High-Stakes Friday

After Wednesday's Fed-fueled risk asset fall and Thursday's early climb, volume could be wild today. Also, let's look at the buck, incoming econ data, the Nasdaq's chart and more.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Stocks roared out of the gate on Thursday morning, as if there was a mass intent to take back some lost ground after Wednesday afternoon's Fed-inspired risk asset bonfire. Markets settled into a range that lasted more or less for the rest of the singular trading session only to wilt through the final hour of that session. It was then that the true nature of the day was revealed. The rally had been a trap set for momentum traders as short-term profits were taken and what green had been on the screen for most of the day turned a pale shade of red.

No, in case folks were wondering, months of pricing in easier money next year cannot be priced out in just a few hours. Our beloved marketplace will skate on thin ice for now, and when there is reason, exposure to risk will be reduced. That said, this morning is Friday morning. Happy Fri-Yay to all! Now, what's this risk you speak of?

Risky Friday

Risks to my portfolio, let me count the ways. Where do I begin? No, this won't be an "earnings day" but it will be a "macro day." I often mock the monthly personal consumption expenditure price index data as redundant, as it tends to run along the same trends as the much more closely followed month consumer price index numbers, even if it does run below the CPI. That's most likely why it's the Fed's "favorite" measuring stick for consumer-level inflation. This morning, we'll get the November PCE release and as these releases come so late in the following month, there tends to be less of a chance for surprise as there is for the CPI release.

That said, this morning we expect to see the headline PCE print at monthly growth of 0.3% and annual growth of 2.5%, which would be up from 2.3% for October. At the core, we're looking for monthly growth of 0.2% and year-over-year growth of 2.9%, up from October's 2.8%. After The Federal Open Market Committee's hawkish cut on Wednesday, any upside surprises here, especially because the year-over-year numbers could provoke another algorithmic beat-down. Oh, and the inflation expectations part of the University of Michigan's revision to their December Consumer Sentiment survey could impact markets as well.

The data is not where the risk ends. Readers likely noticed that U.S. equity index futures are weak this morning after weakness spread across both Asia and Europe. Traders and investors are on edge and fully aware that this Friday is not just Friday, it's a "triple witching" expirations event Friday and as far as those are concerned, this one could be a doozy. Estimates for the notional value of options tied to equities, indexes and exchange-traded funds seem to be running as low as $6.6 trillion and as high as $7.7 trillion, at least according to what I have seen. Keith McCullough, co-founder and CEO of Hedgeye Risk Management tweeted early this morning that the bulk of "nearly $4.5T in national open interest" that was linked to either the S&P 500 or the SPDR S&P 500 ETF Trust SPY alone were set to expire this morning.

Lastly, there is the added pressure of a likely government shutdown tonight after the House of Representatives rejected a temporary funding plan backed by Pres. Elect Donald Trump. Nearly all House Democrats voted against the bill, and they were joined by 38 House Republicans. The short-term resolution would have pushed the funding deadline out to March 14 and made this a Trump problem instead of a Biden problem. Don't be surprised if the government does start to shut down this evening.

Dollar Bill Y'all

You kids see the U.S. Dollar Index soar on Thursday? Gee whiz, it was as if the U.S. dollar had been shot out of a cannon. Overnight, I have seen the U.S. Dollar Index trade as high as 108.43 after trading with a 106 handle just ahead of the FOMC's economic projections on Wednesday afternoon. The stronger dollar put the whammy on Crude prices, and cryptocurrency prices, especially Bitcoin. The most well-known cryptocurrency, at last glance, was trading more than 12% off of its intraweek high. Gold is down for the week, but interestingly, up since Wednesday afternoon despite the stronger greenback as some investors seek safe haven.

Equities

Not the kind of rebound some had hoped for. Perhaps the stronger economic data had something to do with that. On Wednesday morning, the Bureau of Economic Analysis revised its estimate for Q3 gross domestic product up to growth of 3.1% (q/q, SAAR) from 2.8%. In addition to that, the weekly report on initial jobless claims printed below expectations< Perhaps most impressively though, the Conference Board's Index of Leading Indicators for November printed in positive territory at +0.3% m/m. This ended an eight-month losing streak for this series and proved to be only the second positive month for this series in the past 32. Not a misprint. But the economy is strong, they said.

Almost all of our major and mid-major equity indexes closed moderately lower for the session, despite having traded higher earlier. The only winner I saw was the Dow Jones industrial average. At a gain of just 0.04%, the Dow ended a 10-day losing streak. The S&P 500 closed 0.09% lower as the Nasdaq Composite closed down 0.1%. The Russell 2000 again took the brunt of investor ire at -0.45%. Interestingly, the Philadelphia Semiconductor Index closed significantly lower at -1.56% as Micron Technology MU took a beating of 16.2%, and Lam Research LRCX suffered a loss of 5.3%, but I question the performance of that index on Thursday as the Dow Jones US Semiconductor Index was down "just" 0.3% and they supposedly cover the same turf.

Eight of the 11 S&P sector SPDR exchange-traded funds closed in the red on Thursday, led lower by the REITs XLRE as that group continues to suffer from the normalization of the slope of the Treasury yield curve and the Materials XLB as that group was hammered by dollar strength. The winners on Thursday were the Utilities XLU and the Financials XLF.

Perhaps Most Interesting...

Winners beat losers at the NYSE by a rough 2 to 1 and at the Nasdaq by about 4 to 3. Advancing volume took a 39.7% share of composite NYSE-listed trade and a 46.3% share of composite Nasdaq-listed trade. However, aggregate trading volume receded from Wednesday's levels for names domiciled at both exchanges. As stocks generally moved sideways. You kids get where I am going with this?

With today being a triple-witching event and also the final trading day ahead of a holiday shortened week, with the holiday smack-dab in the middle of next week, chances are that trading volume today will be out of control.

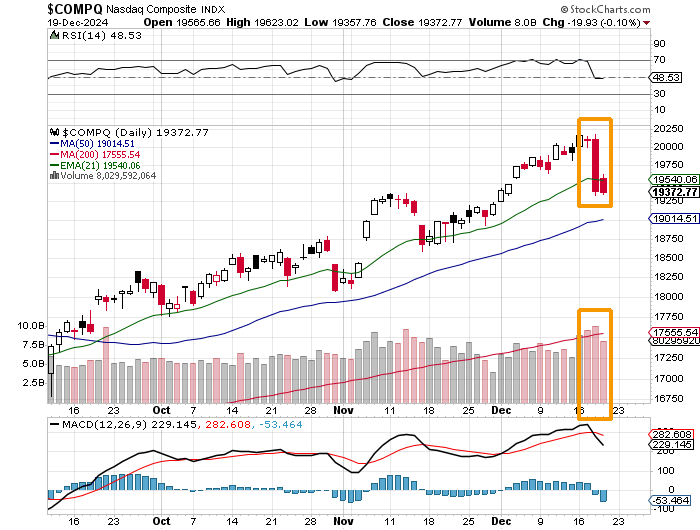

I will use the Nasdaq Composite, but the concept holds true for the S&P 500 as well. While Tuesday into Wednesday counted as a Day One in terms of identifying a downward change in trend, Thursday, though slightly lower, still sported lower volume and could potentially count as the break we needed to see before Day One and the next shoe to drop. That next shoe could be today. Assuming that we'll experience greatly increased trading volume, all we'll need to see is some sharp equity market weakness and we'll have that confirmation.

Confirmation. Ahead of the Santa Claus Rally period. Typically, the Santa Claus Rally, which covers the final five trading days of the outgoing year and the first two trading days of the incoming year, is positive a little more than 75% of the time and produces an average gain of close to 1.5% for the benchmark index (formerly the DJIA, currently the SPX).

Well, you can't have your cake and eat it too. Either this likely confirmation will fail, or Santa's not coming. Both of these market "truths" cannot co-exist at this time.

Economics (All Times Eastern)

08:30 - Personal Income (Nov): Expecting 0.4% m/m, Last 0.6% m/m.

08:30 - Consumer Spending (Nov): Expecting 0.5% m/m, Last 0.4% m/m.

08:30 - PCE Price Index (Nov): Expecting 0.3% m/m, Last 0.2% m/m.

08:30 - Core PCE Price Index (Nov): Expecting 0.2% m/m, Last 0.3% m/m.

08:30 - PCE Price Index (Nov): Expecting 2.5% y/y, Last 2.3% y/y.

08:30 - Core PCE Price Index (Nov): Expecting 2.9% y/y, Last 2.8% y/y.

10:00 - U of M Consumer Sentiment (Dec-F): Flashed 74.0.

10:00 - U of M One Year Inflation Expectations (Dec-F): Flashed 2.9%.

10:00 - U of M Five Year Inflation Expectations (Dec-F): Flashed 3.1%.

13:00 - Baker Hughes Total Rig Count (Weekly): Last 589.

13:00 - Baker Hughes Oil Rig Count (Weekly): Last 482.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: WGO (.19), CCL (.07)

At the time of publication, Guilfoyle had no position in any security mentioned.