Introducing TheStreet Pro's Wealth Advisor Letter

Welcome to our newest offering for wealth advisors and individuals who want to learn more about managing their money.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I am pleased to announce that we at TheStreet Pro are launching TheStreet Pro’s Wealth Advisor Letter, a newsletter for wealth managers. I’m Louis Llanes, a veteran wealth manager with over 30 years of experience advising high-net-worth individuals about investment strategy and overall wealth planning. I will be writing about managing traditional and alternative investments, holistic wealth planning strategies, business development, and more.

My goal is to be a resource for advisors who strive to improve their practice. If you are an individual investor who manages your own wealth, I invite you to tune in as well because many of the strategies you will read about can help you think about your personal situation. If you work with a financial advisor, this newsletter will offer insights and ideas you can discuss with your advisor. It is my goal to help you be a better-informed investor when talking to your advisors.

I look forward to interacting with you and invite your comments and feedback.

Louis Llanes, CFA, CMT

Opportunities Wealth Advisors Should Not Miss

Today, I'd like to share how process and personalization drive advisory success. We'll do this by discussing how advisors should navigate concentrated positions for stock, real-estate, and business owners.

These strategies are ones that I've used successfully since learning valuable lessons early in my career during the Dotcom bust.

It was September of 1999, and I was a young investment manager with only three years of experience. My training as a CFA was steeped in picking investments based on trying to calculate the intrinsic value of stocks and buying attractive businesses with a strong competitive advantage. Before this time, I felt like I had the markets whipped.

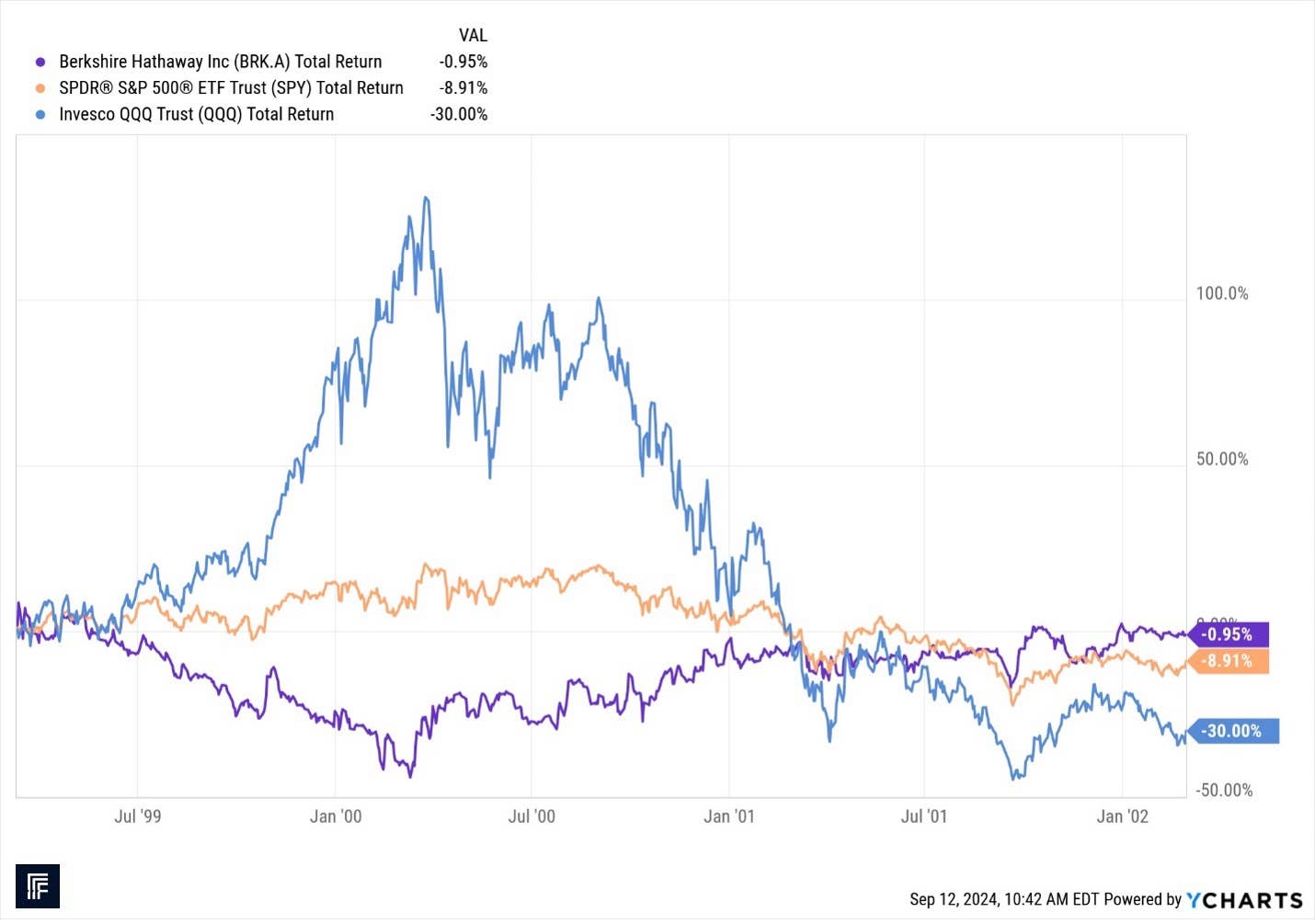

This valuation approach earned solid returns, but now our stocks were falling rapidly, and the market was rewarding dotcom stocks with no cash flow. The only metric that seemed to work was the number of “eyeballs” viewing their sites. I was baffled. As you can see in the chart below, the Nasdaq skyrocketed while value investor like Warren Buffett’s Berkshire Hathaway, were free falling. During this time, investors were selling shares of high-quality companies and going to speculative issues. This was my first lesson that selling is very important.

A painful truth came to light – selling based on valuation can leave you looking like an idiot in the market. Retail investors seemed to be better stock pickers than I was because they were chasing the hot dotcom stock of the day and doing better than our portfolio. It was humiliating! The urge to change strategies was intense. It took two years for this to reverse. But as the chart shows, when it did, these investors got hammered, and it took a decade to recover. Could we be in a similar situation today?

One of the biggest excuses we heard when trying to advise clients was that they did not want to generate a lot of taxes when selling their stocks and real estate. You hear the same thing today.

As a wealth manager, I see three huge opportunities to help these clients and to increase assets under management - and as usual, it deals with taxes.

Tax Solutions For Three Investment Situations

A surefire way for wealth advisors to attract new clients is to help them avoid writing a large check to the IRS. Tooling up to have the expertise to help them is one of the smartest things an advisor can do right now.

The first big opportunity is the executive with highly appreciated stock. It is common for executives to be sitting on big gains, and maybe to be in love with their company stock. They’ve received incentive stock options (ISOs), restricted stock units (RSUs), and other stock grants over the years, and now these positions are concentrated to a level that is unacceptable. They may not understand this. Don’t let them wait until it’s too late.

The second big opportunity are investors who have been investing in real estate for years and are getting closer to retirement. They want to lessen the burden of managing real estate properties or diversify their nest egg while making their portfolio more liquid and accessible. They need to improve the flexibility of their balance sheet without the use of debt and other complications.

The last big opportunity is the business owner who wants to retire, but will have complicated capital gains, income, and estate taxes upon the sale of the business. The proceeds from the business sale must be tax-efficient and reinvested to meet the client's and their family's long-term goals.

But there is one more thing every advisor must add to their toolkit to scale at a larger level-and it has nothing to do with finance!

Be Both an Economist and a Therapist

When I wrote my book “Financial Freedom Blueprint”, the editors wanted me to get quotes. I asked a lot of people I respected for quotes. My teenage daughter has watched me at work, talking to investors and colleagues. To my surprise, she had been listening to me and observing both my and my clients’ mood swings. She walked up to me and said, “Dad, I think you have to be both an economist and a therapist to do a good job in your field”. Boom! She was right so I put her quote in the book.

Lots of investors are emotionally attached to the investments that made them wealthy. I had a conversation the other day with a potential new client and friend who is a doctor. She said, “All you have to do is hold NVDA and Costco.” I know she didn’t really mean that, but I bet she felt it was true on some level.

So, the question is, how do you get an intelligent person like a doctor or technology executive to make better choices? It all starts with having and communicating a process.

Provide Value With a Tangible Process

New clients tend to gravitate toward advisors with clear processes that offer tangible benefits when executed well. The primary goal is to guide clients toward transparent, fact-based thinking while addressing their psychological biases toward concentrated investments. This can be challenging, as it's natural to feel emotionally attached to investments that have generated significant wealth. However, if you demonstrate a process that helps prospective clients find solutions to improve their tax situation while maintaining upside potential, they are more likely to be receptive to your message.

It reminded me of what Jeffrey Gitomer, a renowned sales coach and author of the bestselling book The Little Red Book of Selling, once told me, "My 30-year secret to marketing without ever placing an ad is to put myself in front of people who can say yes to me and deliver value first."

By providing value upfront, you engage people immediately. Because they see you can really help them, they are much more excited about sharing their detailed information with you. They are pulled toward you for advice.

Cookie Cutter Advice Means You Are a Commodity

Once a client is intrigued and you've gathered the details of their portfolio, it's not enough to simply apply a cookie-cutter asset allocation model and recommend buying or selling securities based on it. To make informed recommendations, you need to thoroughly research their largest holdings. The goal is to understand the drivers of returns, such as profitability, revenue growth, expenses, and any endogenous factors within the industry. Additionally, you must have a solid grasp of the financial stability of these investments. It’s all about understanding the true economics your client is facing and shining a light on it.

This knowledge is crucial because it allows you to determine two key factors: whether the investment is overpriced and which types of investments would be strong diversifiers to complement their concentrated positions. By doing so, you can select investments that reduce risk and provide additional upside potential.

Losses Accumulate Quickly While Gains Build Slowly

I've seen fortunes lost because an investor refused to pay enough in taxes. Why? Because they held onto a deteriorating investment and watched its value plummet. Losses accumulate quickly, while profits build slowly. Most investors will wait until it’s too late to sell. It is just a fact. Risk management is critical, especially with highly speculative investments, even if it results in significant tax payments.

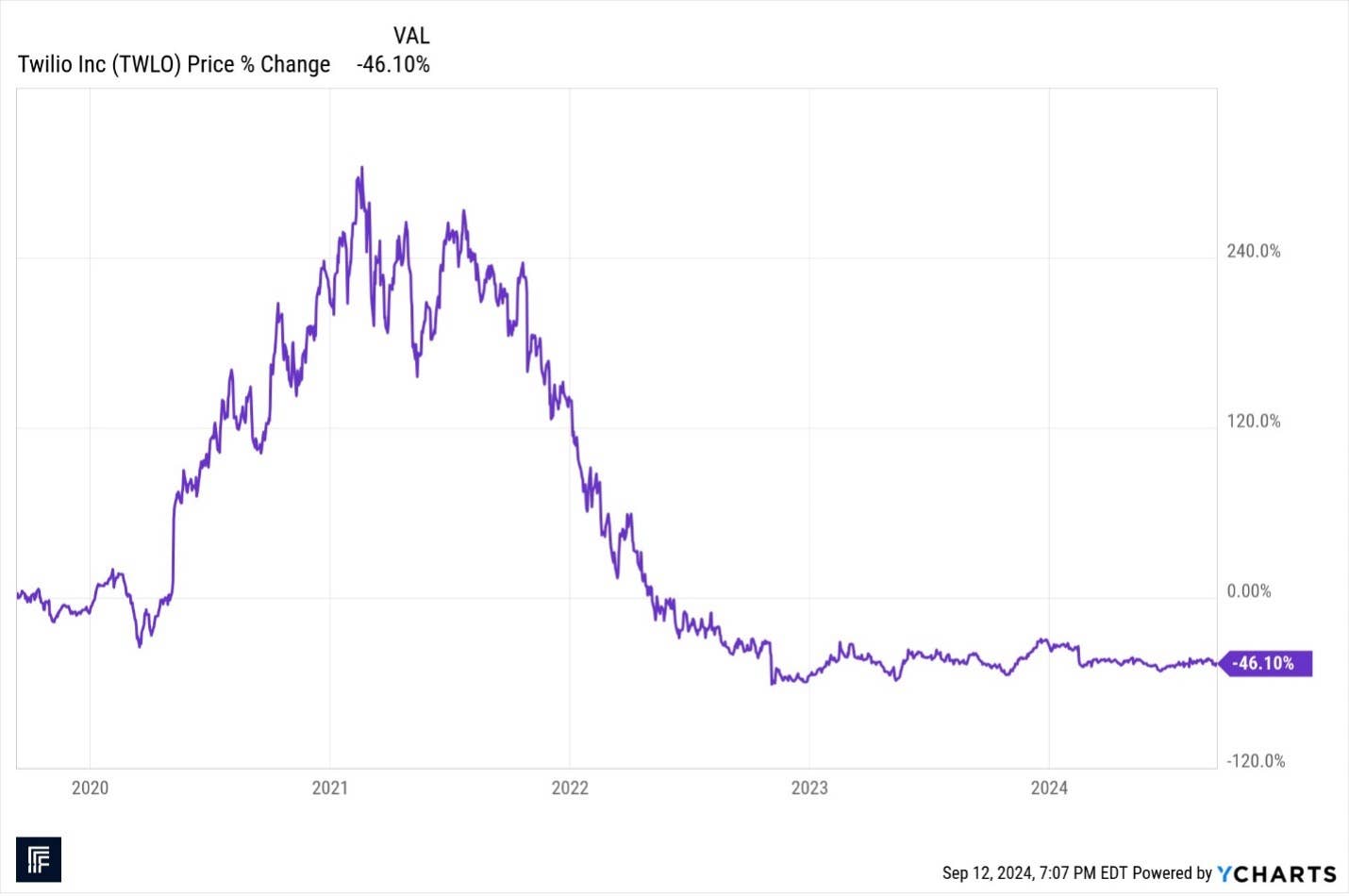

Your advice may not always work because of client emotions. You must prepare investors for tax bills and manage their expectations. For instance, a client recently had a concentrated position in Twilio Inc. TWLO, and I recommended they start trimming their holdings based on the quality, valuation, and sentiment criteria I discuss later in this article.

We began selling a portion of the stock, planning to scale out gradually, but the client was very upset after receiving their tax bill. After their tax return was filed, the client refused to sell any more shares. Despite still holding a concentrated position and repeated calls urging them to sell, the 80% decline in value of their remaining shares made the tax bill look like peanuts.

If a concentrated investment is overpriced to the point where it is likely to underperform the market on an after-tax basis for a long period of time, your priority should be reducing this position. Once that's addressed, you can shift focus to complementary, less correlated investments. However, before proceeding, it's essential to discuss a tax budget with the client. A tax budget sets clear guidelines, limiting the amount of taxes acceptable in the current year, often expressed as a percentage of the portfolio—for example, 2–5%.

It's important to recognize that setting the tax budget too low may not always be prudent. Clients with large concentrations in speculative companies or real estate could face losses that would severely impact their retirement plans. In such cases, it may be necessary to incur higher taxes to preserve the client’s wealth.

Building Client Confidence in You

Nobody can predict the future, so setting return expectations is inherently based on probabilities—though clients often dislike hearing about returns in those terms. For this reason, I focus on a sound, evidence-based methodology that can justify recommendations. This approach offers a more effective way to educate and motivate.

If there ever were a holy trinity in investing, it would be this - competitive returns, lower risk, and a lower tax bill. All three of these elements should be addressed in a great process. To do this, you have to have a clear way to estimate expected returns, and it has to be forward-looking, not based on historical averages. Your process must also increase diversification through non-correlated assets. The non-correlation should not just be based on statistics. It should also diversify non-related fundamental drivers. Ideally, new investments should also have an after-tax expected return higher than those you are selling.

Communicate your philosophy while you make recommendations. This will attract the right kind of clients, too. It’s amazing how many people are thankful after you’ve done little more than define an investment philosophy for them. They simply haven’t had the time or expertise to do so on their own!

Blocking and Tackling of Your Own Philosophy

The basics of your philosophy are no simple matter. In fact, it is one of the biggest determinants of whether you will keep clients long-term. I like to frame expected returns with some basics. One of the best frameworks for this comes from Benjamin Graham’s The Intelligent Investor, which emphasizes investing in assets with a long-term competitive advantage, diversifying, and avoiding overpaying for investments. It is useful because it works over the long-term, and it can be applied to most asset classes.

I’ve found it helpful to evaluate investments using three dimensions and to show the rationale to clients:

1. Quality: This refers to the stability of cash flows, the security of the financial position, and the strength of the long-term competitive advantage. The higher the quality, the longer you can hold an investment.

2. Valuation: This assesses the current market value of the investment relative to its intrinsic value based on cash flows, growth, and net assets. It helps determine whether an investment should be trimmed or eliminated based on its expected returns over time.

3. Sentiment: This gauges the short-term sentiment surrounding the investment. Is the market bullish or bearish? Investments often present excellent selling opportunities when short-term sentiment is rising.

Using these dimensions provides a structured way to assess and communicate investment opportunities, offering clients clarity and confidence in the process. If these dimensions don’t work for you, find the factors that resonate most with you and your clients.

Create Your Process

This is the process that I use with clients to reduce taxes, preserve wealth, and improve potential returns. It is in a logical order that makes sense to the client across the three investor scenarios:

Step 1: Initial Consultation. Start with a clear discussion to understand the client’s goals, risk tolerance, and emotional attachment to certain securities. Get a clear view of the portfolio structure by obtaining a detailed view of the client holdings: public and private securities, real estate assets, and business interests. Discuss concentrated positions that may pose significant risks or create future tax liabilities.

Step 2: Complete a Thorough Portfolio Evaluation. Analyze each asset’s financial health by evaluating and ranking each holding based on quality, valuation, and technical conditions. For stocks, evaluate profitability, cash flows, debt levels, and growth potential as well as industry dynamics. For real estate, review rental income, tenant trends, and market liquidity. Identify concentrations and overvalued positions that pose risk and evaluate unrealized gains.

Step 3: Create a Tax Budget. Set a manageable tax budget that balances reducing risk with minimizing tax liabilities. Decide on the acceptable tax exposures for the current year (e.g., limiting taxes to 2 – 5% of the portfolio value) while considering the urgency of diversifying away from concentrated positions. For stocks, rank holdings by appreciation and focus on selling the least appreciated long-term capital gain assets with the worst expected return first. Sell any underperforming assets or loss-making positions to offset gains and reduce the overall tax impact. For real estate, explore 1031 exchanges and other tax deferral strategies, such as diversifying into attractive UPREITs for tax deferral, improved liquidity, and diversification. Explore charitable giving.

Step 4: Implement Improved Return Potential and Diversification to Reduce Risk. Work toward a target allocation that reduces over-concentration in any one sector or asset class. Focus on reallocating funds into non-correlated assets compared to concentrated risks while maintaining long-term growth potential. Reinvest proceeds in high-quality assets that offer long-term competitive advantages, reasonable valuations, and potential for better growth. Use evidence-based approaches to target investments so that the client can understand the rationale behind reallocating capital.

Key Takeaways:

Process and Personalization Drives Advisory Success

I’ve identified three major opportunities for independent wealth advisors, all of which involve selling highly appreciated assets.

- You need to be both an economist and therapist

- Have a clear philosophy and well-defined process that provides immediate value and earns your clients' trust. Avoid cookie-cutter advice!

- Discuss tax budgets early in the process so that you both agree on what is acceptable

This positions you as a knowledgeable, proactive advisor, capable of delivering lasting value—which, in turn, will accelerate your growth.

Thank you for reading the first edition of TheStreet Pro’s Wealth Advisor Letter. Please leave a comment below and let me know what strategies you use with your clients to help their portfolios become tax-efficient.

Louis Llanes, CFA, CMT