Habit of Divergence, Powell Lifts the Banks, A Palantir Positive, Albemarle's Chart

Yellen implied Tuesday that consumer inflation that emerged in 2022 was driven more by global supply-side shortages than reckless fiscal policy. Yeah, and I have a bridge to sell you.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

What is the purpose of marking time? To get your cover and alignment, Sir.

Anyone who has ever spent any time marching in a parade or learning close order drill has been asked this question or something like it by someone probably a little scarier than they expected wearing a Smokey Bear/Campaign hat. The answer provided is clear. Marking time is to march in place, while using the thunder of the boots striking the ground to get instep. To cover down is to line up 40 inches behind the noggin to your front, and to align is to form up with your shoulders four inches from the shoulders to your left and right.

This is what makes everything look neat and organized. This is the first impression any unit or organized mass of humanity makes on the public or any leader of such humanity makes on his or her superiors.

While on the surface, accomplishing nothing, marking time is an expression of both precision and discipline. The markets, if anything, appeared organized on Tuesday and though both Fed Chair Jerome Powell and Treasury Secretary Janet Yellen testified before our legislators. In the end, little was accomplished, but everything was neat and appeared quite organized.

Yellen

In her appearance before the House Financial Services Committee, Treasury Secretary Janet Yellen did little more than tell legislators how effective President Biden has been in his dealings with her and that the president's cabinet has not met to discuss invoking article 25 of the U.S. Constitution. For those not in the know, the Secretary of the Treasury is a member of the cabinet and Article 25 of the U.S. Constitution to replace a U.S. president who has become unable to fulfill that leadership role can only be invoked by the cabinet. Congress does not have that power or authority.

Yellen did not really provide any newsworthy testimony as far as our purposes are concerned other than to acknowledge that labor markets have cooled and to imply that the burst of consumer inflation that emerged in 2022 had nothing to do with reckless fiscal policy but was more driven by global supply-side shortages. Yeah, and I have a bridge to sell you.

Powell on Policy

Powell's appearance was really pointed in multiple directions. The Fed Chair stated that "Elevated inflation is not the only risk we (the Fed) face," as he too acknowledged a softening labor market.

On employment, Powell added, "The latest data show that labor market conditions have now cooled considerably from where they were two years ago, and I wouldn't have said that until the last couple of readings." The last part of that quote was likely in reference to the unemployment rate that has now gone higher for three consecutive months.

While implying that cutting trees too soon, too deeply could reverse progress made in the fight against consumer-level inflation, Powell did offer those looking for easier monetary conditions some hope... "More good data would strengthen our confidence that inflation is moving sustainably toward 2%." On that, headline CPI, on a year-over-year basis, has exhibited overt disinflation for two straight months with expectations for a third when that data point is reported tomorrow.

I would warn readers that due to base effects, year-over-year disinflation could look authentic into August/September. This is/was expected...then, later this year it gets tough again. That could provoke an error in policy if the FOMC is simply looking for an excuse to decrease short-term rates ahead of the election.

Powell on the Banks

Powell did provide a pre-earnings boost to big bank stocks as he confirmed to the Senate Banking Committee that officials will likely soon release a changed version of the Basel III proposal that could have forced U.S. banks to hold up to 19% more in reserve than they have been in order to buffer against losses in an economic downturn.

He did not offer a specific percentage increase that is currently in discussion but did say that officials "are very close to agreeing on the substance of those changes." He also added that there would be a "need to put a revised proposal out for comment for some period."

The KBW Bank Index gained 1.52% on Tuesday, making that index an upside outlier for the day. Citigroup C, JP Morgan JPM, Bank of America BAC and Wells Frago WFC all gained between 1.2% and 2.8% for the day.

Tuesday Came and Went...

.... Leaving barely a ripple. The S&P 500 gained a whopping 0.07% for the regular session, while being "outperformed" by the Nasdaq Composite, which was up 0.14%. Gee willikers, Batman, both of those indexes closed at record highs. Again. That is getting to be a habit, a habit of divergence and does not imply that Tuesday was much of an "up" day across the marketplace.

The small-to mid-cap indexes all closed at least 0.45% lower, while the Dow Transports (-1.09%) closed in the hole for a third straight session. Smaller-cap stocks and transportation stocks are more highly dependent upon growing economic activity than are many other slices of our equity markets, just in case this is the market sending a message.

Six of the 11 S&P sector SPDR ETFs closed in the green for the session, led by the Powell-infused Financials XLF at +0.77%. No other fund among these 11 even gained half of one percent on Tuesday. Materials XLB and Energy XLE led to the downside at -1.02% and -0.88%, respectively. Those are both commodity-driven sectors, meaning that they are cyclical in nature, or more dependent upon the business/economic cycle for performance.

Losers beat winners by roughly 7 to 4 margin at the NYSE and by about 5 to 4 at the Nasdaq. Advancing volume took just a 42.3% share of composite NYSE-listed trading volume, but a surprising 54% of composite Nasdaq-listed trade. As for aggregate trading volume, activity increased by 1.5% day over day across NYSE-listed names but decreased across Nasdaq-listed names by 8.5% rendering much of the day's price discovery as less significant in projecting the big picture.

Anyone Else Notice?

That the NFIB Small Business Optimism Index for June printed up from May at 91.5. In fact, this was the strongest print for the survey year to date (since December). Granted, prior to 2021, prints above 100 for this series were the norm, but June was the third most optimistic month of the past 19 for small business owners. The earnings outlook was still -29%, so let's not get that excited, but even that was an uptick.

In Other News

Early Tuesday morning, Oracle ORCL announced that Palantir's PLTR Foundry Platform and Artificial Intelligence Platform (AIP) were certified on Oracle's Cloud Infrastructure and will now be generally available across all of Oracle's distributed cloud deployment options.

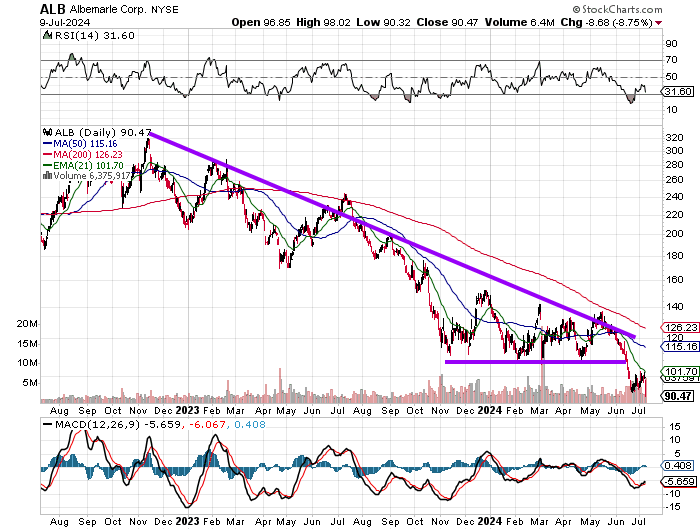

Awful Chart

Lithium has gone from trading at $85,000 per metric ton in late 2022 to roughly $12,500 per metric ton on Tuesday. That's about an 85% drop over that time. The short-term prospects do not appear strong either.

Remember former Sarge-fave Albemarle ALB? Haven't taken a look at that chart in a long while? If you've had this stashed away in your book without really taking that good look, you should probably sit down.

Buy ALB now that it has broken out to the downside coming out of a descending triangle? I need to see more life than that. The shares are still trading below triangle support, Relative strength is still relatively weak, and the daily Moving Average Convergence Divergence (MACD) is still in deeply bearish territory despite showing some recent improvement.

I am still waiting on this one.

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 7.03%.

07:00 - MBA Mortgage Applications (Weekly): Last -2.6% w/w.

10:00 - Wholesale Inventories (May-rev): Flashed 0.6% m/m.

10:30 - Oil Inventories (Weekly): Last -12.157M.

10:30 - Gasoline Stocks (Weekly): Last -2.214M.

13:00 - Ten Year Note Auction: $39B.

The Fed (All Times Eastern)

10:00 - Speaker: Federal Reserve Chair Jerome Powell.

14:30 - Speaker: Reserve Board Gov. Michelle Bowman.

14:30 - Speaker: Chicago Fed Pres. Austan Goolsbee.

19:30 - Speaker: Reserve Board Gov. Lisa Cook.

Today's Earnings Highlights (Consensus EPS Expectations)

After the Close: AZZ (1.29), PSMT (1.05), WDFC (1.27)

At the time of publication, Guilfoyle was long WFC and PLTR equity.