Markets at the Midpoint, Russell Rebalance, Debate Thoughts, Week Ahead

Let's take a look at where equity markets stand exactly six months into the year, including the effects of the weak Japanese yen, steepening yields, macro data and more.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Happy Monday. For baseball fans, especially fans of the New York Mets, Happy Bobby Bonilla Day. For my Canadian readers, Happy Canada Day, or if you are my age, Dominion Day!

I don't know about most of you, but I felt my age by last Friday afternoon. For the week, the major indexes sandwiched three "up" days with two "down" sessions, which left equities quite mixed for the week in aggregate.

Interestingly, despite what at the end of the week was perceived as encouraging news on inflation, Treasury debt securities sold off even as the U.S. dollar Index continued its ascent. Perhaps this has more to do with the weakening Japanese yen. Japanese economic performance and Japanese monetary policy than it does domestic economic performance and domestic policy.

After all, Japanese accounts in the aggregate comprise the largest foreign holdings of U.S. sovereign debt by a significant margin. While that may drive flight out of the yen and into dollars, there could also be a need by Japanese investors in need of capital to take "carry" profits. In addition, should the Bank of Japan continue to intervene in currency markets in order to bolster their home currency, just how do you think they'll go about that? Separately, the euro is stronger this morning on the back of the French parliamentary elections. This has the U.S. dollar Index trading lower as we work through the zero-dark hours leaving the relationship between the greenback and the yen nearly unchanged.

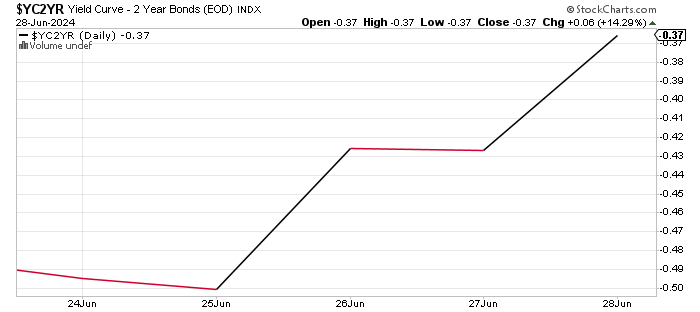

Over the course of the week past, the yield for the U.S.-10-Year Note popped for an upward move of 10 basis points, while the yield for the 2-Year Note only gained three basis points. By week's end, U.S. 2-Year paper paid 4.75%, while the 10-Year paid 4.39%. This worked towards "steepening" (If that's what you still call it when it's this inverted) the yield curve a bit:

That's a fairly aggressive move in the 10 yr / 2 yr spread over just five days. This morning, I saw the curve steepening just a wee bit more as well.

The main event, of course, for the second week in a row, was the expected surge in trading activity on Friday. This past Friday, just to remind those who enjoy their weekends, was the day of the Russell Index Reconstitution, which came a week after our June "triple witching" expirations event. The end of June Russell Reconstitution, also known as the "Russell Rebalancing" is always projected to be the busiest trading day of the year.

This past Friday did disappoint just a bit on that end. While aggregate trade across both NYSE and Nasdaq listings was indeed up roughly 100% and 66%, respectively, on a day-over-day basis, the day was not quite top dog as far as volume is concerned for 2024. Oh, Friday did in fact beat the Friday prior. That said, this past Friday was not as busy as the "triple witching" expiration of March 15 was across the membership of the S&P 500.

The Macro

Before we even got to the much-ballyhooed May PCE numbers that were released Friday morning, we had to get through the Richmond Fed Manufacturing Index, June Consumer Confidence, May New Home Sales and May Durable Goods Orders, all of which were less than impressive. Within that Durable Goods Orders report, the most important item, core capital goods orders, which excludes air and defense purchases, printed at disastrous "growth" of -0.6%. This key measure of economic health, which is seen as a proxy for business investment, has now printed in a state of monthly contraction for eight of the past 12 months.

Then there was Thursday's final revision to Q1 GDP. The Bureau of Economic Analysis revised their estimate for Q1 GDP to growth of 1.4% (q/q, SAAR). Remember that Final Q1 GDI printed at growth of 1.3% (q/q, SAAR), which legitimized the GDP print as the two ran side by side.

It is key to understand that GDP (gross domestic product) and GDI (gross domestic income) are both measures of national output, and that both measure the same economic activity from a different perspective. In theory, they should produce the same result as one is intended to be a check upon the other. You and I both know that's not what happened in 2023, when GDP for the year printed at growth of 2.5% and GDI for the year hit the tape at growth of 0.4%. At least one of them was not just incorrect, but very incorrect.

Lastly, headline May PCE inflation printed flat month over month and at growth of 2.6% year over year. Both of these prints were right on consensus view and down from April. Core PCE hit the tape at growth of 0.1% m./m and growth of 2.6% y/y. Again, these numbers were right on the money as far as expectations were concerned and again, down from April. The surprise came in the other data provided in this report that showed less consumer spending than projected.

GDP Modeling

By week's end, after the disappointing Durable Goods Orders report, and the disappointment in personal spending, the Atlanta Fed was forced to revise their GDPNow real-time model for the second quarter to growth of 2.2% (q/q, SAAR) from 3.0%. The other three Fed districts that do model GDP in something like real time, only revise their models on weekends.

Brace yourself as Atlanta has persistently been the upside outlier among the four and so far, this year, St. Louis has been the most accurate. Across those other three Q2 GDP models, the New York Fed sees the second quarter growing 1.93%, the St. Louis Fed is at +0.76%, and the Cleveland Fed is at +0.69%.

Equity Marketplace

It's now time to take a look at where equity markets stand, exactly six months into the year as above and beyond the Russell Rebalance, Friday brought with it the final day of trade for the month, quarter and half.

- The S&P 500 gave up 0.08% last week to close the first half up 14.48%.

- The Equal-Weight S&P 500 gave up 0.42% last week to close the first half up 4.07%.

- The Nasdaq Composite gained 0.24% last week to close the first half up 18.13%.

- The Nasdaq 100 gave up 0.09% last week to close the first half up 16.98%.

- The Russell 2000 gained 1.27% last week to close the first half up 1.02%.

- The S&P Small Cap 600 gained 1.14% last week to close the first half down 1.61%.

- The S&P Mid Cap 400 gave up 0.06% last week to close the first half up 5.34%.

- The Dow Transports gained 2% last week to close the first half down 0.74%.

- The Philly Semiconductor Index gave up 1.2% last week to close the first half up 31.06%.

- The KBW Bank Index gained 2.53% last week to close the first half up 8.83%.

Last week, four of the 11 S&P sector SPDR ETFs gained ground over the five-day period, while seven of those funds closed the week in the red. Year to date, over half of a year, 10 of the 11 S&P sector SPDRs are in the green, led by Communication Services XLC and Technology XLK. Those two funds are up a respective 18.52% and 17.94% year to date followed by Energy XLE and Financials XLF. Only the REITs XLRE are in the red (-2.49%) at the half-way mark.

Do I Mention the Debate?

I am not sure that this impacts economics in the short-term or markets in real-time, but I do think as an American that what we saw last Thursday night was terrifying. I think we would have had to have been fools to think that President Joe Biden was still close to the top of his game, but now we know beyond the shadow of doubt that he is suffering from some kind of serious age-related deterioration.

Everyone gets old at a different pace. There are no cheap shots being taken here, in this column. We do have to ask, though, how long has the president been this bad, and we do have to ask just how far and how deep the attempt to cover up this reality goes.

I understand completely a cabinet and legislative leaders hiding a president's incapacity from our adversaries. That's common sense. However, to run him out there for re-election when they had to know there was a very good chance that he would be on the losing side of perhaps the most lopsided presidential debate in my lifetime is very close to inexcusable. We have an article 25 for a reason. We elect vice presidents for a reason. I am no fan of either political party, so while I am a very fiscally conservative thinker, I see both of these presumed nominees as highly irresponsible in a fiscal sense.

I try to be apolitical and as objective as possible. I take no joy in seeing any American president humiliated on the national and global stages like that. Now, we have five months, and it's probably more than that, maybe much more than that... where we know someone unelected is probably making the important decisions. Not good at all.

The Week Ahead

This is yet another holiday week. It seems like holidays have been constant of late. You see, while salaried employees love federal holidays, grinders don't like them at all. Grinders are folks like traders, contractors and salespersons who work on commission. In short, folks don't eat if they don't work.

There's an old saying on Wall Street... "Short weeks are always long." What it means is that the pressure is on when there are fewer days available to make a living. The average earnings required per day to clothe and feed the family increase while often the liquidity or trading volume decreases. This is a combination that makes for a period of heightened risk. A risk that at times eats that trader from the inside while he or she never ever lets their family see them sweat. Rock on. That said, Thursday is Independence Day. Financial markets will be closed. Ahead of the holiday, equity markets will close three hours early on Wednesday.

Corporate... There is going to be one quiet week. I did not see any conferences or events out there this week that merited a mention. As far as earnings are concerned, the calendar is very, very light this week. On Tuesday morning, we'll hear from MSC Industrial Direct MSM, and on Wednesday morning, Constellation Brands STZ reports.

The Fed... This crew is for the most part taking the week off, at least from making public appearances. Chair Powell will speak on Tuesday morning, while New York Fed Pres. John Williams speaks on both Wednesday and Friday. Additionally, the Minutes of the FOMC policy meeting that culminated on June 12 will be released on Wednesday afternoon, after the closing bell.

Macro... The headline event for the week will be this Friday's release of the Establishment and Household Employment Surveys for June by the Bureau of Labor Statistics. My expectations are for non-farm payroll growth of a seasonally adjusted 183K jobs, an unemployment rate of 4%, a participation rate of 62.6% and an underemployment rate of 7.5%. I also expect to see a serious slowing of year-over-year wage growth.

Lastly... You kids see the Boeing BA news? According to reports, it looks like the Justice Department will charge Boeing with fraud and the aerospace giant will have until the end of the week to decide whether or not to plead guilty or risk going to trial. Oh and Boeing has agreed to acquire Spirit AeroSystems SPR.

Economics (All Times Eastern)

09:45 - S&P Global Manufacturing PMI (Jun-F): Flashed 51.7.

10:00 - ISM Manufacturing Index (Jun): Expecting 49.1, Last 48.7.

10:00 - Construction Spending (May): Expecting 0.2% m/m, Last -0.1% m/m.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle had no positions in any securities mentioned.