'Golden Weakness'

Chinese stocks make a U-Turn as stimulus hopes fade following the holiday week. Also, NVDA, AMD breaking out.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The surging Chinese stock market finally rested and even reversed course on Tuesday as mainland stocks reopened after being closed for the "Golden Week" holiday period. Call it ... the "Golden Pause." There had been some expectation that Beijing would announce even more, or at least specify, fiscal stimulus measures upon returning from the time off, which so far has not happened. Traders and investors started to lose conviction that mainland Chinese authorities will ultimately implement enough fiscal spending coordinated with easier monetary policy to support the recent run higher for Chinese equities.

The World Bank on Tuesday reiterated its estimate for 2024 Chinese gross domestic product growth of 4.8%, decelerating to growth of 4.3% in 2025. Meanwhile, Zheng Shanjie, who is chair of the National Development and Reform Commission, charged with Beijing state economic planning, stated that he had "full confidence" that the mainland economy would achieve its targeted 2024 GDP growth level of 5%. His projected confidence seemed to sap investor confidence that the kind of help insinuated by the politburo more than a week ago was indeed on the way.

The Hong Kong-based Hang Seng Index, which had not closed for the week-long holiday and had been up 35% since its mid-September lows, gave back 9.4% on Tuesday. The Shanghai Composite that had closed for the holiday, did close Tuesday up 4.6% as it had some "catch up" to do, but that was also 4.7% off of the day's highs. The CSI 300, which is an index composed of blue-chip stocks drawn from listings from both Shanghai and Shenzhen (sort of similar to the relationship between the NYSE & Nasdaq) opened up 10.8%, but closed up 5.9%. This negative U-turn for Chinese stocks also put the whammy on European equities, though U.S. equity index futures appear to be up small several hours ahead of the opening bells in New York City.

'Insane' Chip Demand, Indeed

Taiwanese tech manufacturing giant Foxconn, better known as a supplier to Apple AAPL, is reported to be building the largest manufacturing facility in the world to supply Nvidia NVDA with GB200 superchips in order to meet what Nvidia CEO Jensen Huang referred to as "insane" demand. The new facility is aimed at meeting this demand for chips built on the Blackwell architecture, which Benjamin Ting, senior VP for Foxconn's cloud enterprise solutions business referred to as "awfully huge."

Fed Speak That Makes You Go ... Hmmm...

On Monday, Minneapolis Fed Pres. Neel Kashkari said, "The balance of risks have shifted away from higher inflation towards higher unemployment."

Whether intended or not, this seemed to indicate that perhaps Kashkari did not have so much faith in the recently reported Bureau of Labor Statistics employment surveys for September, which crushed expectations. U.S. stocks seemed to react negatively, though Minneapolis does not vote on policy again until 2026.

But early this morning, Fed Gov. Ariana Kugler spoke to the ECB at Frankfurt and soothed those trading U.S. markets. Kugler said, "If progress on inflation continues as I expect, I will support additional cuts in the federal funds rate to move toward a more neutral policy stance over time."

Obviously, Gov. Kugler and I are not looking at the same models. I see this past September as the low in year-over-year consumer-level inflation, and some gradual re-acceleration beginning with October or November, but probably October.

Kugler added: "If downside risks to employment escalate, it may be appropriate to move policy more quickly to a neutral stance. Alternatively, if incoming data do not provide confidence that inflation is moving sustainably toward 2%, it may be appropriate to slow normalization in the policy rate."

At least she "sort of" checked herself. Another Fed official showing, either not so much confidence in the September employment surveys, or a Fed official that understands how foolish the Federal Open Market Committee looked back on Sept. 18 for aggressively cutting rates with labor markets "supposedly" not under pressure and inflation certainly not beaten.

A Not So Risky Marketplace

Monday certainly was not a "risk-on" day on Wall Street. As mentioned, 24 hours ago, there had been early selling pressure across the spectrum of U.S. Treasury debt securities. The yields of the U.S. Ten- and Two-Year Notes actually did re-invert briefly on Monday, before the Two-Year Note rallied slightly. As I bang out this morning note, U.S. Ten Year paper pays 4.02%, in line with where that product went out on Monday, while the Two-Year Note currently yields 3.97%, down one basis point from last Monday.

Crude oil prices continued to rise on Monday, despite a U.S. Dollar Index that has not given much back at all. The DXY still stands well above 102, but geopolitical concerns in the Middle East and unsettled weather in the Gulf of Mexico put upward pressure on oil futures prices. WTI has given back almost 2% as refining facilities in the Gulf do not look like they will be impacted by Hurricane Milton as that intense storm heads for a midweek collision with the west coast of Florida.

U.S. equities were hit in the nose on Monday. The Nasdaq Composite gave up 1.18% as the S&P 500 surrendered 0.96%. Some industry specific mid-major indices were not hit as hard as the Dow Transports, Philly Semiconductors, and KBW Banks gave back 0.2%, 0.19% and 0.15% respectively. Small caps, however, were slapped around. The Russell 2000 fell 0.89%, while the S&P 600 gave back 1.01%.

Interesting Note on Semis

While the Philadelphia Semiconductor Index did lose 0.15% on Monday, led to the downside by ASML Holdings ASML and Qorvo QRVO. Conversely, the Dow Jones U.S. Semiconductor Index gained 0.9% on Monday (despite measuring the same industry), led higher by Nvidia and Taiwan Semiconductor TSM.

Breadth

Ten of the 11 S&P sector SPDR exchange-traded funds closed out the Monday session in the red on Monday, led lower by the Utilities XLU as Treasury yields moved higher to compete with dividends. The XLU gave back 2.3% on Monday followed by three other sector funds that all lost more than 1%. Energy XLE was the lone winner among the 11 funds for the day, gaining 0.35%.

Losers beat winners at the NYSE by a rough margin of 8 to 3 and at the Nasdaq by roughly 7 to 3. Advancing volume took a 36% share of composite NYSE-listed trade, and a 44.1% share of composite Nasdaq-listed activity. Interestingly, despite the action having taken place on a Monday, aggregate trading volume was up ever so slightly across listings at both exchanges.

Is that meaningful? While I would like to see a more convincing increase in total trade in order to feel some conviction, we do have to pay attention to a Monday increase in trading activity from a Friday, especially when losers beat winners so decisively and declining volume tops advancing volume so decisively.

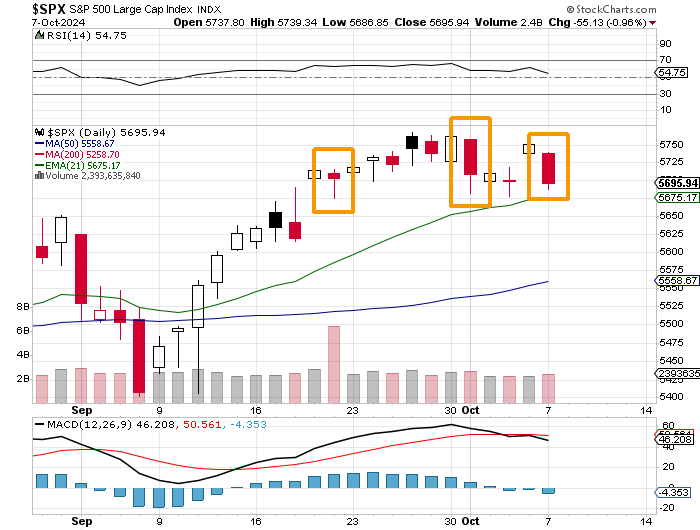

Going to the Chart...

I have highlighted for readers the last three times that the S&P 500 experienced a "down" day on increased trading volume.

These are not the kinds of Day One environments that set up "follow-throughs" that we used to see when humans, and therefore emotion, controlled a greater percentage of order flow.

Readers will see that the down day on Oct. 1 was very similar to the one yesterday. That one produced a downside trade that may have worked with precision timing but signaled no change in trend. The first one on this chart, came on Sept. 20, and as a Triple expirations Friday, bore greatly increased trading volume and also a mid-day reversal, so I don't know if we can take anything away from the high-volume red-candle session of that day. It certainly appears that the market did not.

Both...

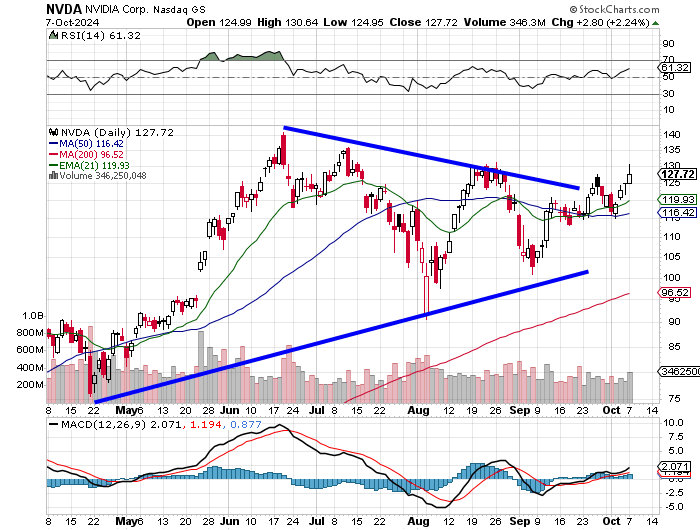

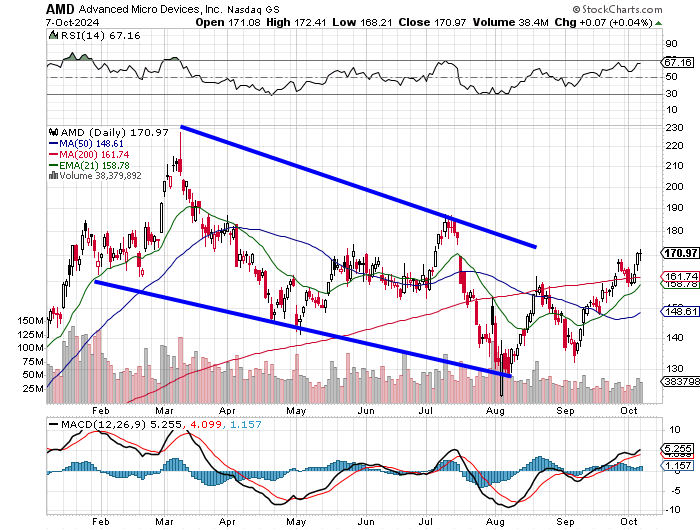

Nvidia and Advanced Micro Devices AMD continued to make progress on their technical breakouts on Monday. Remember, the Nvidia event ends tomorrow. The AMD event will be a one-day affair held this Thursday.

Breaking out from a pennant formation...

Breaking out from a falling wedge pattern.

Economics (All Times Eastern)

06:00 a.m. - NFIB Small Biz Optimism Index (Sep): Expecting 91.9, Last 91.2.

08:30 - Balance of Trade (Aug): Last $-78.8B.

08:55 - Redbook (Weekly): Last 5.3% y/y.

4:30 p.m. - API Oil Inventories (Weekly): Last -1.5M.

The Fed (All Times Eastern)

03:00 a.m. - Speaker: Reserve Board Gov. Adriana Kugler.

12:45 p.m. - Speaker: Atlanta Fed Pres. Raphael Bostic.

4:00 - Speaker: Boston Fed Pres. Susan Collins.

7:30 - Speaker: Federal Reserve Vice Chair Philip Jefferson.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: PEP (2.29)

At the time of publication, Guilfoyle was long XLU, NVDA and AMD.