Doug Kass: Investors Aren't Being Compensated for Multiple Risks

Beyond the next few months, I fully expect equities to finally fall back to an area that represents value to us.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

"There have been times in my life that I've been awash in so many opportunities that I could have invested everything by nightfall, and then there's other times (like now) ... when we just haven't seen anything that makes sense, that moves the needle"

- Warren Buffett (Berkshire Hathaway's 2024 Annual Meeting)

Like Warren Buffett, I continue to view the market as overvalued.

At the core of my ursine outlook is the specter of "slugflation" (sluggish economic growth and sticky inflation).

* Sluggish Economic Growth: I am growing increasingly concerned about domestic economic growth as the lagged impact of cumulative (or "stacked" inflation) takes hold.

The U.S. economic surprise Index has turned negative for the first time in a year:

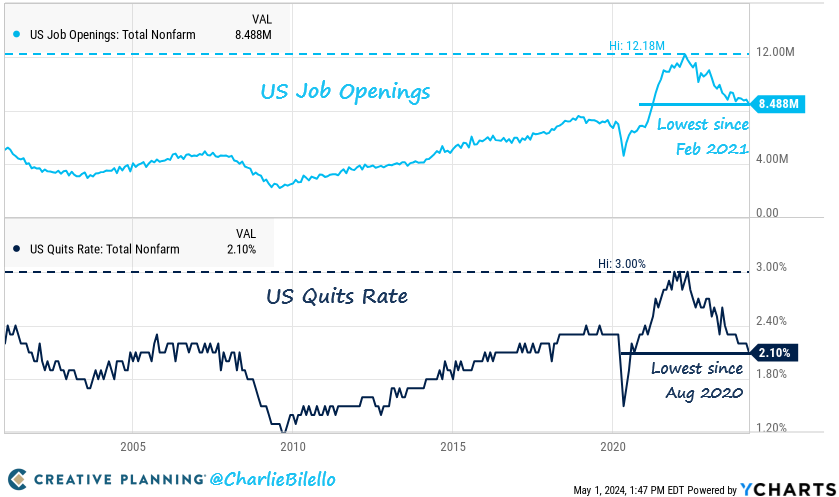

The labor market is cooling off:

Job openings are dropping to the lowest level in over three years:

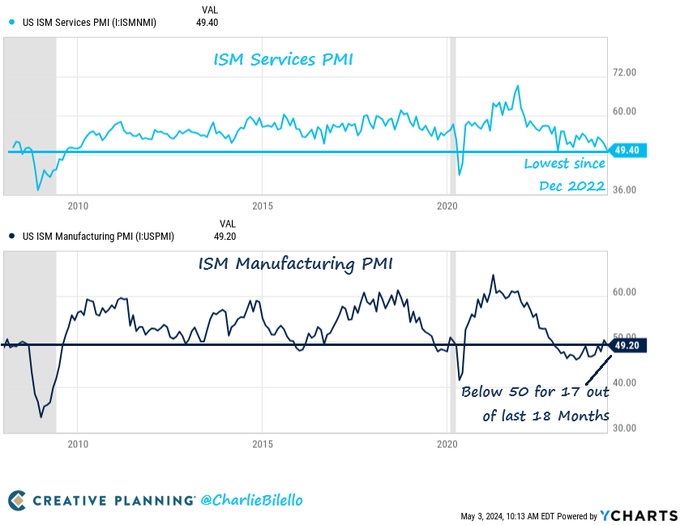

The ISM Services PMI moved below 50 for the first time since Dec 2022. ISM Manufacturing PMI has been below 50 for 17 out of the last 18 months. The only times when both PMIs have been below 50 at the same time:

* July 2008 (recession)

* July 2009 (recession)

* April-May 2020 (recession)

* December 2022

* Today...

U.S. manufacturing and services employment has simultaneously contracted for three consecutive months. Over the last 20 years, this has happened ONLY twice, during the 2020 pandemic and 2008 Financial Crisis:

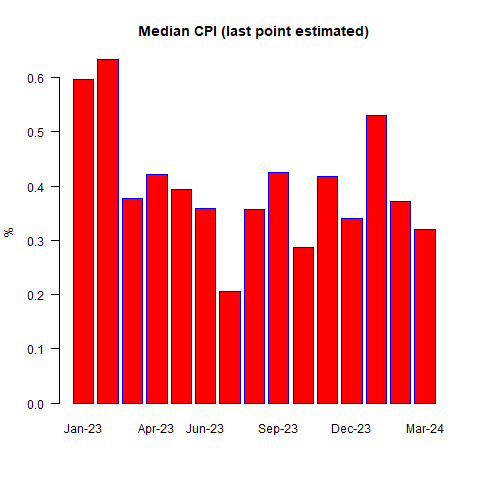

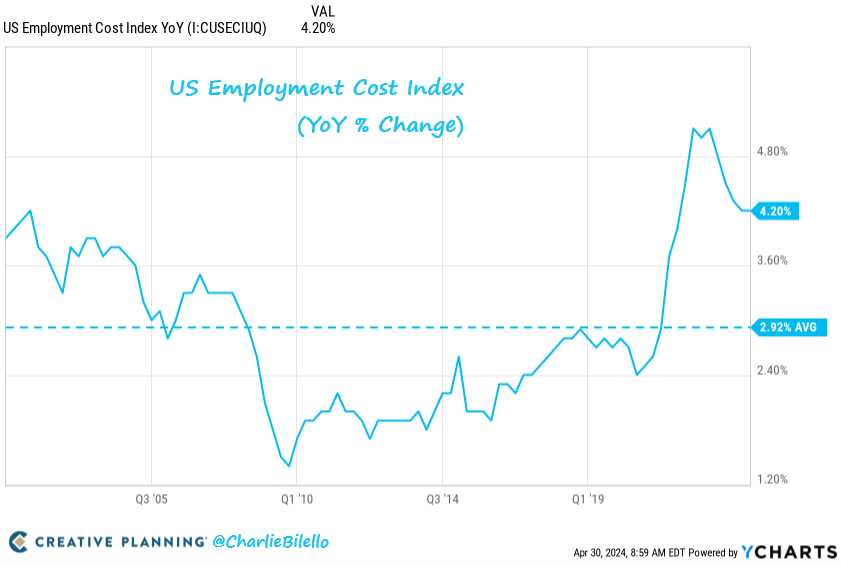

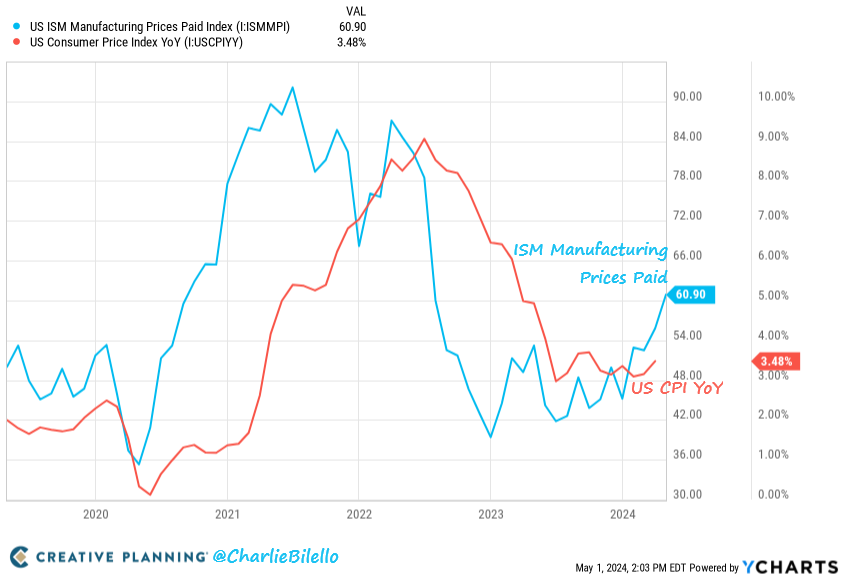

* Sticky Inflation:

The broadest measure of U.S. labor costs (a large component of the CPI) rose by +4.2% over the last year - far above expectations:

The prices paid component of ISM Manufacturing has moved up to its highest level in two years, potentially signaling higher inflation for longer. This was a leading indicator of the inflationary spike in 2021-22:

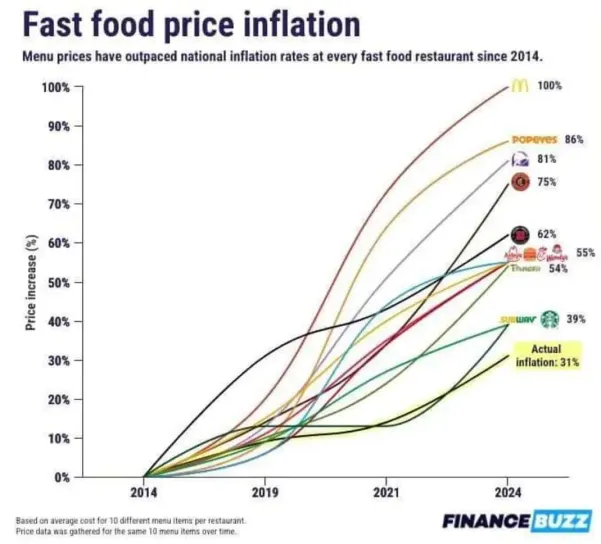

* Stacked (or Cumulative) Inflation: Inflation has already begun to eat into company top line sales - the rapid rise in admission prices of the theme parks at The Walt Disney Company DIS and in the high cost of meals and coffee at McDonald's MCD and Starbucks SBUX. We remain short all three of these stocks!:

_____

Other factors concern us as well.

Equity valuations are climbing despite irresponsible fiscal leadership in Washington, D.C. that render any attack on controlling the rapidly expanding U.S. deficit as unlikely in a backdrop of extreme partisanship and in front of the presidential election in November 2024:

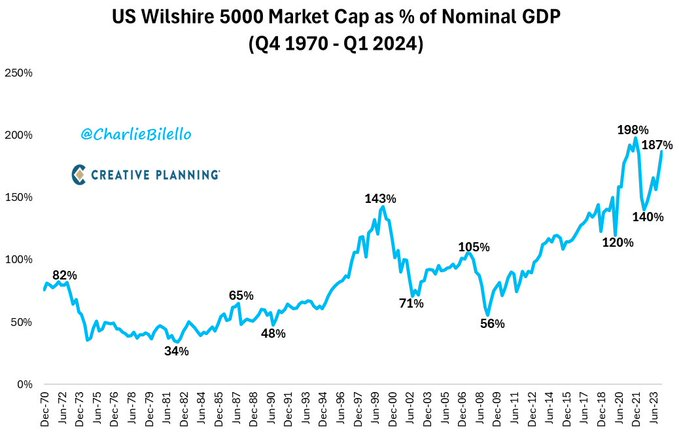

By most historical metrics, stocks are valued in the 90% tile or higher:

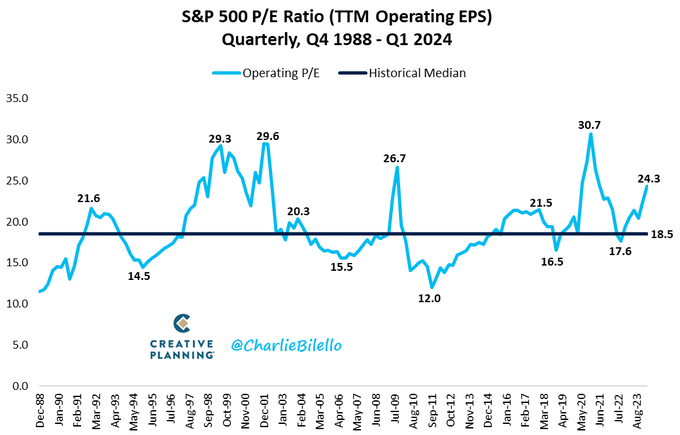

The S&P 500's Price/Earnings ratio moved up to 24.3x in Q12024, which is 31% above the median Price/Earnings ratio since 1988 (at 18.5x):

The suppression of interest rates over the 2008-2022 interval and the rabid fiscal largesse since Covid have artificially distorted our economy and our markets. But, the long and variable lag of monetary policy actions over the last two years is now beginning to be felt particularly in the commercial U.S. real estate markets.

Disturbingly, a domestic economic downturn might coincide with a need to continue large fiscal expenditures — raising the chances that individual and corporate tax rates are raised in an untimely manner (in order to fund that spending.

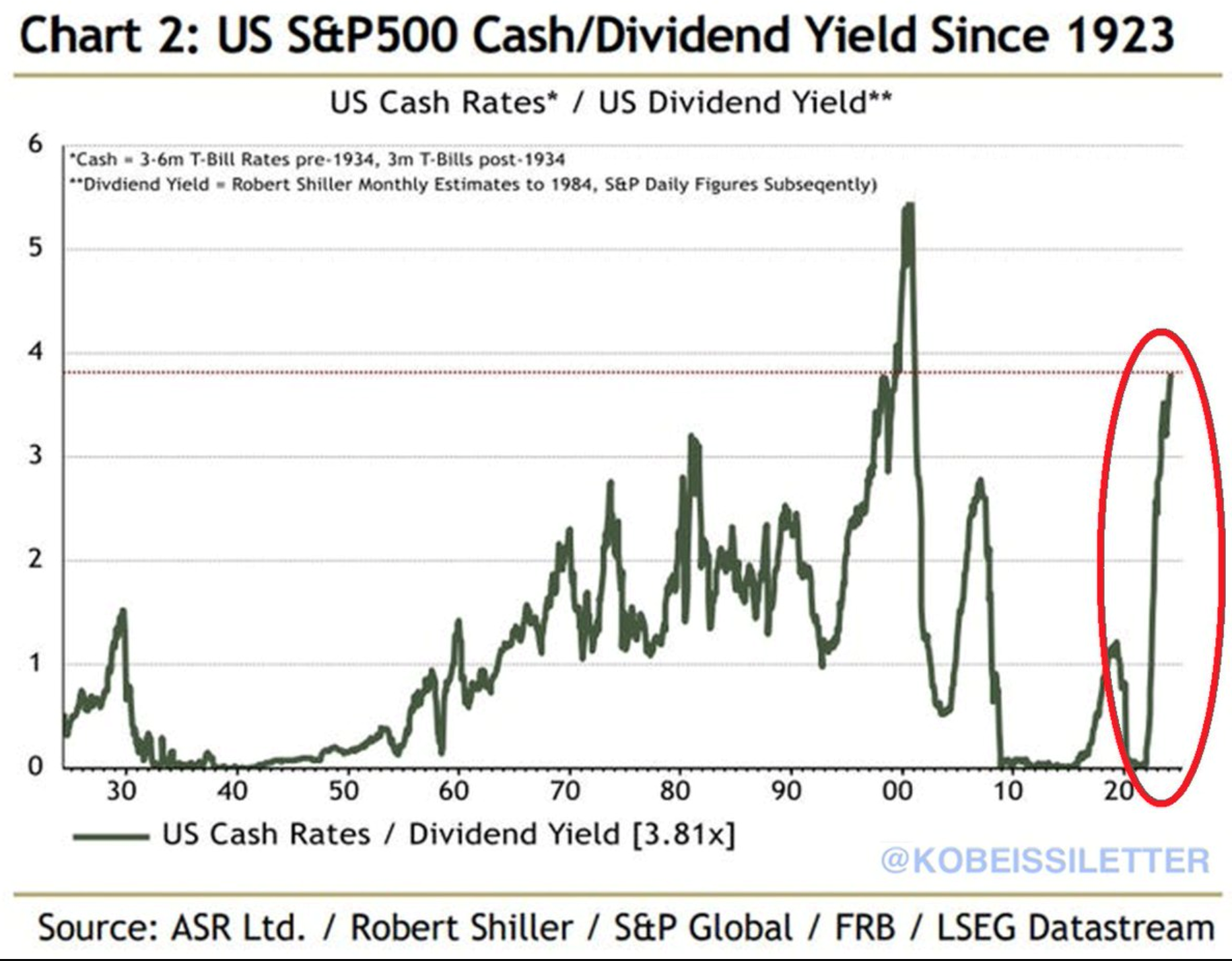

As noted previously, stocks seem particularly overvalued relative to interest rates. Relatively high interest rates have continued to produce a paper-thin equity risk premium (which is at the lowest level in almost two decades). Noticeably, the S&P dividend yield (1.38%) compares unfavorably to the return on 6-month Treasuries (5.34%):

In summary, investors are not being compensated for the multiple risks we see.

All the factors described above - and others - will likely contribute to disappointing corporate profits (relative to consensus expectations) and lower stock market valuations.

Tactical Strategy

Investing is the intersection of economics, analysis and psychology.

The understanding of a company's "intrinsic value" and weighing that calculus against the current share price provide us with the determination of a security's upside reward v. downside risk. This is the essence of value investing. It also provides us, in theory, with a "margin of safety" — a lodestar to our investment strategy.

The input of one's analysis forms the basis for the accuracy of the reward v. risk proposition.

I am respectful of the market's price momentum which is influenced importantly by a changing market structure in which passive investing has vastly eclipsed active investing. That said, I have no issue, when justified by my analysis, with adopting a contrarian position and going against the tide.

A non-consensus view may be especially appropriate now - particularly in the face of higher/inflated equity prices coupled with the accumulated fundamental headwinds discussed in this commentary.

In doing so, I am reminded of a famous quote from Larry McCarthy — a trader of fearless resolve and one of the most respected junk bond traders on Wall Street:

“Higher prices bring out buyers. Lower prices bring out sellers, and size opens eyes. Time kills trades. When they’re cryin’ you should be buyin’. When they’re yellin’ you should be sellin’. Takes years for people to learn those basics – if they ever learn them at all.”

To conclude, I am a disciplined contrarian and I select equities (long and short) through hard-hitting analysis, with a calculator in hand.

I plan to be patient in continuing to pursue a risk-averse strategy concentrating on pairs trading with a small short overlay over the near term.

Beyond the next few months, I fully expect equities to finally fall back to an area that represents value to us.

Representative Longs

My representative longs include Goldman Sachs GS, Morgan Stanley MS, St. Joe Co JOE, Peapack Gladstone Financial PGC , DraftKings DKNG, Valvoline VVV, Viking Therapeutics VKTX, Green Brick Partners GRBK, Freshpet FRPT, Elanco Animal Health ELAN, Johnson & Johnson JNJ, Exxon Mobil XOM, Chevron CVX, Procter & Gamble PG and Sprott Uranium Miners URNM.

Representative Shorts

My representative shorts include McDonald’s MCD, Walt Disney Co DIS, Starbucks SBUX, Tesla TSLA, PowerSchool Holdings PWSC, Medical Properties Trust MPW, Winnebago WGO, Sleep Number SNBR, B. Riley Financial RILY, Freedom Holding Corp FRHC, Petco Health and Wellness WOOF, Warner Bros. Discovery WBD, Chegg CHGG, FIGS FIGS, Blackstone Mortgage Trust BXMT and Xponential Fitness XPOF.

At the time of publication, Doug Kass was long and short the above names.

This article was previously published on Doug's Daily Diary.