Market Chutes and Ladders, Fed Adjustments and Tapering, Macro Madness

The byproduct of this policy shift is higher for longer, not just for rates, but for the monetary base, for money supply, for the slosh that has permitted increased valuation metrics for risk assets.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I remember enjoying the simple children's game Chutes and Ladders when I was very young. Never thought I'd have to play that game professionally as an adult. Such is life.

Such is the reality of a market structure whose creators thought it wise to replace crowds of traders wearing colored jackets working towards price discovery in a centralized location while pricing shares of stock in Spanish pieces of eight. Or maybe those creators simply worship at the altar of unearned profit just like everyone else.

I mean how can profit be earned when it has nothing to do with analysis, or actual price discovery, and everything to do with creating momentum. Yes, creating momentum through the use of high-speed, keyword-reading algorithms that have the ability in a hollowed-out marketplace (as in no human book of bids and offers) to lead the overwhelming weight of passive, non-cogent, order flow around by the nose.

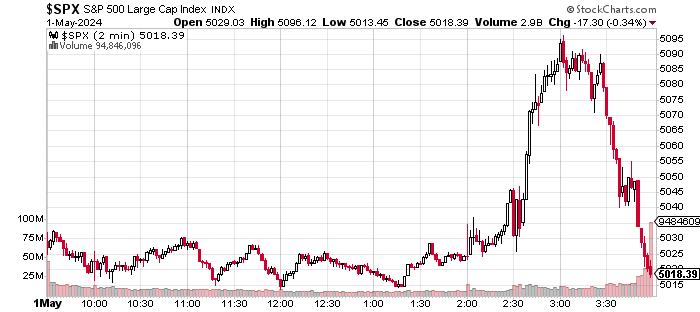

That said, this is what the S&P 500 looked like on Wednesday, minute by minute:

Round and Round

What comes around goes around

I'll tell you why

Yeah

- Pearcy, De Martini, Crosby (Ratt), 1984

The Fed

There certainly were some adjustments made by the central bank on Wednesday. Not very hard to figure out.

The FOMC had to acknowledge the lack of success in fighting inflation so far in 2024. This sentence was added to the official policy statement's first paragraph: "In recent months, there has been a lack of further progress toward the Committee's 2 percent inflation objective." Does acknowledgement mean that a rate hike is on the table? Not exactly. During the press conference, Fed Chair Jerome Powell said... "I think it's unlikely that the next policy rate move will be a hike." Nuff said on that topic. I guess.

Does acknowledgement even mean that rate cuts are off the table? Again, no. During the press conference, Powell also said..."It is likely to take longer for us to gain confidence that we are on a sustainable path down to 2 percent inflation, I don't know how long it will take."

Powell and his crew are trying to push out making any hard decisions until after the national election in early November. I get that. There is a need for the Fed to at least appear independent, and at a minimum, apolitical.

What this kind of posturing does is push out the status quo. "Higher for longer" will be the mantra for short-term interest rates. Powell believes that the current posture of U.S. monetary policy is restrictive. I believe quite the opposite, that policy is not currently restrictive, and the idea of increasing rates should have at least been hinted at on Wednesday.

Markets, aside from the money-making games played by the algo crew, seemed to like the extension of the status quo, which I think back me up. Treasuries rallied on Wednesday and while the major equity indexes were mixed, market internals and breadth were quite strong.

Then There Was This...

The Fed did surprise us, not out of left field, as we knew this was coming, but the timing and aggressiveness of the tapering plans for the quantitative tightening plans were also an upside impetus for stocks on Wednesday. I had expected that Powell would address an eventual tapering of the program during the call, but instead, the Committee went ahead and implemented a policy change to be effective as early as June.

The drawdown will, in June, move from $60B worth of Treasuries per month down to $25B worth of Treasuries per month. The drawdown in the Fed's holdings of mortgage-backed securities will hold steady at $35B worth per month. That had been expected to remain the same. The Fed will continue to reinvest principal payments in excess of those caps into the Treasury market. That's pretty dovish. The fact is that we have now had one regional bank fail in 2024, and the Fed is worried about denting bank reserves, which would become a reality if the QT program had been left in place as was.

To allow that program to proceed could have caused disruptions in overnight funding markets and created liquidity problems that the central bank would rather see avoided. The byproduct of this policy shift is higher for longer, not just for short-term rates, but for the monetary base, for money supply, for the slosh that has permitted increased valuation metrics for risk assets.

Marketplace

Treasury securities rallied on the QT tapering news. The U.S. 10-Year Note went out at a yield of 4.63%, down five basis points. The U.S. 2-Year Note ended Wednesday paying 4.97%, down 8 basis points. Early on Thursday morning, I have seen both of these yields move down a little further.

At the headline level, equity markets went nowhere fast on Wednesday afternoon, after following the algo crowd allowing the tail to wag the proverbial dog. The KBW Bank Index gained 0.67% for the session, as the Philadelphia Semiconductors were pounded for a loss of 3.54% as Skyworks Solutions SWKS and Advanced Micro Devices AMD gave up 15.3% and 8.9%, respectively following their earnings reports. Among the Dow Industrials, Dow Transports, S&P 500, S&P 400, S&P 600, Nasdaq Composite and Russell 2000, the largest gain for the day was 0.35%, while the largest loss was 0.34%.

On a sector level, the results were just as non-committal. Five S&P sector SPDR ETFs closed in the green, led by the Utilities XLU, as five closed in the red, led by Energy XLE. One sector SPDR, the Financials XLF, actually managed to close out the regular session unchanged. On a Fed policy decision day. That's incredible.

Breadth, however, was quite strong. Winners beat losers at both of New York's stock exchanges, by margins of roughly 3 to 2. Advancing volume took a 54.1% share of composite NYSE-listed trade and a 58.4% share of composite Nasdaq-listed trade. Aggregate trading volume increased on a day-over-day basis as well...across both NYSE and Nasdaq listings and across the membership of both the S&P 500 and Nasdaq Composite.

I think what this volume tells us is that, at least for now, professional money probably bought that algo-inspired late day selloff on Wednesday. Will the major indexes make another run at their respective 50-day simple moving averages (SMAs) after hitting resistance at that spot earlier this week? I would think that is likely.

The Madness

I am not sure how many readers made note of the BLS Business Employment Dynamics (BED) report for Q3 2023. The report was released a week ago, yes, by the Bureau of Labor Statistics and has largely been ignored by the financial media. What the BED report does is measure employment by quarter, with a great lag, so while a very good analytical tool, it is not so useful in real time. That is why traders and news people every month go with the BLS Non-Farm Payrolls number, which is part of the BLS Establishment Survey as a proxy for job creation.

Economists know that this "BED" report is far more accurate than the monthly Establishment Survey as the Establishment Survey is done in a hurry, polling just 670K employers and then extrapolating those results across the population so as to estimate a number deemed as likely. The BED report is done quarterly and gone over slowly after polling 9.1M employers. There is no doubt about which of these reports is more accurate. The quality of the work is not even close.

What was released last week was the BED report for Q3 2023 (that's the lag). For that quarter, the BED report shows net job losses in the United States of 192K. Those are losses, not job creation. The Non-Farm Payrolls reports for Q3 2023 total 640K, implying robust job creation that we now know was truly job destruction. That's an overstatement of 832K jobs. When we look at Q2 2023, we see that the monthly Non-Farm Payrolls reports overstated job creation by another 489K positions.

You guys do see where I'm going, right?

The Q4 2023 BED report is still months away, but the overstatement in job creation (that the media is still running with and is still being cited by politically biased economists) over the six months that make up Q2 and Q3 2023 comes to 1.321M positions. We already knew that there are fewer full-time positions in the U.S. than there were a year ago. This, however, does show a labor market that did start to fall apart in 2023.

Yes, of course, this means that the BLS will have to issue a huge revision to its job creation numbers later this year. This is bigger than that though. The year 2023 was painted as a year of economic growth, where those who called for a recession were openly scoffed at in the media. We may have come much closer to actually entering into economic contraction in mid-2023 than many folks think.

Just as obviously, the BEA will have to revise 2023 GDP lower at some point. Go back and look at Q2 and Q3 2023. For those quarters, GDP growth printed at 2.1% and 4.9% (q/q, SAAR) respectively. Remember what I've told you about GDI. It's supposed to equal GDP as the two measure the same economic activity. Q2 and Q3 GDI printed at growth of 0.5% and 1.9% (q/q, SAAR).

How interesting. That was the period we talked about at that time. I might have been the only kid on the block who bothered checking GDI against GDP in 2023. I wrote (over and over) that something was amiss. The financial media, many of whom read this column, were mostly afraid to speak up. Well, something actually was amiss, gang.

Economics (All Times Eastern)

08:30 - Balance of Trade (Mar): Last $-66.9B.

08:30 - Initial Jobless Claims (Weekly): Expecting 212K, Last 207K.

08:30 - Continuing Claims (Weekly): Last 1.781M.

08:30 - Non-Farm Productivity (Q1): Expecting 0.8% q/q, Last 3.2% q/q.

08:30 -Unit Labor Costs (Q1): Expecting 3.2% q/q, Last 0.4% q/q.

10:00 - Factory Orders (Mar): Expecting 1.6% m/m, Last 1.4% m/m.

10:30 - Natural Gas Inventories (Weekly): Last +92B cf.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: COP (2.08), CMI (4.96), HII (3.48), MRNA (-3.48), SO (0.90), W (-0.42)

After the Close: AMGN (3.91), AAPL (1.51), SQ (0.73), CTRA (0.41), X (0.93)

At the time of publication, Guilfoyle was long SO, CTRA and AMD equity.