Let's Give Them Something to Talk About

Time for a chat about the market chatter. Here's what I'm hearing (and not hearing), what's reflected in the sentiment stats, and how that could change with jobs report.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The chatter is getting more bearish but the sentiment statistics don’t really reflect it yet. Chatter-wise there is more talk of a recession and more talk of bad news being bad news. And of course there is the scary September seasonality chatter.

About the only chattering I haven’t yet heard is how we are supposed to sell before Rosh Hashanah and buy before Yom Kippur. Perhaps because Rosh Hashanah is still about a month away. It is rather late this year.

In fact as I listened to the parade of Fed watchers discussing whether the central bank is behind the curve or not, or whether they should cut 25 basis points or 50 basis points, it strikes me that no one is ever satisfied with the Fed. The same way folks will say the Jewish holidays are early or late in a given year, they are somehow never on time. Maybe it’s all just human nature to complain about such things.

But back to sentiment. The Investors Intelligence bulls didn’t change much this week. The American Association of Individual Investors (AAII) saw a small shift from bullishness as the bulls are no longer over 50% (they are now at 45%) but the bears did not rise, they fell two points (to 25%).

Everyone seems to have jumped into the neutral camp. Long-time readers will know that this is typical as folks rarely jump the fence from bull to bear but rather make a stop on the fence. Either way, there is nothing extreme there.

The National Association of Active Investment Managers (NAAIM) pulled back their exposure this week from the mid-80s to 71. That’s a start, but 71 is the middle of nowhere. Based on the chatter I would have expected that to be 55-60 already.

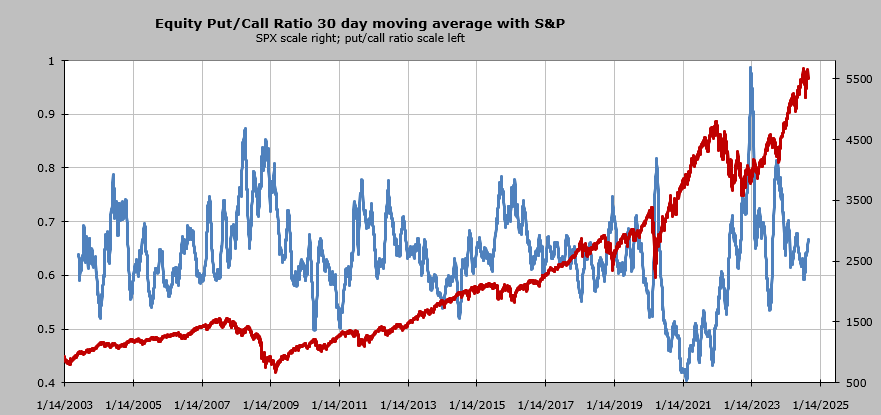

Even the put/call ratios are not showing any extreme fear. We still haven’t had a reading over 1.0. The total put/call ratio spent the entire day on Thursday in the 60s! In the end it closed at a more normalized 0.85.

As of this writing (and since the data doesn’t settle until much later Thursday night, please take this with a grain of salt, maybe even an entire shaker), it seems that there were a lot of calls on the VIX being bought, enough to keep the ratio down.

Yet, the equity put/call ratio was over 1.0 as the puts expanded greatly late in the day. That would be the first sign of some real caution coming into the market.

Speaking of the equity put/call ratio I thought we should check in on the 30-day moving average. About a month ago (late July) we saw this dip under 0.60, which I said was too low. It has edged its way up to 0.65, which is in the middle of nowhere but if we start getting readings like that (possible) reading over 1.0 this should move up quickly.

Perhaps the Employment number will give the market a lift or maybe it will finally get that gap on the S&P 500 at 5455 to fill. A bearish reaction on a Friday ought to see the put/call ratio rise.