Cracks in the Facade?

Are we witnessing statistical noise, or does recent data indicate something more worrisome?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It’s been said that markets climb a wall of worry. Well, markets have been climbing, but when it comes to the U.S. economy, there seems to be little to fear.

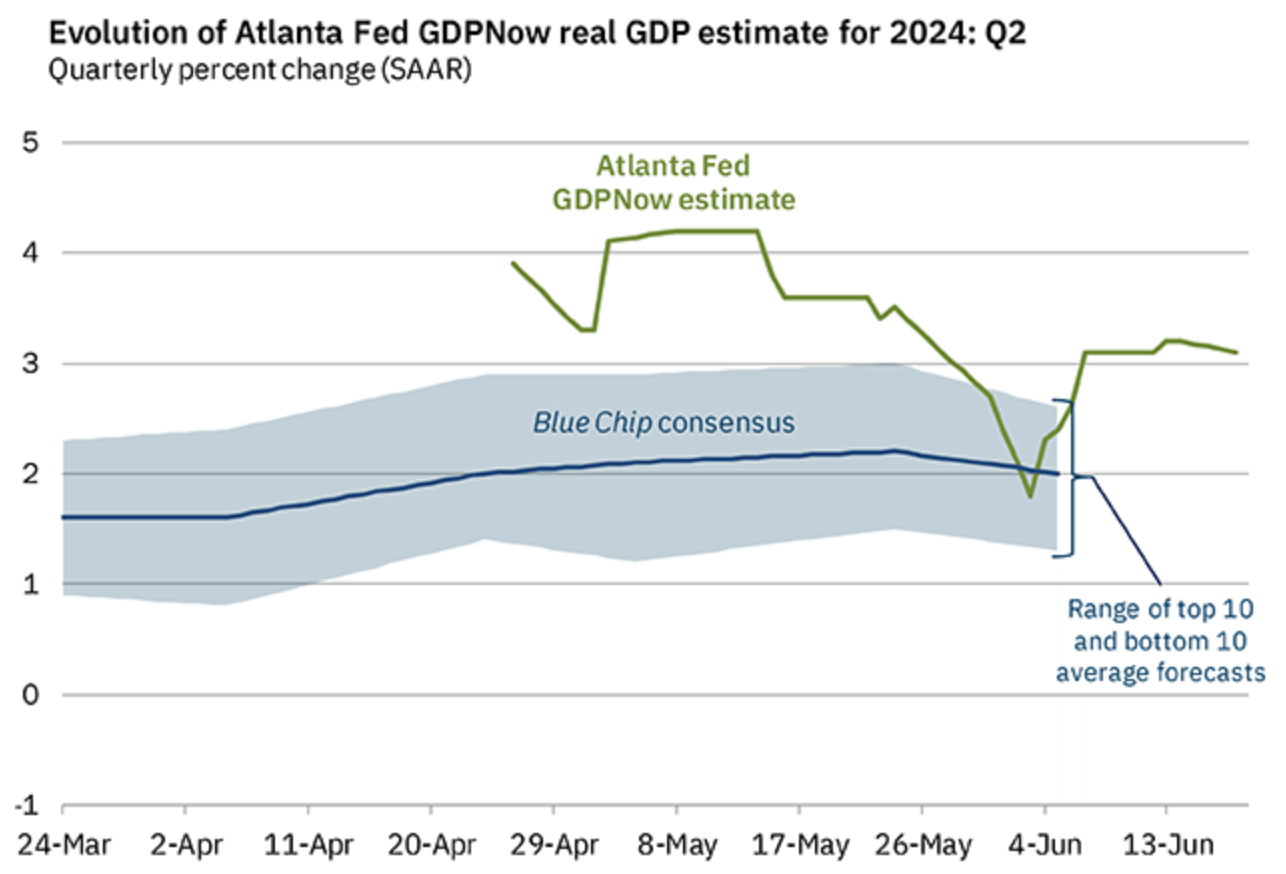

The Atlanta Fed’s GDPNow update for June 18 suggests that second quarter GDP will come in at 3.1%. As recently as May 31, GDPNow projected second quarter GDP growth at 2.7%. After a pullback, this estimate has been trending higher (green line).

Job creation remains strong. According to the Bureau of Labor Statistics (BLS), the U.S. economy produced an average of 249,000 jobs per month over the past three months (upper line).

This figure is tempered somewhat when we focus only on jobs created by the private sector. Still, an average of 206,000 private sector jobs per month over that same stretch (lower line) indicates that the job market remains resilient.

Robust results in private education and health services (89,300 average over the past three months), health care and social assistance (88,000 3-month average), and leisure and hospitality (36,000 3-month average) bode well for continued strength.

A resilient job market, combined with our current state of disinflation, would seem to present an ideal economic situation.

Unfortunately, there are cracks in the facade - or at least, what appear to be cracks at first glance.

Several key reports have missed the mark in recent weeks. Are we witnessing statistical noise, or does recent data indicate something more worrisome?

To find out, let's take a closer look at three recent economic indicators.

JOLTS (Job Openings and Labor Turnover)

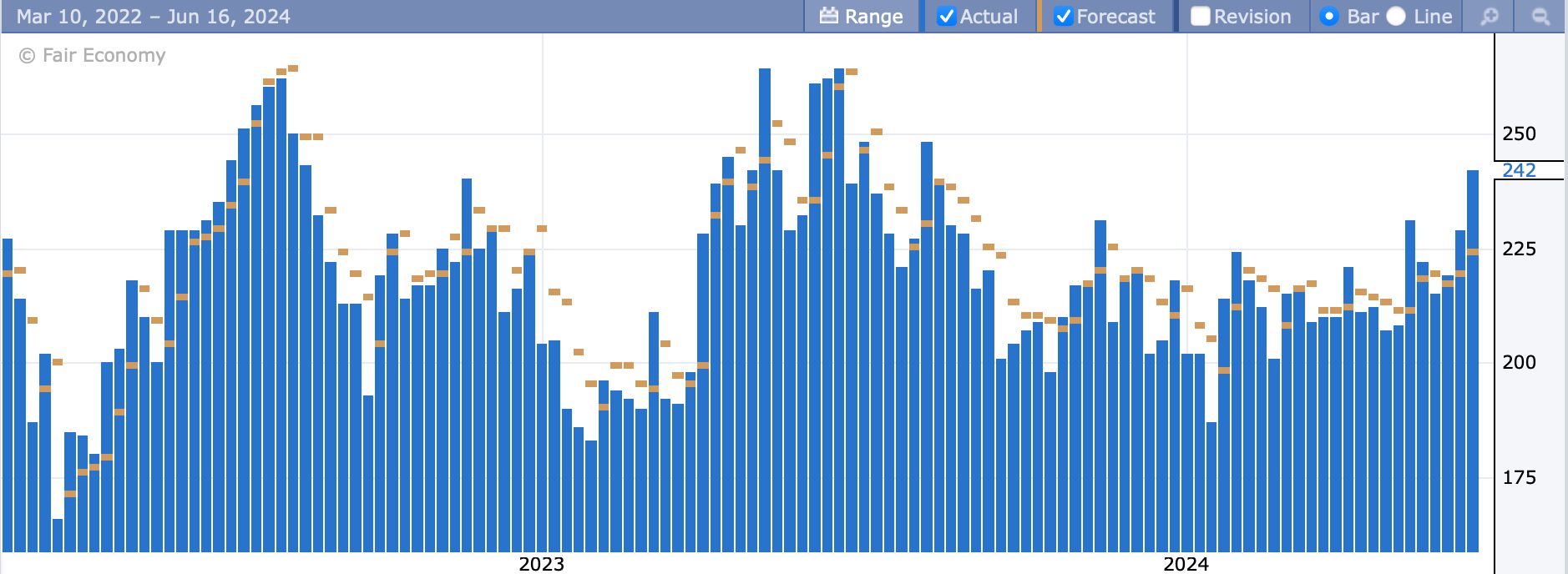

The June 4 JOLTs (Job Openings and Labor Turnover) report presented its worst result since May of 2021. According to that report, there were 8.06 million U.S. job openings at the end of April.

Two years ago, that figure was above 11 million. At first glance, this may appear troublesome.

While those stats may appear to be negative, they’re not - at least when compared to pre-pandemic levels. Prior to the pandemic, the highest JOLTs figure recorded this century was about 7.6 million, in November of 2018.

Based on this chart, the record JOLTs figures of 2022 were an anomaly, and current levels of job openings are in line with the long-term trend.

JOBLESS CLAIMS

Unemployment claims have been trending higher since the start of this year. Last Thursday’s reading of 242,000 newly unemployed workers was the highest level reached since August of last year.

While the right side of this chart is clearly rising, the wider picture shows that unemployment claims have been fluctuating within a range since the late stages of the pandemic. While currently rising, U.S. unemployment claims are well within a normal range.

RETAIL SALES

On Tuesday, advance retail sales figures for May showed a slight increase of 0.1% month-over-month. Excluding auto sales, retail sales declined by 0.1%.

Consumer spending helps drive the U.S. economy, so are Tuesday’s figures a cause for concern?

The flattening of retail sales shouldn’t come as a surprise, due to a combination of higher interest rates and inflation. According to Adriana Kugler, a member of the Fed’s Board of Governors, consumers are "trading down" to lower-cost products.

Walmart (WMT) and Target (TGT) are climbing on board this trend, as they recently announced price cuts on thousands of items.

Bottom line: consumers are still buying - they’re just more price-conscious due to inflation. In inflationary times, trading down seems like normal behavior.

The good news is, consumers haven’t gone on strike, they’re bargain hunting, and that's going to have an impact on retail sales statistics.

One final caveat: while these so-called cracks appear to be nothing more than anomalies, they do bear watching. We'll reevaluate this data if JOLTs or retail sales fall off a cliff, or if unemployment claims skyrocket.