported into the U.S. from any country having placed a digital services tax on U.S.-based tech companies. The president posted to social media, “This TARIFF will supersede Trade Deals made with the Country, whether implemented, signed, or not.”

We already know that the president’s “reciprocal” tariffs were struck down by the Supreme Court. Hence, these tariffs, if attempted, could not be considered “reciprocal” and another statute would have to be found.

Not Like We Didn’t Warn Readers…

Oracle (ORCL) shares gave up 19.4% last week. In doing so, ORCL gave back at least 2.58% every single day last week. That was, for ORCL, the worst one week performance since the burst of the “Dot-Com” bubble back in August of 2001. That’s 25 years. That’s pre-9/11. That’s a long time ago.

I have repeatedly warned readers to steer clear of long positions in this name, as I have for quite a while now pointed toward significant cash burns, an absolutely horrific-looking debt load and a balance sheet that does not show the kind of deferred revenue that one might expect with the kind of

remaining performance obligation that the firm boars of.

It looks like at least some folks on Wall Street are actually doing the fundamental analysis (which has become a lost art) on this name and the stock has behaved accordingly. On Friday, ORCL closed down 57% from its September 2025 high, but perhaps more alarmingly, closed down 40.7% from its recent June 1st intraday high. That day, investors rejected what had been a three-day rally.

Week Ahead

Yet another holiday week lies to our direct front. The week will be quiet in some ways. Light on earnings. Light Fed schedule. Still, there are some heavyweight-level events set for the next few days so we can’t try to coast through this period. We’re going to have to rev it up and play the darned game.

- The Geopolitical: Are we at war again or not? After exchanging fire all weekend, the U.S. and Iran apparently started talking about peace again on Sunday. Hence the higher open for equity index futures last night. Then there are the threats of tariffs against the E.U. Literally, anything could happen this week in the realm of the geopolitical that could disrupt our market week in one way or the other.

- Macro: Depending on what we see coming out of peace talks between the U.S. and Iran, the macroeconomic schedule should take center stage this week. This is June Jobs Week. The Bureau of Labor Statistics will release the results of its two employment situation surveys for the month on Thursday. This will come after the ADP Employment Report covering the private sector, for June, hits the tape on Wednesday morning. Nearly as important will be the ISM Manufacturing survey results that will also cross the tape on Wednesday morning.

- The Federal Reserve: It’s a holiday week. Usually that means we won’t hear anything from the Fed. But a new sheriff in town. The rest of the crew may or may not be looking for ways to avoid putting in any extra work, but Fed Chair Kevin Warsh will speak from the ECB Forum on Central Banking this Wednesday morning.

- Earnings: Second-quarter earnings season will not begin in earnest for another two weeks or so. This week, a holiday week, is literally void of any headline-level names that might have filled out the earnings calendar. There are a few names that readers have heard of that will release their quarterly results, but nothing that gets trades fired up. This afternoon, we’ll hear from AeroVironment (AVAV). That will be followed up by Constellation Brands (STZ) and Nike (NKE) on Tuesday afternoon. FactSet (FDS) and General Mills (GIS) will report on Wednesday morning and that’s close to all we’ve got, gang.

- Events: Honeywell Aerospace (HONA) will trade regular-way this morning, after being spun off by parent Honeywell International (HON). Honeywell Aerospace has already been added to the S&P 500, replacing Conagra Brands (CAG).

The Week That Was…

The S&P 500 posted a second losing week in four last week, suffering five straight “red candle” sessions, as did the Nasdaq Composite. This is how it went:

- The S&P 500 lost 0.05% on Friday and 1.95% for the week.

- The Nasdaq Composite gave up 0.24% on Friday and a nasty 4.6% for the week.

- The Nasdaq 100 surrendered 1.09% on Friday and 4.24% for the week.

- The Russell 2000 gained 0.07% on Friday and 1.02% on the week.

- The S&P Small Cap 600 tacked on 0.94% on Friday and 3.05% for the week.

- The S&P Midcap 400 lost 0.16% on Friday but gained 0.65% for the week.

- The Dow Transports lost 0.49% on Friday but gained 0.87% for the week.

- The Philly Semis were pummeled for 5.29% on Friday and for 7.94% for the week.

- The KBW Bank Index was beaten for 1.21% on Friday but gained 1.48% for the week.

On Friday, seven of the 11 S&P sector SPDR exchange-traded funds closed out the session in the green. The defensive sectors out-performed and health care (XLV) led the defensives. Technology finished out the day in a very distant last place. Interestingly, winners beat losers at both of New York’ equity exchanges on Friday and advancing volume beat declining volume for names listed at both of those exchanges.

For the week, as well, seven of the eleven S&P sector SPDR ETFs finished in the green. The story was much the same. Defensives led and were led by health care and the REITs (XLRE). Growth suffered as technology and communication Services under-performed.

The Chart

Though the price action visible on the charts for the day of a Russell Rebalancing can often be taken with a grain of salt much like the action on a ‘triple-witching” expirations event, something disturbing did happen on Friday.

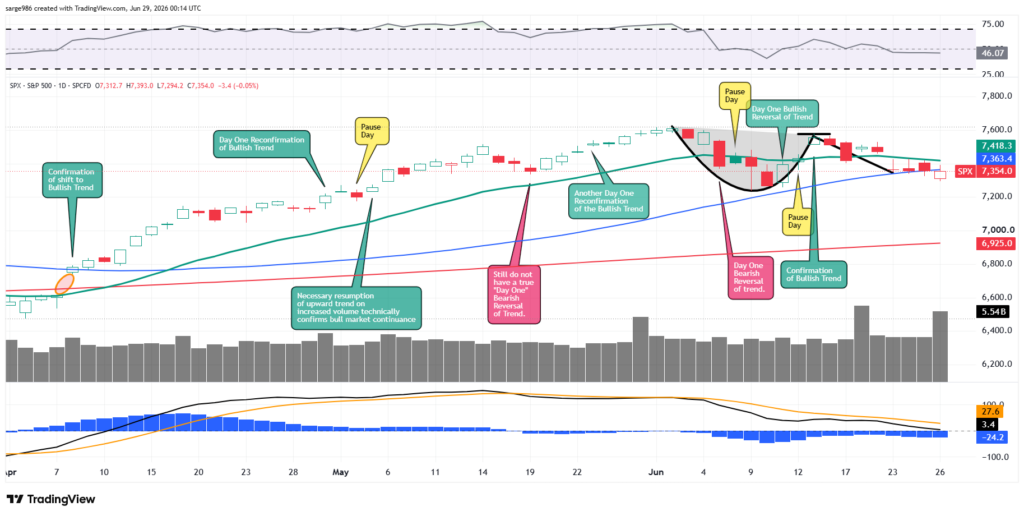

Readers will see that the S&P lost its 50-day simple moving average on Friday and closed below that line. It is key for readers to remember what I have told you in the past: Key technical lines are not lost when they are pierced. They are lost when contact is lost. Contact was not lost on Friday. Hence, the index has today to regain that line and not sustain real technical damage.

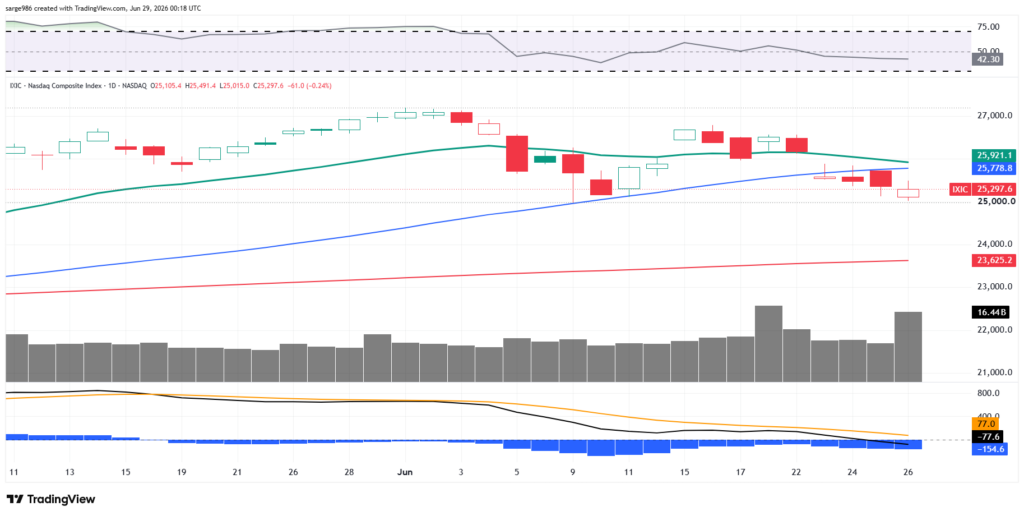

Readers will also see that the Nasdaq Composite lost that line on Thursday and lost contact on Friday. Does the Nasdaq have a problem? Maybe, but check this out:

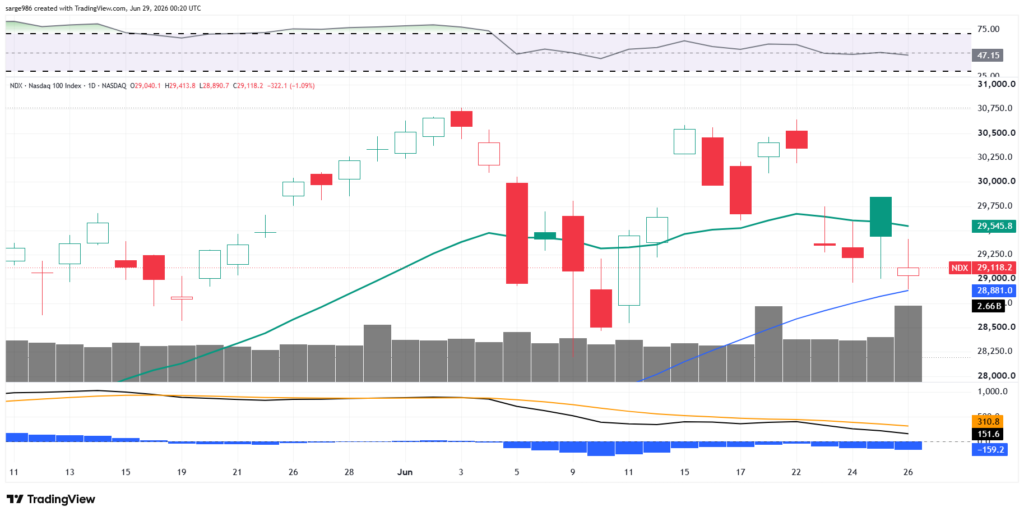

The tech-heavy Nasdaq 100, even with all of the troubles experienced by Tech, AI and the Mag 7 over recent days, still has not lost its 50-day SMA. In fact, the Nasdaq 100 found support there on Friday. True story.

Earnings

As of June 26, according to FactSet, for the second quarter, Wall Street now expects to see year-over-year earnings growth for the S&P 500 of 23.1%, up from 22% last week. Wall Street also sees revenue growth of 12.3%, up from 12.1% one week ago. For the second quarter, 48 S&P 500 companies have issued negative earnings guidance while 63 have issued positive guidance.

For the full year of 2026, the street now looks for earnings growth of 24%, up from 23.3% last week, and up from 14.7% more than two months ago. This would come on revenue growth of 11.2%, up from 11.1% last week and up from 7.7% a rough ten-plus weeks ago. The outlook for the third quarter is also very positive. Third quarter S&P 500 earnings growth is now estimated at 26.7%,year over year.

At the moment, the Energy and Technology sectors are projected to have grown Q2 earnings an absolutely jaw-dropping 123.2% and 63.2% respectively. Just one sector, Health Care (at -9%) is currently projected to have suffered a Q2 earnings contraction.

Valuation

Still using data provided by FactSet, the S&P 500 ended last week trading at 20.1-times 12 months’ forward-looking earnings, flat over two weeks’ time and down from 21.6 times about 10 weeks ago. This is still well above the five-year average of 19.9 times for the index as well as being well above its ten-year average of 19 times.

The S&P 500 also ended last week trading at 27.3 times trailing 12 months’ earnings, down from 27.4 times just one week ago, and also above levels that the index reached more than two months back. This also stands well above the five-year (24.5 times) and 10-year (23.4 times) averages for the index.

Eight of the 11 sectors are now trading at or above their five-year average valuations, led by the Industrials (25.0 times). Three sectors closed out last week undervalued relative to or even with their five-year norms, down from four sectors over the past two weeks.

Fed Funds Futures

Fed Funds futures trading in Chicago are currently pricing in a 70% probability for no change to be made to the current target range (3.5% to 3.75) for the Fed Funds Rate at the culmination of the next FOMC policy meeting on July 29. There is no chance for a rate cut being priced in as there is a 30% likelihood for a raise being accounted for.

There are no rate cuts fully priced in at any point in the future looking out towards year’s end 2027. That said, there is now a rate hike priced in for September of this year (60% probability). There is nothing else priced in at this point going out a year and half beyond that potential hike.

The Final Frontier

Late Friday, Nasdaq announced that after the close of business on July 6th, ahead of the July 7th open, SpaceX (SPCX) will, under the recently adopted “fast-track” framework, to the prestigious Nasdaq 100 index. Despite the fact that SPCX will start out with a relatively small weighting (under 1%), this is a big deal. This action triggers billions of mandated purchases of the stock as passive investment vehicles replicating or tracking the index will be forced to buy the shares. Under the old rules, SpaceX would not have qualified for inclusion in the Nasdaq 100, which is composed of the 100 largest non-financial firms listed at that exchange.

Economics (All Times Eastern)

10:30 – Dallas Fed Manufacturing Index (June): Expecting 2, Last 0.4.

The Fed (All Times Eastern)

No public appearances scheduled.

Today’s Earnings Highlights (Consensus EPS Expectations)

After the Close: AVAV (1.47)

At the time of publication, Guilfoyle was long WDC equity.