Beat-Down City, Markets Face Economic Reality, Intel's Disaster, Trading Amazon

All of the horrible, frightening things that you go to sleep trying not to think of were unleashed Thursday. We could use a 2023/2024 style overstated number for job creation right now.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Happy Jobs Day!

You know, even though we all know that the BLS monthly Employment survey results are not worth the paper that they are printed on (if they were actually printed on paper), the markets could use a 2023/2024 style overstated number for job creation right now.

After the past few days, or after Thursday, specifically, financial markets were forced to face economic reality. You could have heard the ugly stick revving up inside Pandora's Box just before somehow, someone left that box unlocked. All of the horrible, frightening things that you go to sleep trying not to think of were unleashed. The ugly stick among them. Bopping not just the field mice over the head with a nasty attitude, but hitting bid after bid, until the algorithms realized all too quickly that maybe for now, they should bid no more.

As if Wednesday's awful prints for June ADP private sector job creation, and the July Chicago PMI were not bad enough, Thursday got real nasty. The Department of Labor dished out 249,000 weekly initial jobless claims, which was the most people signing up for state-level unemployment benefits in one week in a year. Continuing jobless claims increased to the highest number of Americans out of work on a sustained basis since November 2021.

Then came a real disaster. The July ISM Manufacturing PMI. Maybe we should not be so surprised. The U.S. has been in at least an Industrial recession for years now. We had thought that the contraction in the manufacturing space was running out of steam. We thought wrong.

The ISM survey printed at 46.8 at the headline, down significantly from June and far below expectations. The headline print has reflected monthly contraction from the month prior in 20 of the past 21 months. July was the most severe single-month contraction since November.

New Orders contracted at an accelerated rate as did Production. Manufacturing-based employment fell off of the map, with the ISM report reading "Respondents' companies are continuing to reduce head counts through layoffs, attrition and hiring freezes." Backlogged Orders fell to a jaw dropping 41.7 in June and maintained that level of contraction in July. Do readers understand how hard it is to be that weak two months in a row? Inventories contracted for an 18th consecutive month. Oh, there was expansion in one key area. You guessed it. Prices.

I'm not done. June Construction Spending hit the tape at -0.3% month over month, coming off of May's -0.4%. Wall Street had been looking for something more like +0.2%. Q2 GDP revisions anyone? Not until August 29.

Don't Forget...

The U.S. federal debt-load crossed the $35 billion mark earlier this week. As Dougie Kass pointed out on Thursday in his Daily Diary on TheStreet Pro, every month the federal government adds $196 billion in brand new debt. Every single day, the federal government adds $6.4 billion in brand new stinking, filthy debt. Doug breaks it all down to the most minute detail... $75,000 per second. Nice job, America. You need every taxpayer to bail out every stinking thing you think of. Well, you broke them. You broke the bank. Nice going.

What happens now? BOJ monetary policy has entered a tightening cycle despite being in recession. That's how afraid of consumer-level inflation they are. The yen, a reserve currency, cracked the 150 level again on Thursday, but this time headed in a northerly direction. Does the U.S. default? Of course not, the U.S. can print its own money. Exactly.

It won't happen today and hopefully it won't happen tomorrow, but I find it difficult to imagine the U.S. Treasury doing anything other than eventually monetizing the debt or a substantial portion of it. That's the only thing that can bail out the over-indebted who will not show the political will or fiscal discipline to do right by the people.

Won't that make inflation worse, Sarge? You bet your tailpipe it will. Enjoy that September interest-rate cut. Fifty basis points with a core CPI still at 3.3% and one reserve currency central bank swimming upstream.

Savers and folks living on fixed income? Your legislators never even considered you. Not for a second. Unless you help feed their agenda. Good grief. Got a tune running through my head as I work through the zero-dark hours this morning.

Take Your Whiskey Home

But it takes me at least halfway to the label

'Fore I can even make it through the night

Well, I think that you're headed for a whole lot of trouble

Yeah, yeah, I think that you're headed for a whole lot of trouble

Baby yeah, I think you're headed for some trouble

If you take your whiskey home

-- A. Van Halen, E. Van Halen, Roth, Anthony (Van Halen), 1980

They Love Them Some U.S. Treasury Securities

Quantitative easing on the way? Investors sought safety on Thursday, and U.S. sovereigns are still considered safe. Muhahahaha!!!

The U.S. 10-Year Note paid just 3.99% by the time they shut down on Thursday. That was the first time that 10-Year paper paid less than 4% since February.

This morning, I have seen the 10-Year yield just 3.95%. The 2-Year Note? Went out yielding 4.17% last night. Pays just 4.14% this morning.

Beat-Down City, USA

Incredible. The Philadelphia Semiconductor Index suffered a 7.14% beating on Thursday, leading the Technology sector SPDR XLK 3.7% lower, and the Nasdaq 100 down by 2.44%. Run to small-caps? The Russell 2000 gave up 3.03% on Thursday. Run to the Dow Transports? Down 1.69%. The S&P 500 beat the broader market on Thursday (that sounds weird) by losing "just" 1.37%, while the Nasdaq Composite surrendered 2.3%.

Remember Moderna MRNA? Going to save the world. Well, nobody saved Moderna on Thursday as that name gave up 21% post-earnings. MGM Resorts MGM? Down 12.3%. Lam Research LRCX and Qualcomm QCOM, down more than 9% a piece.

Did anyplace provide a safe harbor on Thursday? Well, yes. There were four winners among the 11 S&P sector SPDR ETFs. The four defensive sectors, Utilities XLU, REITs XLRE, Health Care XLV, and Staples XLP, all gained more than 1% for the regular session.

That said, losers beat winners by more than 2 to 1 at the NYSE and more than 3 to 1 at the Nasdaq as advancing volume dwindled and aggregate trading volume increased for names listed at both exchanges. Professional money was on the move on Thursday and from the looks of overnight futures markets, still probably is. We'll see what employment surveys do to these markets in a few hours.

Intel

You've got to be kidding me. EPS miss, Revenue contraction and miss. Horrible guidance. I wouldn't buy Intel INTC with your money even if I hated your guts.

I expected to wake up and see that CEO Pat Gelsinger had been let go. Guess not yet. You know I thought this company had a shot when Krzanich was running the show. Too bad he was goofing off. Intel has not seemed competitive since.

Amazon Reports

A significant EPS beat for Amazon AMZN. Slight revenue miss on 10.2% growth. Operating income crushed guidance. Forward guidance on the light side.

Amazon Web Services was the only business unit that beat its sales expectations, growing 18.7%, with Wall Street looking for 18% growth. This is the margin driver for the company. AWS generated 63.6% of its operating income on a 35.5% operating margin.

The rest of the company? Online Stores, Physical Stores, Subscription Services, and even Advertising Services all fell short of revenue expectations. Regional operating margin, ex-AWS... North America 5.63%, International 0.86%. Eek, the cat.

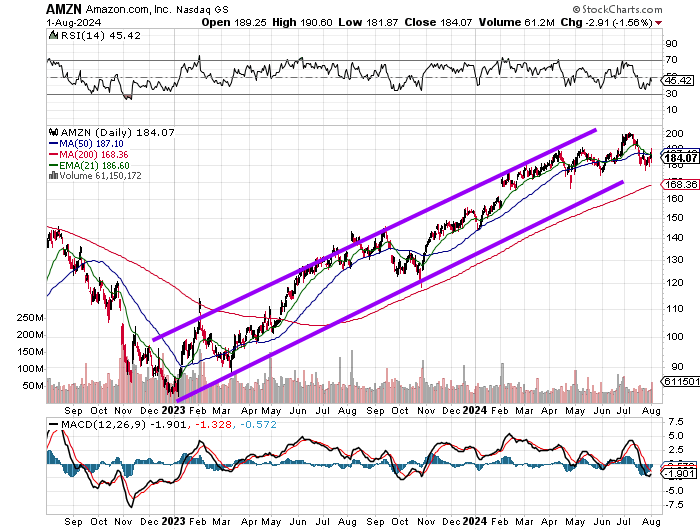

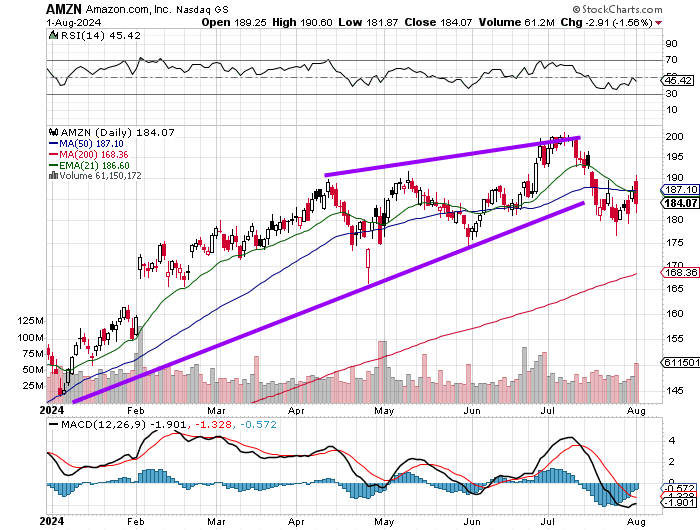

I have shown you this 18-month price channel a thousand times (it seems), and it has served us well. Unfortunately, things, and Amazon's chart, have changed.

See the rising wedge? I apologize to loyal readers for not recognizing this pattern sooner. Rising wedges are patterns of bearish reversal. AMZN appears to have broken out to the downside.

Any way out of this? Yes, AMZN closed $3 below its 50-day simple moving average (SMA) on Thursday. It has to take that line back quickly in order to improve its short-term outlook. Amazon's Realtive Strength Index (RSI) is neutral, but its daily Moving Average Convergence Divergence (MACD) is postured bearishly.

The stock could, on a weak opening, test that 200-day SMA in the high $160s this morning. Will I sell some or all of my AMZN, which is not a top-10 holding of mine (number 14)? Like every other professional in this business, if that line fails, I'll be a seller. If it holds, I'll add on the discount. Fun game. Not.

Stay Tuned for Apple

I'll be back in a bit with an in-depth analysis of Apple AAPL for TheStreet Pro readers.

July Employment Situation (08:30 ET)

Non-Farm Payrolls: Expecting 182K, Last 185K.

Unemployment Rate: Expecting 4.1%, Last 4.1%.

Underemployment Rate: Last 7.4%.

Participation Rate: Expecting 62.5%, Last 62.6%.

Average Hourly Earnings: Expecting 3.9% y/y, Last 3.9% y/y.

Average Weekly Hours: Expecting 34.3, last 34.3 hours.

Other Economics (All Times Eastern)

08:30 - Factory Orders (June): Expecting 0.5% m/m, Last -0.5% m/m.

13:00 - Baker Hughes Total Rig Count (Weekly): Last 589.

13:00 - Baker Hughes Oil Rig Count (Weekly): Last 482.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: CVX (3.00), XOM (2.04), LIN (3.79)

After the Close: AMC (-0.36)

At the time of publication, Guilfoyle was long XOM, AMZN equity. Long AAPL calls, Long AAPL puts.