Equity Haircut, BLS Revision, Walmart Leaving China, Netflix at a Crossroads

U.S. equity markets got a haircut and it was an uneven one at that.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

U.S. equity markets got a haircut on Tuesday, and it was an uneven haircut at that. For the major indices, it was just a trim. The S&P 500 gave back just 0.2%, as the Nasdaq 100 and Nasdaq Composite slipped 0.24% and 0.33% respectively as those three indices all saw eight-day winning streaks come to timely ends.

That Nasdaq performance came despite the drag created by a Philadelphia Semiconductor Index that surrendered 1.33%. The sell-off was far more severe elsewhere. Lattice Semiconductor LSCC and Intel INTC led the group lower, suffering beatings of 2.69% and 2.46%, in that order. The small caps were hit particularly hard as the S&P 600 gave up 1.19% and the Russell 2000 lost 1.17%. The KBW Banks were down an even 1% as the Dow Transports were tripped up for 0.91%.

There was just a touch of risk-off sentiment in the air, as traders moved at least some capital out of equities and into U.S. treasuries. The U.S. ten-year note went out on Monday, yielding 3.82%, down six basis points for the session. U.S. two-year paper paid 4.01% by day's end, also down six basis points. Overnight, I see U.S. equity index futures flat to slightly higher and those treasury yields close to unchanged.

The How and Why

What could have caused a trim off of the sides and top with all eyes still optimistically focused upon this Friday's presumably dovish address from Jackson Hole and next week's scheduled earnings release by market bellwether Nvidia NVDA? The answer is two-fold, my friends.

First, Fed governor and known policy hawk Michelle Bowman spoke publicly on Tuesday. Bowman is known to worry about a resurgence in consumer level inflation, and my feeling is that she is probably correct in her concerns over maintaining some vigilance. Speaking from Colorado Springs, Bowman said, "The progress in lowering inflation during May and June is a welcome development, but inflation is still uncomfortably above the committee’s 2% goal. I will remain cautious in my approach to considering adjustments to the current stance of policy.”

Remember, the algorithms that control the various points of sale for U.S. equities read keywords and react. There is no longer a human thinking about what to do. This was a hawkish statement.

Bowman added, “The rise in the unemployment rate this year largely reflects weaker hiring, as job searchers entering the labor force are taking longer to find a job, while layoffs remain low. It will become appropriate to gradually lower the federal funds rate to prevent monetary policy from becoming overly restrictive.”

That was dovish, and that's why Tuesday's sell-off did not become a rout.

Gov. Bowman was not the only direction markets were pressured from, to take some profits on Tuesday. Wednesday morning, at 10 a.m. ET, the Bureau of Labor Statistics will release that agency's preliminary estimate for its annual benchmark revision to the monthly non-farm payrolls prints released for the 12 months starting with April 2023 and ending with March 2024. I have seen estimates for this preliminary number that would erase anywhere from 500,000 to more than 1 million jobs that were never actually created during that period.

Depth and Breadth

The pressure on equities was broad on Tuesday. Eight of the 11 S&P sector SPDR ETFs closed out the regular session in the red for the day. Energy XLE at -2.64% easily led the retreat, while the three sectors that did manage to close in the green were all defensive in nature. The Staples XLP led in that direction at +0.48%.

Losers beat winners at the NYSE by just about two to one and at the Nasdaq by a little less than two to one. Advancing volume took a mere 28.6% of composite NYSE-listed trade and a more respectable 46.4% share of composite Nasdaq-listed activity. The catch was in the trading volume. Tuesday was not the busiest of sessions.

Aggregate trading volume was down 7.1% day over day for NYSE-listings and down 4.7% for Nasdaq-listings. Across the membership of the S&P 500, aggregate trade printed lower than the day prior for a third consecutive session. Tuesday's activity across that benchmark index fell a whopping 23% short of its 50-day trading volume simple moving average.

In fact, S&P 500 trading volume has not reached that 50-day average since August 7, 2024. This kind of puts a wee bit of doubt in most of the market's rally off of those August 5, 2024 lows. To once again borrow from Grant Williams, "Things that make you go hmmm."

Anyone Else Notice...

What came out of Deutsche Bank on Tuesday afternoon? Deutsche Bank strategist Henry Allen penned a research note on Tuesday where he pondered the short-lived yen carry trade near-mini crash of early August. Allen wrote "It's striking just how brief the recent turmoil was. In many respects, it's an even quicker version of what took place after SVB's collapse in March 2023, where volatility quickly spiked before subsiding again."

Allen continued, "Even as markets have stabilized, several of the fundamentals driving the selloff haven't gone away. Data has been increasingly soft at a global level, falling inflation means that monetary policy is increasingly tight in real terms, geopolitical concerns are elevated, and we're headed into a tough period on a seasonal basis."

Allen listed five reasons why the early August selloff could be re-ignited:

- Equity valuations are elevated, and positioning is overweight

- Economic data has been softening globally

- Monetary policy is becoming tighter in real terms as QT hums along

- September is historically the market's worst performing month

- Geopolitical tensions have not eased

Tell Us How You Really Feel

Either Walmart WMT needed the cash or perhaps has lost faith in China's ability to grow the consumer side of its economy, as had once been projected. News broke at zero-dark thirty on Wednesday morning that America's largest retailer, Walmart, had reportedly sold its entire $3.6 billion stake in Chinese e-commerce giant JD.com JD.

Walmart had owned just over 10% of JD and sold that stake at what looks to be an 11% discount to JD's closing price on Tuesday. Walmart will instead just focus on its 45 Sam's Club locations in China and will obviously have a much smaller footprint in the highly populated nation going forward. WMT is up 0.4% overnight, while JD is trading 7.3% lower.

Very Interesting

Bloomberg News reported on Tuesday that Citibank global head of FX quantitative investor solutions Kristain Kasikov is seeing a small and probably short-term, reverse carry trade taking shape. The carry, for now, involves the borrowing of U.S. dollars to fund investments in emerging markets.

Kasikov said, "We've seen our positioning sentiment on the U.S. dollar starting to turn much more bearish."

Kasikov added that hedge funds were now using the U.S. dollar rather than the Japanese yen as the currency of choice to fund risky investments elsewhere as the BOJ is tightening and the Fed is expected to ease. Kasikov mentioned that the dollar was also being used to buy the Brazilian real and the Turkish lira.

You Be the Judge

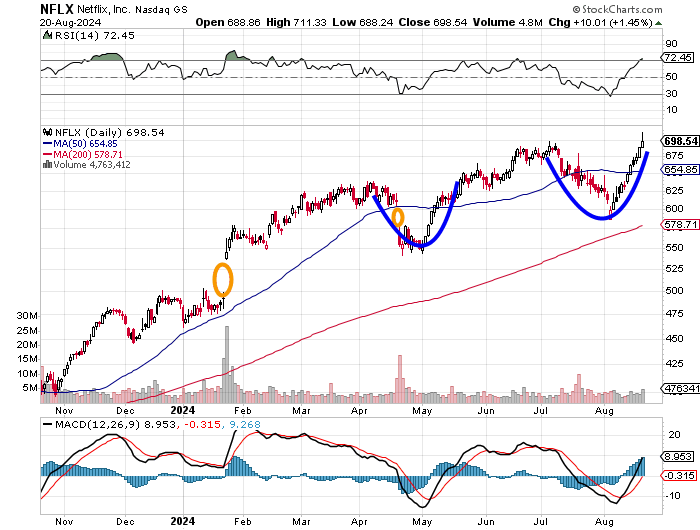

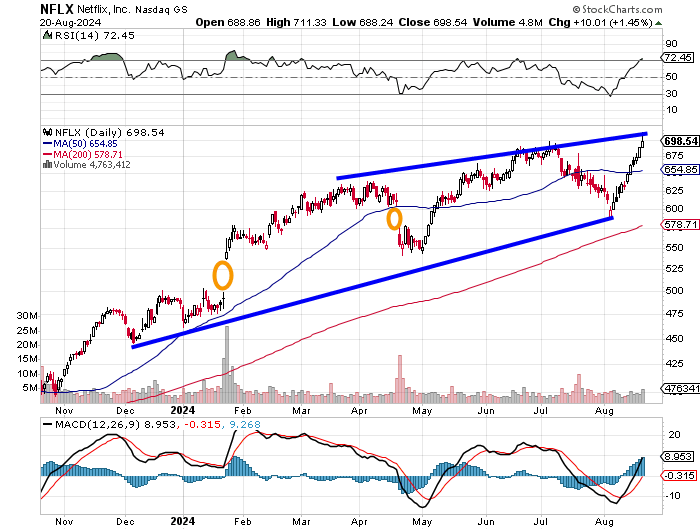

Long-time readers know my record in Netflix NFLX is not one of celebration and consistent victory. My higher profile calls in the name have been shorts, and I have usually ended up having to manage the heck out of those positions to minimize losses or squeeze out pennies that I thought should have been dollars. I am not in the name right now. When you have trouble hitting the curve, you learn not to swing at it. That said, NFLX is at a technical crossroads.

So, what do you see?

Is NFLX set to break out to the upside from a cup pattern as it has in the past? It is trying to move past what would be the pivot should a handle not develop, right now.

Or is NFLX forming a rising wedge pattern, which is a pattern of bearish reversal. If that's the case, NFLX is now at resistance. I'm sitting this one out. Though, I thought a few of you kids might be interested to know that there are two ways to see this chart right now and that the stock is at the point of commitment one way or the other.

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.54%.

07:00 - MBA Mortgage Applications (Weekly): Last 16.8% w/w.

10:30 - Oil Inventories (Weekly): Last +1.357M

10:30 - Gasoline Stocks (Weekly): Last -2.894M.

13:00 - Twenty Year Bond Auction: $16B.

The Fed (All Times Eastern)

All Day - Jackson Hole Economic Symposium.

14:00 - FOMC Minutes.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: ADI (1.51), M (.30), TGT (2.19), TJX (.92)

After the Close: A (1.26), NDSN (2.34), SNOW (.16), URBN (1.00), ZM (1.22)

At the time of publication, Guilfoyle was long TJX, NVDA and WMT equity.