In This Market, There's No Rest for the Wicked

Let's see if risk is back on after a through thrashing, whether the Fed will protect us on the recession tightrope — and why my Nvidia add was my best single trade in a while.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Terrific Tuesday. So, it is. Remember though that damaged assets must gain far more than they lose in percentage terms before they break even. Losing 25%, one needs to gain 33.3% to break even. I think the bulls will take the Nikkei 225's 10.2% Tuesday rally. That said, while far better than a sharp stick in the eye, Tuesday's activity, which is welcome, has not gone quite as global as Monday's had, and does not replace all the market cap that had been lost.

The rebound across Asia has been somewhat spotty, as has the opening across Europe. It does not feel to me to be honest that the yen carry trade has been completely unwound. Remember, Japanese accounts, including and especially the Bank of Japan, are the largest investors in aggregate in U.S. sovereign debt. That said, the U.S. dollar is up against the yen on Tuesday, but still not back even to Friday's levels.

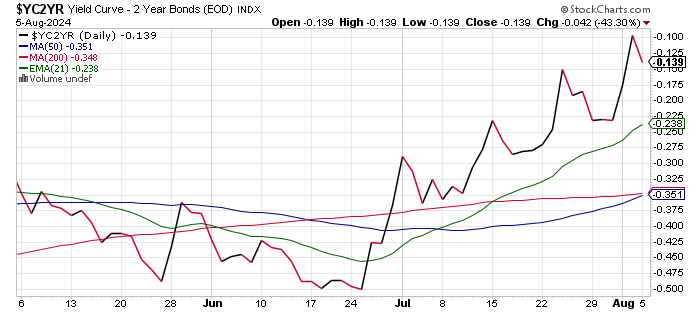

Speaking of U.S. sovereign debt securities, the spread between the yields of the U.S. Ten Year and Two-Year Notes did briefly "un-invert" on Monday, and then went back to their usual positions relative to one another. One can see here that this spread is clearly still in a rising trend and has been since late June.

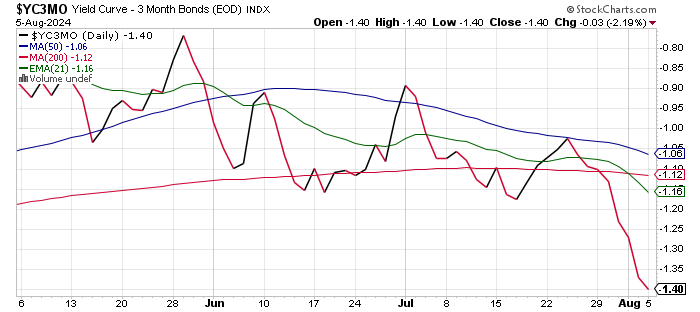

For the day on Monday, the yield for the U.S. Ten Year Note dropped just two basis points to 3.77% after having been lower. The yield for the U.S. Two Year Note closed almost flat at 3.88%. These two yields stand at 3.85% and 3.98% respectively as I work my way through the zero-dark hours. Interestingly, the inversion of the spread between that U.S. Ten Year Note and the U.S. Three Month T-Bill has only been exacerbated over this same time frame. This spread is considered to be the most accurate predictor of economic contraction in the Treasury yield curve toolbox and appears to be playing along with the Sahm Rule trigger experienced late last week. ...

We'll Make Right, Said Fed ...

On Monday, Chicago Fed Pres. Austan Goolsbee appeared on CNBC. Chicago is not a voting member of the Federal Open Market Committee this year, but Goolsbee did vote last week as an alternate in place of the recently retired Loretta Mester, who ran the Cleveland Fed. Goolsbee stated, "The Fed's job is very straightforward, maximize employment, stabilize prices and maintain financial stability. That's what we're going to do."

I'm pretty sure the central bank is still officially operating under a dual mandate and that this third mandate is both implied and understood. Just thought I'd point that out. Goolsbee added that if there were to be an economic deterioration that "we're going to fix it."

Oh boy. I feel better.

San Francisco Fed Pres. Mary Daly also spoke publicly on Monday. San Francisco does hold FOMC voting rights this year. Daly said that the Fed "Will do what it takes" to meet its dual mandate (yes, dual), but added: "We look at the totality of the information before we act," suggesting that overall economic activity is a concern. At least that was how I took it.

More importantly perhaps than anything said by these two Fed officials, were words spoken by former Fed economist Claudia Sahm on Bloomberg Television. Sahm, who is currently chief economist at New Century Advisors, who has become a lot more famous since her recession indicator was triggered on Friday, said that it was "very unlikely that we are in a recession." But, she added, "The changes that the Sahm rule picks up on do not look encouraging. They're headed in the wrong direction, and that momentum is what can get us into trouble."

Quite ominously, Sahm added, before her interview was over, that "We might not be there (in a recession), but we're getting uncomfortably close."

Gee, I wonder if anyone who writes a daily markets column for TheStreet Pro, who has held several fancy corporate Wall Street titles with the word "economist" in them, has been saying almost exactly that for several months now.

The Economics Anthem, According to Ozzy

I Don't Know

People look to me and say

"Is the end near, when is the final day?"

What's the future of mankind

How do I know, I got left behind

Everyone goes through changes

Looking to find the truth

Don't look to me for answers

Don't ask me, I don't know

- Ozzy Osbourne, 1980

A Thorough Thrashing

U.S. markets were severely beaten again on Monday. The S&P 500 gave up 3% for the session adding to losses of 1.37% and 1.84% experienced last Thursday and Friday. The S&P 500 is now down 6.8% in three sessions and down 8.5% over a rough three weeks since the mid-July high. The Nasdaq Composite surrendered 3.43% on Monday and now stands down 8.9% from Thursday's high and down 15.3% from its mid-July high. The transports, small caps and banks offered no refuge for the wicked on Monday, nor have they of late. In fact, even the more defensive sectors were taken out to the woodshed on Monday.

All eleven S&P sector SPDR exchange-traded funds shaded well into the red on Monday, as the Industrials XLI and Staples XLP were the only two among them to lose less than 2%. Technology XLK and the Financials XLF led the way lower. That said, two Sarge names, CrowdStrike CRWD and Advanced Micro Devices AMD performed well during the day and another, Palantir Technologies PLTR did well after the close. This helped keep the Sarge-folio in the green on Monday. Perhaps the best single trade I made in a while was the overnight addition to the Nvidia NVDA long 24 hours ago. That stock closed down 6.36% for the regular session, but up 6.28% from where those purchases were made.

Breadth was awful on Monday. Losers beat winners by a stunning 13-to-1 margin at the NYSE and by a rough 6 to 1 at the Nasdaq. Advancing volume took just a 7.5% share of composite NYSE-listed trade and a 20% share of composite Nasdaq-listed trade. Aggregate trade was up on a day over day basis across both exchanges as well as across the memberships of the S&P 500 and Nasdaq Composite.

Remember: All That Glitters

When the spit hit the fan, gold held up better than Bitcoin. Bitcoin may or may not be a better investment. However, it is clearly not a better store of value. I remain long actual physical gold as well as the SPDR Gold Shares GLD and the Goldman Sachs Physical Gold Fund AAAU.

Are We Entering a Recession ... Or Approaching One?

As we wonder whether or not the U.S. is entering into or close to entering into recession, the one slice of macroeconomic data released on Monday was quite "growthy" in nature. The ISM Services PMI rebounded from a weak June into July, not behaving at all like its Manufacturing counterpart.

For the July release of the ISM Services survey, the headline print moved back into expansionary territory as did such key components as new orders, production, employment, and order backlog. Unfortunately, pricing not only remained hot, but accelerated into July and has now been in a state of expansion for an incredible 86 consecutive months. That's more than seven years if you're looking to blame one side of the aisle or the other.

Economics (All Times Eastern)

8:30 a.m. - Balance of Trade (June): Last -$75.1B.

8:55 - Redbook (Weekly): Last 4.5% y/y.

4:30 p.m. - API Oil Inventories (Weekly): Last -4.495M.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: CAT (5.54),DUK (1.02), KVUE (0.28), PLNT (0.66), UBER (0.53), VMC (2.50)

After the Close: ABNB (0.94), AMGN (5.00), SMCI (8.21), UPST (-0.39), WYNN (1.19)

At the time of publication, Guilfoyle was long CRWD, AMD, PLTR, NVDA, GLD, AAAU.