Consumer Price Index Is Ready to Make Landfall

Twisters and heavy rain hit in Florida and now we wait for the market's main event that could be the lull before October; Also, let's check the chart of Broadcom.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

So far, so good. Zero dark-thirty. On the east coast of central Florida there was one pre-hurricane tornado after another for most of Wednesday afternoon and evening. We have lost power a couple of times now, but never for very long. At least so far. I don't want to jinx us. My home appears to be in good shape. We have a little flood in the back, in a room that's built for it. My wall of sandbags and mulch-bags did a pretty decent, but imperfect job.

I think all of my trees are still standing, but my windows are shuttered, so my vision, especially through the dark hours, is limited. I lost a part of one tree from Hurricane Helene and that storm missed us by hundreds of miles. This one is currently passing overhead.

As for the area, a nearby Wells Fargo branch lost its roof. A strip mall near the bank sustained fairly significant damage as did a number of homes. At one point, I had to wake my wife and get us into a bathroom central to our home. There was one tornado two miles directly to our south and another one about six miles to our northeast.

I have a number of folks on the west coast of the state to check on once we see daylight. I know that the ballpark where the Tampa Bay Rays play their home games, a domed stadium, lost its roof. Hoping for the best possible outcome and praying for the safety of all impacted.

The Main Event: CPI

This morning, the Bureau of Labor Statistics will drop its September consumer price index data upon us, which will be this week's "main event." We are looking for a further slowing of both headline and core prices on a month over-month-basis, and a slowing of headline year-over-year inflation. As readers likely know, I have been expecting September to be the low for the year in terms of year-over-year CPI. The renewed acceleration in consumer pricing likely starts with October and in my opinion will gradually build into the first or second, most likely second, quarter of 2025.

This morning's results will most likely embolden the members of the Federal Open Market Committee who have been more aggressive in terms favoring a quick and sustained move toward easier interest rate policy. This will also embolden investors who have been betting on much lower short-term rates.

Currently, after the release of a string of stronger than (I ever) expected macroeconomic data-points, futures markets trading in Chicago are now pricing in an 18% probability for no rate cut at all on Nov. 7. That's a doubling of that likelihood this week alone. That does leave an 82% chance for a quarter-point rate cut just after the election. These markets are still pricing in a 78% probability for a half-percentage point worth of rate cuts by year's end.

Friday morning will bring us both September Producer Prices and the earnings releases of JP Morgan JPM and Wells Fargo WFC as the large money center banks get the third-quarter earnings season under way.

Marketplace

The bifurcation of U.S. financial markets continued on Wednesday. Equity traders continue to act as if earnings are growing wildly, and interest rates are going lower. CPI leak? That said, Treasury markets continue to either price in no further rate cuts or are finally taking the U.S. federal debt-load seriously.

Both gold and WTI Crude held at lower levels from where they traded earlier in the week, despite a U.S. Dollar that continues to appreciate vs. its reserve currency peers. Bitcoin has taken something of a beating over the past few days, in dollar terms.

The S&P 500 gained 0.71% for the day, while the Nasdaq 100 gained 0.8%, significantly outperforming the Nasdaq Composite, which was up 0.6%. Small caps lagged but still showed gains for the session as the KBW Banks and Philly Semiconductors led the mid-majors, gaining 1.25% and 1.06% respectively.

Arm Holdings ARM and Broadcom AVGO led chip stocks as Nvidia NVDA and Advanced Micro Devices AMD paused one day ahead of AMD's big AI event. Jensen Huang is done for the week. Now, it's Lisa Su's turn.

On Breadth and 'Baloney'

Ten of the 11 S&P sector exchange-traded funds shaded green on Wednesday, as both Technology XLK and Health Care XLV gained more than 1% over the day. Only the Utilities XLU closed in the red. Winners beat losers by an almost 2 to 1 margin at the NYSE, but this may surprise ... losers beat winners by a narrow margin at the Nasdaq. Advancing volume took a 63.7% share of composite NYSE-listed trade and a 54.1% share of composite Nasdaq-listed activity.

Aggregate trading volume increased across NYSE-listings from Tuesday's totals but decreased on a day over day basis for Nasdaq-listings. What does it all add up to? In my opinion, an uncertain optimism that has diverged from other financial markets. My thoughts on that? Take advantage rather than call it "baloney." Right or wrong, we adapt to the environment in front of us. That's how winning is done. We're players in a game, not the game's creator.

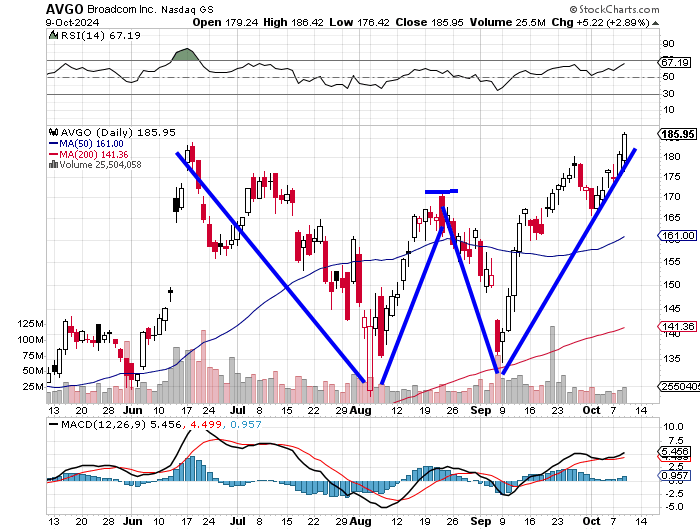

Speaking of Broadcom

That name has broken out past a $172 pivot created by s double-bottom reversal pattern and is now attempting to take and hold new post-June highs.

A double-bottom pattern at the top of the chart? OK, call is a basing period of consolidation if you want. That only serves to take the pivot from $1172 up to $185. Making this morning's action all the more important. I have no current position.

My Trading Amid Tornadoes

As readers have probably guessed, I was not very active on Wednesday. I did, however, add to longs in both the Goldman Sachs Physical Gold ETF AAAU and the SPDR Gold Shares ETF GLD on weakness before I started bobbing and weaving tornadoes.

Note To Readers: I will be off tomorrow (scheduled) and most of next week, as I have family coming down from the Northeast and I have taken very little time these past few years, which kind of ticks my wife off. She thought I would become a normal human as I aged.

Economics (All Times Eastern)

08:30 a.m. - Initial Jobless Claims (Weekly): Expecting 225K, Last 230K.

08:30 - Continuing Claims (Weekly): Last 1.826M.

08:30 - CPI (Sep): Expecting 0.1% m/m, Last 0.2% m/m.

08:30 - Core CPI (Sep): Expecting 0.2% m/m, Last 0.3% m/m.

08:30 - CPI (February): Expecting 2.3% y/y, Last 2.5% y/y.

08:30 - Core CPI (February): Expecting 3.2% y/y, Last 3.2% y/y.

10:30 - Natural Gas Inventories (Weekly): Last +55B cf.

1:00 p.m. - Thirty Year Bond Auction.

The Fed (All Times Eastern)

09:15 - Speaker: Reserve Board Gov. Lisa Cook.

10:30 - Speaker: Richmond Fed Pres. Tom Barkin.

11:00 - Speaker: New York Fed Pres. John Williams.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: DAL (1.55), DPZ (3.65), TLRY (-0.03)

At the time of publication, Guilfoyle was long WFC, XLU, NVDA, AMD.