In the Fight Between the Big-Caps and the Mid-Caps, the Biggies Still Lead

Let's compare the big-caps to the mid-caps to see who's in the lead, before looking at the indicators to see where we might go.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

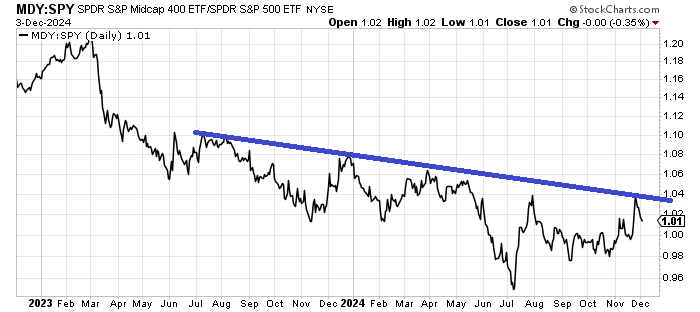

I was asked to look at the chart of the Mid Caps relative to the big caps and I must say I was quite surprised. I hear so many folks recommending Mid Caps and I figured this chart would show how strong they have been. But rather I see a chart where the Mids haven’t been able to make a higher high vs the S&P in two years.

I realize the last few days where the Mag 7 have taken the lead once again haven’t helped the cause but even before that, this blue line stays intact. If we are to head into a period of Mids outperforming Bigs, then this ratio will need to get over that line, just to show us it can make a higher high. I am eyeing that late July high for the ratio at 1.04 as the level it needs to surpass.

Speaking of the Mag 7, or index movers, I feel compelled to note the volume for the QQQs on Tuesday was incredibly low. It came in at 16 million shares. Recall just over a week ago I noted that 25 million had become the norm and that felt quite low. I don’t believe we’ve seen a non-holiday trading day with a mere 16 million shares.

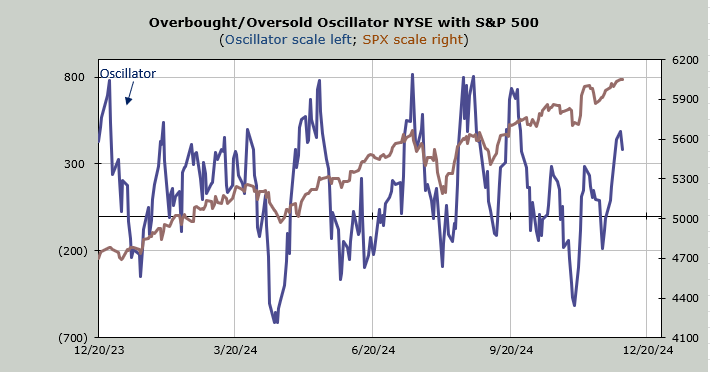

Now let’s talk about breadth. It’s been fine. I would not call it great, just fine. It went from lagging to catching up and it acts more like the S&P is running a few feet ahead of it and the breadth is always trying to catch up.

But something changed on Tuesday. Breadth wasn’t terrible considering the Russell was down 17 points but the S&P has added 17 points this week and breadth hasn’t been positive yet. And that has taken its toll on the McClellan Summation Index.

Yesterday I noted that I thought the Summation Index was lethargic in that it had hardly pushed upward even though the direction was up. That’s the blue line on the chart. After the last two days of negative breadth a mere net negative of -400 advancers minus decliners on the NYSE will halt that rise in the Summation Index. That is not much of a cushion as we head into a short term overbought reading later this week.

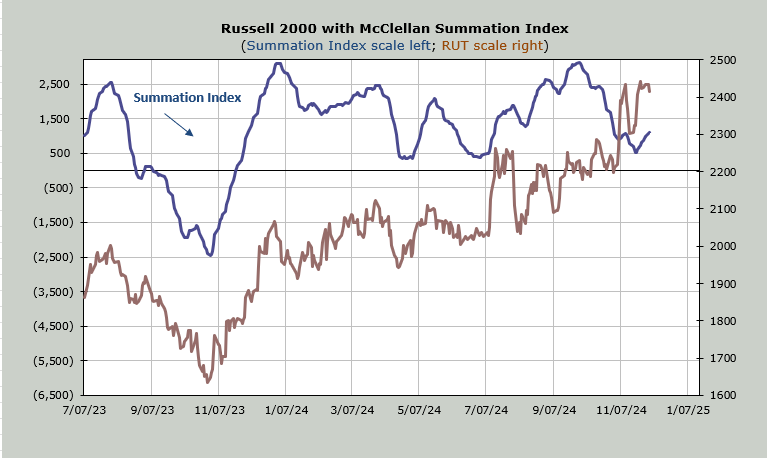

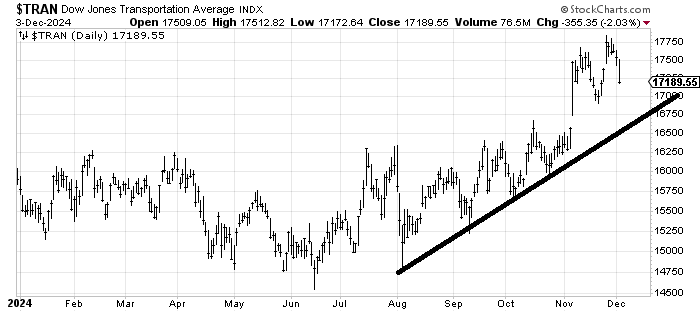

Now it may very well ‘right’ itself and give us a better cushion as we head into the end of the week but I would also like you to look at the Transports. That was a two percent whack on Tuesday that no one seemed to even mention. And they were already down a percent from the high coming into the day.

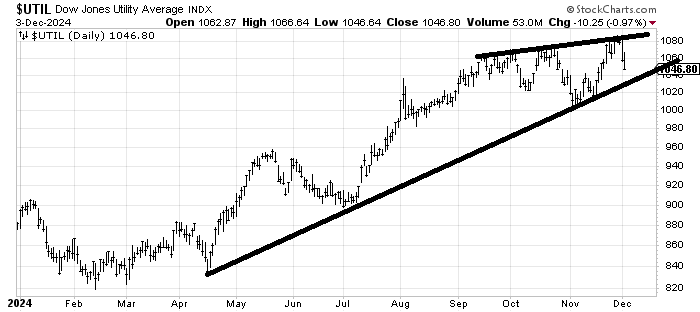

We looked at the Utes a few days ago but they lost another percent on Tuesday as well. They are now down three percent from their recent high. Just remember that the Utes were the ones that I believe gave us the heads up on the bond rally. Are they doing the same again?

After all, the REITs and staples took hits on Tuesday too.

I said I expect the bonds to pullback (they did on Tuesday) but this type of action as we head into an overbought condition has me still in the camp that we get a pullback next week in stocks (followed by a Christmas rally). I get the sense folks might not be ready for a pullback though. A little volatility would shake things up.